Electricity Retail Pricing Packages for the Energy Transition: International Experience, Design Mechanisms, and Emerging Trends

Hang Jing*, Yansong Xia, Houzhi Li and Mingze Gao

State Grid Smart Vehicle-to-Grid Technology Co., Ltd., Beijing 100031, China

E-mail: jinghang@evs.sgcc.com.cn

*Corresponding Author

Received 04 October 2025; Accepted 26 November 2025

Abstract

Retail electricity tariffs have transitioned from uniform cost-recovery schemes to diversified packages that incorporate temporal, locational, and carbon-intensity signals. This paper reviews the evolution of retail pricing mechanisms, their global applications, and the design principles that underpin modern tariff innovation, and it further identifies electric-vehicle (EV) charging tariffs as a rapidly expanding subset within this broader transformation. Drawing on cases from the United States, the European Union, Australia, Japan, and China, the review traces the progression from traditional two-part tariffs to smart-meter-enabled time-of-use pricing, real-time dynamic rates, and subscription–dynamic hybrid designs. Core mechanisms – marginal-cost reflection, risk hedging, digital customer segmentation, and vehicle-to-grid integration – are evaluated in terms of system efficiency, cost recovery, and distributional fairness. Evidence shows that time-of-use pricing combined with automated control can reduce peak load by 5%–15%, real-time pricing pilots achieve up to 20% load shifting, and subscription-based EV tariffs lower annual charging expenses by 25%–35% while maintaining renewal rates above 90%. The analysis concludes that jurisdictions capable of integrating digital infrastructure, flexible regulation, and equity safeguards are best positioned to deliver retail tariff designs that are efficient, resilient, and socially inclusive.

Keywords: Datacenter design, energy efficiency of datacenter, energy efficient metrics, datacenter carRetail electricity tariffs, time-of-use pricing, real-time pricing, subscription-based tariffs, electric vehicle charging packages, risk-sharing mechanisms.

1 Introduction

In the complex context of global energy transition and accelerating digitalization, electricity retail pricing schemes have evolved from early flat-rate tariffs oriented toward cost recovery into diversified product portfolios that incorporate temporal, spatial, and carbon-intensity differentiation, while simultaneously balancing user demand flexibility and system efficiency [1]. On the one hand, the widespread deployment of smart metering and wide-area communication networks has enabled near real-time observability of electricity consumption data, providing the technical foundation for granular pricing on an hourly or even 15-minute basis. On the other hand, the large-scale integration of distributed photovoltaics, residential storage, and electric vehicles has made the traditional “average-cost pricing” model inadequate for transmitting accurate marginal cost signals, while exacerbating peak–valley mismatches and ramping pressures in power systems with high shares of renewable generation [2]. Between 2022 and 2024, the global energy crisis triggered extreme price volatility, prompting regulators across multiple jurisdictions to pay increasing attention to consumer vulnerability and affordability. A variety of tariff innovations have been introduced, including subscription-based packages, price caps, and social safeguard mechanisms, with the aim of striking a balance between risk-sharing and cost-reflectiveness [3].

In line with this trend, major markets such as the United States, the European Union, Australia, and Japan have either completed or are advancing a third wave of retail reforms centered on “dynamic pricing + default time-of-use + optional hedging.” In North America, several states have already begun transmitting real-time wholesale settlement signals directly to household thermostats and EV chargers, thereby enabling automated load shifting [4]. The European Union has recently advanced toward a more flexible and consumer-centric retail pricing framework through the Electricity Market Design Reform Directive (Directive (EU) 2024/1109), officially adopted on 11 April 2024. The Directive requires all electricity retailers to offer both fixed-price and dynamic-price contracts, mandates that consumers be allowed to switch contracts at any time without penalty, and introduces new safeguards against price spikes – such as hedging obligations, emergency interventions, and enhanced transparency in supplier–consumer contracts. (Official source: Official Journal of the European Union, L 2024/1109) [5]. In the United Kingdom, Ofgem has strengthened the role of retail pricing in supporting local flexibility through the ED3 Network Price Control Framework, released as part of its regulatory guidance package for Distribution System Operators (DSOs) for the 2023–2028 period. The framework encourages DSOs and retailers to pilot locationally differentiated tariffs, flexibility-based compensation schemes, and network-constraint-driven dynamic pricing, supported by targeted innovation allowances under the “Net Zero Innovation Portfolio.” By integrating retail tariffs with local grid constraints and flexibility services, ED3 aims to accelerate decarbonisation while improving distribution-level investment efficiency. (Official source: Ofgem, “ED3 Price Control: Draft Determinations,” 2023) [6]. In Australia and Japan, hybrid packages combining subscriptions with super off-peak pricing have embedded vehicle-to-grid (V2G) functions and renewable integration incentives, leveraging bundled billing and automated scheduling to achieve both system load balancing and household bill stability [7]. By contrast, many emerging economies remain constrained by cross-subsidies and price regulations, typically maintaining lifeline block tariffs. While such schemes protect the basic electricity consumption of low-income households, they provide limited and unsustainable long-term economic signals for distributed resources and digital demand response [8].

Despite a growing body of literature on individual tariff mechanisms, an integrated understanding of how pricing models evolve across different institutional contexts remains limited [9, 10]. Existing studies tend to focus on specific instruments – such as two-part tariffs, real-time pricing, or EV-specific schemes – without connecting them to the broader trajectory of retail market reforms or examining how technological and regulatory conditions shape their feasibility [11]. Moreover, the interaction between retail tariffs and emerging flexibility markets, and the distributional implications across different customer groups, remain insufficiently analyzed.

This review brings together evidence from major electricity markets to construct a comprehensive analytical framework for retail tariff innovation. It synthesizes historical developments, regulatory structures, design mechanisms, and digital-era innovations, with particular attention to how electric vehicle charging schemes extend and reshape retail pricing logic. By linking technological capabilities with institutional arrangements, the paper identifies the mechanisms through which pricing models influence peak-load reduction, risk allocation, cost recovery, and equity outcomes. The study further highlights the conditions under which hybrid pricing structures – combining time-varying signals, subscription components, and automated demand response – achieve superior system and consumer performance. In doing so, the review aims to offer a coherent foundation for future research and provide actionable insights for regulators and market designers navigating the next phase of tariff reform.

Table 1 Historical trajectory of retail electricity price packages

| Period | Key Characteristics | Core Pricing Logic | System Implications |

| 1930s–1980s: Uniform Tariffs | Vertically integrated utilities; single-rate pricing | Cost-plus rates; average cost recovery | Weak demand incentives; growing peak–off-peak gap |

| 1990s–2000s: Market Liberalization & Two-Part Tariffs | Sector unbundling; retail competition | Capacity charges + energy charges; inclining block tariffs | Improved cost recovery; early demand-side management |

| 2010s: Smart Metering & ToU | AMI deployment; granular consumption data | Multi-period ToU rates; seasonal and tiered structures | 5–15% peak reduction; stronger load shifting |

| 2020s–Present: Digitalized & Dynamic Tariffs | Wholesale pass-through; automation; APIs | Real-time pricing; hybrid subscription–dynamic models | 10–20% load shifting; personalization and flexibility. |

2 Historical Trajectory of Retail Electricity Price Packages

Table 1 outlines the historical evolution of retail electricity pricing packages across four stages: from the uniform volumetric tariff in the 1930s–1980s, to inclining block tariffs and two-part pricing in the 1990s–2000s, followed by time-of-use (ToU) and critical peak pricing (CPP) in the 2010s, and finally the real-time dynamic plus subscription-based hybrid models of the 2020s. The driving factors shifted from cost averaging under vertically integrated utilities, to market liberalization and revenue decoupling, then to smart metering and demand response, and ultimately to digital platforms, electric vehicle (EV) loads, and household storage.

2.1 Flat-Rate Tariff Period (1930s–1980s)

In the past decade, a variety of electricity price types have been introduced, and the main ones are shown in Table 2 [12].

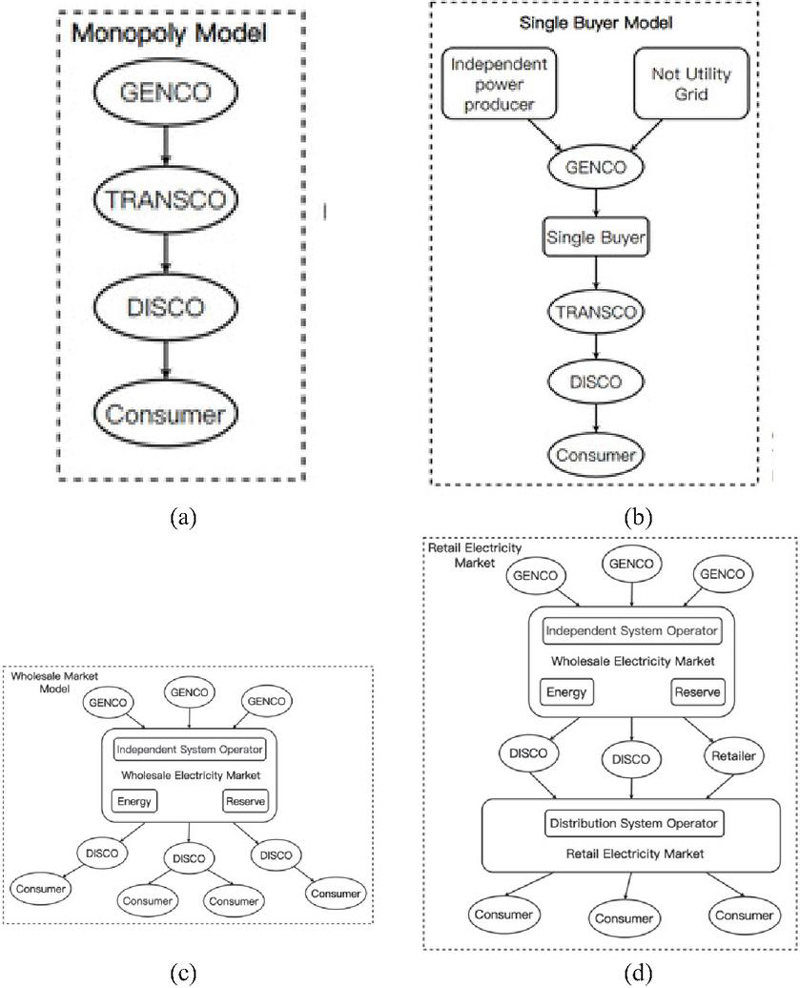

From the 1930s to the 1980s, the global electricity sector was generally characterized by vertically integrated utility monopolies, where a single enterprise undertook generation, transmission, distribution, and retail supply (Figure 1). Electricity tariffs were primarily determined using a cost-plus model, with accounting covering elements such as fuel, depreciation, operations and maintenance, and the rate of return on capital [12]. For reasons of universality and political acceptability, regulators typically approved a uniform average cost of electricity, while implementing cross-subsidization between residential and industrial/commercial users through fixed discounts or surcharges [13].

This model reflected the principle of “uniform pricing with cost recovery,” but did not differentiate between ToU periods, meaning that consumers paid the same price during peak and off-peak hours. As a result, retail tariffs exhibited a “flat and uniform” characteristic. Because marginal costs were largely disconnected from end-user prices, the demand side lacked incentives for conservation. System planners thus relied heavily on capacity expansion strategies based on “peak load high reserve margins,” which led to the large-scale deployment of coal-fired and nuclear baseload plants as the dominant means of ensuring supply reliability [15–17].

Under these conditions, the absence of demand-side behavioral incentives, the inefficiency of network investment, and the deadweight losses associated with monopoly structures became increasingly apparent, constraining the optimal allocation of electricity resources. Meanwhile, the lack of flexible price signals widened the peak-to-valley gap in load curves, laying the groundwork for subsequent reforms introducing ToU and dynamic pricing [18].

Table 2 Main tariff types

| Time of Energy | Energy/Power | Smart | |||

| No. | Tariff Name | Consumption Dependency | Dependency | Meters | Equation |

| 1 | Simple or uniform tariff | independent | (Energy-based) | Not needed | TC = C |

| 2 | FR | independent | (Power-based) | Not needed | TC = A * x |

| 3 | Straight-line meter rate tariff | independent | (Energy-based) | Not needed | TC = B * y |

| 4 | Increasing/Block meter rate tariff | independent | (Energy-based) | Not needed | C1, 0 t1 t2 |

| C2, t2 t t3 | |||||

| 5 | Two-part tariff | independent | (Energy- and power-based) | Not needed | TC = A * x + B * y, |

| 6 | Seasonal rate tariff | independent | (Energy-based) | Not needed | TC = B * y max. (yearly) |

| 7 | Peak-load tariff | independent | (Energy-based) | Not needed | TC = B * y max. (Same as Equation (6) but calculated on daily basis) |

| 8 | Three-part electricity tariff | independent | (Energy- and power-based) | Not needed | TC = A * x + B * y + C |

| 9 | Power factor tariff | independent | Power-based | Not needed | – |

| 10 | Tiered (or step) Tariff | independent | (Energy-based) | Not needed | TC = Bn * y |

| 11 | Tiered/TOU | dependent | (Power-based) | needed | TC = An * x |

| 12 | Demand rates | independent | Power-based | Not needed | TC = A * x max |

| 13 | Weekend/holiday rates | independent | (Energy-based) | Not needed | TC = Bn * y. (Same as Equation (8) but calculated on weekends and holidays) |

| 14 | FIT | independent | (Energy-based) | Not needed | – |

| 15 | Net metering | independent | (Energy-based) | Not needed | – |

| 16 | Critical peak pricing | dependent | (Energy-based) | Needed | TC = An * x. (Same as Equation (9) but time intervals are longer) |

| 17 | Real-time pricing | dependent | (Energy-based) | Needed | – |

| /Dynamic pricing | |||||

| 18 | Two-part real-time pricing (Block- and-Index Pricing | dependent | (Energy-based) | Needed | TC = An * x + extra charges (Same as Equation (9) but extra charges are added.) |

| 19 | Sell back | dependent | (Energy-based) | Needed | – |

| No. | Tariff Model | Structural Features | Risk-Sharing Mechanism | Typical Application | |

| 2 | Fixed Price Plans | Single rate or fixed monthly bill | Retailer bears price volatility | Users valuing bill stability | |

| 3 | Time-of-Use (ToU) | Peak/off-peak differentiation | Users adjust usage by time | Load shifting; storage integration | |

| 4 | Real-Time Pricing (RTP) | Direct pass-through of wholesale prices | Users exposed to short-term volatility | Flexible, tech-enabled households | |

| 5 | Hybrid Subscription + Dynamic Pricing | Fixed monthly subscription plus variable component | Partial risk sharing | Rapidly expanding in Nordics & Australia | |

| 6 | EV Charging Plans | Super off-peak prices; controlled charging; V2G incentives | Algorithmic allocation of charging risk | Home charging, fleet charging, V2G pilots | |

Figure 1 (a) Monopoly model; (b) single-buyer model; (c) Wholesale market model; (d) Retail electricity model [14].

2.2 Market-Oriented Reform and the Two-Part Tariff Period (1990s–2000s)

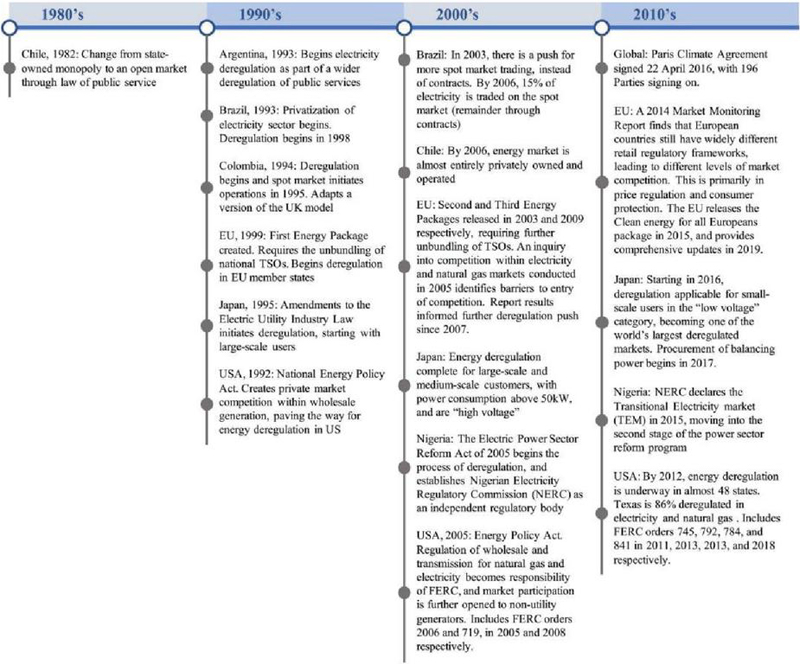

During the 1990s, numerous countries began to restructure their power sectors, as the EU, Japan, and the United States initiated long-delayed efforts to unbundle vertically integrated utilities, a process illustrated in the global timeline shown in Figure 2. These reforms began with the unbundling of generation, transmission, distribution, and retail services, accompanied by the establishment of Independent System Operators (ISOs) or Transmission System Operators (TSOs). Subsequently, competitive mechanisms such as wholesale bidding and capacity auctions gradually shaped market-based wholesale prices [19, 20].

Figure 2 A brief history on the deregulation of electricity markets throughout the world [21].

On the retail side, in order to balance price signals with revenue stability for utilities, a “two-part tariff” structure was widely introduced, combining a demand (capacity) charge with an energy (volumetric) charge. The demand charge was typically calculated according to the customer’s maximum demand (kW) or meter capacity (kVA) and was intended to cover the fixed costs of the network. The energy charge was often designed as an Inclining Block Tariff (IBT), whereby the marginal price increased with higher consumption blocks. This structure both conveyed scarcity signals to large consumers and imposed economic constraints on energy-intensive behaviors, serving as an early tool to encourage energy conservation and demand-side management [22].

In addition, the demand charge provided utilities with a stable cash flow, enabling them to maintain investment ratings and raise capital even in the face of demand fluctuations and wholesale price uncertainty. This mechanism was therefore important in securing the reliability of transmission and distribution networks [23].

Tariff design varied across countries depending on national circumstances, with differences in applicable customer groups, voltage levels, and complementary pricing mechanisms (Table 3). Despite such diversity, certain common features could be observed. In terms of applicability, the two-part tariff was often extended to both residential and commercial/industrial users. As for complementary tariff mechanisms, utilities typically allocated transmission and distribution costs by voltage level, and then introduced additional measures such as ToU pricing, seasonal tariffs, load factor–based packages, or utilization-hour charges within each voltage category. Furthermore, differentiated strategies were adopted according to customer load characteristics, ensuring that the tariff structure could meet the needs of diverse user groups.

Table 3 Comparison of two-part electricity pricing practices in France, the United States, and Japan

| Country | User Type | Electricity Price | System Voltage Level | Auxiliary System |

| US | residential users | Two-part system | three levels | peak-valley ToU, seasonal ToU, and load rate package |

| Industrial and commercial users | Three-part system | three levels | ||

| France | residential users | Two-part blue electricity rate | Low voltage | Seasonal time sharing, peak and valley time sharing, and utilization hours |

| Farmer users | Two-part yellow electricity rate | Low voltage | ||

| Industrial and commercial users | Two-part green electricity rate | Medium and high voltage | ||

| Japan | Business users | Two-part system | No rating | Seasonal electricity prices, segmented electricity prices, electricity charges and load adjustments |

| Various medium and high voltage users | Two-part system | Medium voltage has three ratings, high voltage has five ratings |

2.3 The Era of Smart Metering and ToU Pricing (2010s)

During the 2010s, the large-scale deployment of Advanced Metering Infrastructure (AMI) significantly increased the frequency of electricity data collection, shifting from monthly billing cycles to minute- or even second-level intervals. This technological breakthrough provided a robust foundation for the practical implementation of ToU tariffs [24].

Representative cases include France’s EDF Tempo package, which classifies days into three types – red, white, and blue – and combines them with peak and off-peak periods to form six pricing tiers. On 22 extreme peak days, the “red peak” tariff can reach six to eight times the normal price, thereby strongly incentivizing consumers to shift demand away from peak periods [25]. Italy’s Bioraria tariff, in contrast, adopts a simpler two-block structure, with “F1” (08:00–19:00 on weekdays) and “F2” (all other periods), enabling effective load shifting [26]. In South Korea, KEPCO introduced three- or four-block ToU pricing for commercial users, complemented by demand-control reward mechanisms, which enhanced corporate participation in peak load management [27].

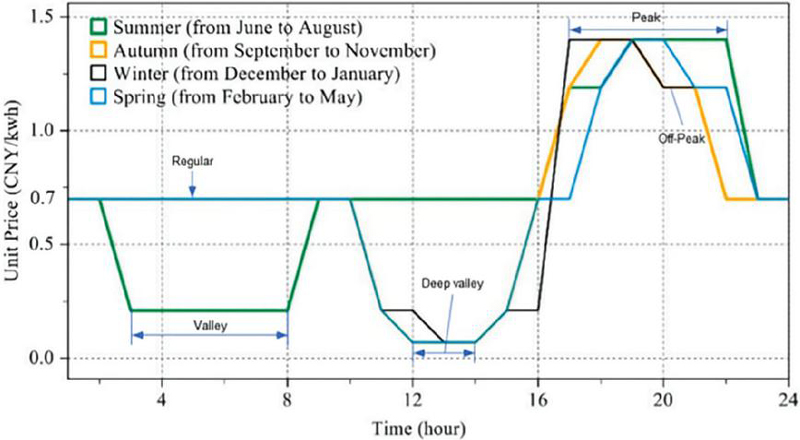

Beyond improving the granularity of measurement and billing, smart metering systems have also provided essential data support for dynamic tariff design, energy feedback, and demand response [28]. Studies demonstrate that the integration of AMI with ToU pricing can effectively facilitate multi-layered task scheduling and coordinated electricity supply (Figure 3), while enabling demand-side flexibility through home automation and real-time energy feedback [29]. A large body of empirical evidence further shows that, when paired with smart control devices, ToU pricing has achieved peak load reductions of 5%–15% across different countries and regions, underscoring the significant potential of combining AMI with ToU tariffs [30].

Figure 3 Seasonal ToU electricity prices on the main grid.

2.4 The Era of Digitalization and Real-Time Pricing (2020s–Present)

Entering the 2020s, the maturation of digital technologies such as cloud computing, the Internet of Things (IoT), machine learning, and mobile payment has enabled electricity retailers to transmit wholesale market price signals directly to end-users at hourly or even 15-minute granularity [31]. At the same time, the high-frequency volatility of wholesale prices driven by renewable energy penetration has created fertile ground for the innovation of differentiated retail packages.

Nordic suppliers such as Tibber and Fortum pioneered the “Wholesale Pass-Through + Zero Commission” model, under which users pay only a monthly platform fee while directly bearing real-time wholesale prices [32]. In the ERCOT market in Texas, companies such as Griddy and Octopus Energy US leveraged APIs to deliver settlement data to mobile applications in real time, enabling household appliances to be automatically scheduled via tools like IFTTT and Home Assistant [33]. In Germany and the United Kingdom, retailers further explored hybrid “Fixed Subscription + Spot Float” billing structures, in which a portion of consumption is bundled into a fixed monthly fee, while any excess is billed at real-time prices. This approach balances predictability for consumers with the transmission of market-based price signals [34].

Real-time pricing mechanisms are typically based on real-time supply–demand conditions in the grid, marginal generation costs, and carbon emission factors, with prices published at the start of each time interval. This not only facilitates effective peak shaving and valley filling but also incentivizes users to shift consumption toward low-price periods, thereby reducing system balancing pressures [35]. Empirical studies indicate that, when combined with smart homes, storage systems, and EV charging schedules, real-time pricing can achieve peak load reductions of 10%–20% [36].

Moreover, real-time tariffs in user-side microgrids are generally lower than settlement prices in the main grid, allowing consumers to purchase electricity at a lower cost while simultaneously reducing the marginal supply costs for retailers. This creates a mutually beneficial arrangement between end-users and suppliers [37]. Recent research further reinforces this conclusion, highlighting that real-time pricing based on grid conditions, marginal generation costs, and carbon intensity not only optimizes system operations but also strengthens demand-side participation in energy flexibility [38, 39]. In the context of rapidly expanding distributed energy and smart technologies, the observed gap between microgrid and wholesale real-time prices demonstrates the dual benefit of consumer cost savings and reduced supply-side costs, thereby reinforcing a mutually advantageous structure for both consumers and retailers [40].

3 Institutional Practices in Major Countries and Regions

3.1 The Practice of Retail Tariff Packages in the Australian Market

Australia began implementing electricity market reforms in the 1990s, making it one of the earliest countries to pursue restructuring in this sector. Given the relatively small scale of its overall market, most electricity retailers operate across state boundaries. Retailers have developed a variety of retail tariff packages based on different dimensions, with the most common being flexible tariffs and ToU tariffs. In addition to standard supply services, many retailers also offer value-added services for consumers to choose from [41].

Research on tariff practices in Australia covers several dimensions, including consumer responses to different tariff schemes and the policy impacts on market outcomes. Doojav and Kalirajan examined the price and income elasticity of electricity demand across Australian states and highlighted the significant heterogeneity across regions [42]. In recent years, with further liberalization of the electricity market and the widespread rollout of smart meters, ToU tariffs have received increasing attention. Burns and Mountain analyzed 6,957 household electricity bills in Victoria and found that, although ToU tariffs offered consumers opportunities to lower costs by shifting demand to off-peak periods, consumer responses to peak–off-peak price differentials were weak. This was especially true among households with lower socioeconomic status, where little or no behavioral adjustment was observed. These findings suggest that while market liberalization and technological progress created the conditions for wider adoption of ToU tariffs, their effectiveness in changing consumer behavior has been limited [43].

Esplin et al. further revealed that electricity retailers often impose higher prices on loyal customers – a practice referred to as the “loyalty tax.” This form of price discrimination has been observed not only in Australia but also in other liberalized markets such as the United Kingdom. Low-income consumers are particularly disadvantaged, as they face greater barriers to accessing market information and higher transaction costs when switching suppliers, making them more likely to pay the loyalty tax. The study underscores the need for policymakers to address the economic burden faced by vulnerable groups in the electricity market [44].

3.2 The Practice of Electricity Price Packages in the US Retail Market

The electricity market in Texas is one of the most prominent examples of power market liberalization in the United States. Operated under the guidance of the Electric Reliability Council of Texas (ERCOT), the retail market is subject to strict oversight by the Public Utility Commission (PUC), which ensures fair competition and price transparency through regulatory mechanisms.

Texas retailers offer a wide variety of tariff packages and value-added services. The most common tariff options include fixed-price contracts, ToU tariffs, and usage-based variable pricing plans. For most retail contracts, electricity is billed on a monthly basis, although prepaid electricity services are also available [45]. The Texas retail electricity market is highly competitive, and retail tariffs are typically lower than the U.S. average. However, during periods of natural gas price volatility or extreme weather events, prices have occasionally exceeded the national average. In competitive market segments, retail electricity reform has reduced retailer costs, while in non-competitive segments – such as those served by municipal utilities or cooperatives – these cost reductions have not materialized [46].

In terms of consumer behavior, the Texas market demonstrates significant consumer inertia. Despite the availability of multiple tariff packages and often lower-price offers from alternative suppliers, many consumers tend to remain with their default electricity provider. Research shows that preferences for incumbent providers are shaped not only by price but also by non-price factors such as service quality, as well as by search costs and switching costs [47].

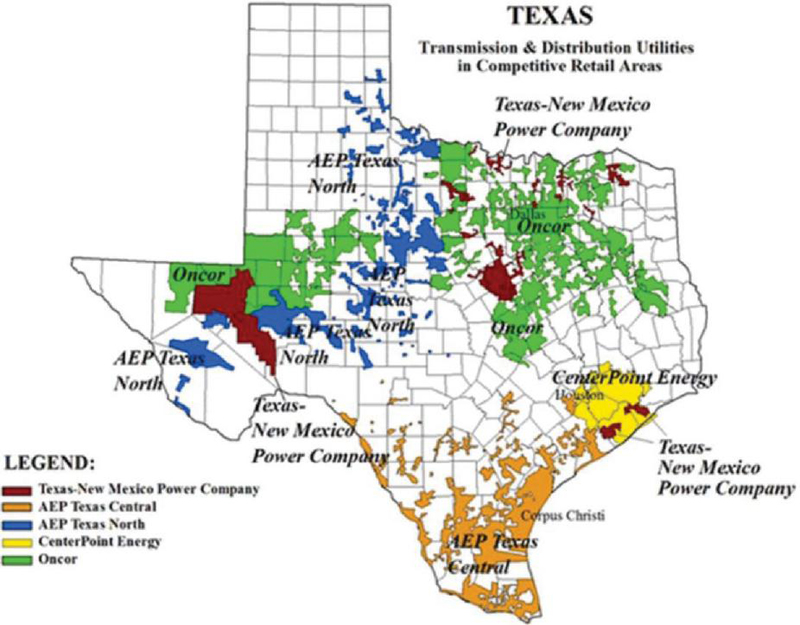

Texas implemented retail electricity competition in 2002 under Senate Bill 7, allowing new entrants to compete with the retail divisions of five former monopoly utilities in ERCOT service areas, including Dallas and Houston. However, markets in Austin, San Antonio, El Paso, and other non-ERCOT regions remained closed due to municipal ownership or jurisdictional boundaries, these service areas, identified in Figure 4.

Figure 4 Areas initially opened to retail competition.

Source: PUCT at: https://www.puc.texas.gov/industry/maps/maps/tdumap.pdf.

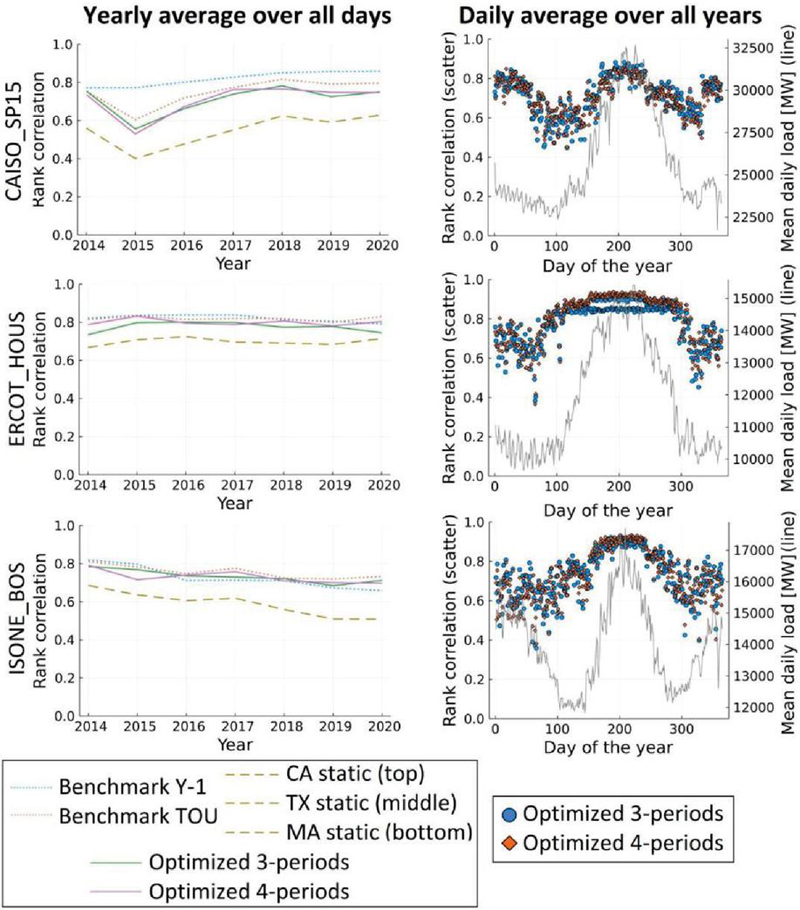

Figure 5 reports the daily average Spearman rank correlation between residential TOU and day-ahead/spot prices at three major US wholesale nodes (CAISO-SP15, ERCOT-Houston, and ISO-NE Boston) from 2014 to 2020. The results show that, with the exception of a few rare price days, the correlation remains stable at the annual average level. Superimposing TOU on CPP barely changes the correlation, indicating that static TOU prices can anchor typical wholesale signals but have limited coverage of extreme market conditions. In contrast, China is enhancing the coupling of retail and system flexibility through VPPs and behind-the-meter/standalone energy storage in ancillary services (which can be connected to the aforementioned Guiyang joint simulation case) [48].

Figure 5 Yearly averaged daily Spearman rank correlations between retail TOU rates and day-ahead prices (left) and daily correlations with spot prices (right) across CAISO SP15 (top), ERCOT Houston Hub (middle), and ISO-NE Boston (bottom), 2014–2020; adding CPP yields nearly identical results, as scarcity events occur on only a few days per year [49].

3.3 The Practice of Retail Tariff Packages in the United Kingdom

Since the 1990s, the United Kingdom has gradually advanced electricity market liberalization, making it one of the earliest and most thoroughly liberalized electricity markets in the world. The UK government has relied on regulatory mechanisms to safeguard fair competition and price transparency. Ofgem, the Office of Gas and Electricity Markets, plays a central role in this process by imposing price caps and promoting market openness, thereby protecting consumer interests while fostering competition.

In the UK retail market, tariff structures generally combine two-part pricing with ToU options. This means that electricity bills include both capacity charges and energy charges. According to Ofgem’s survey findings, overly complex tariff structures and the shortage of qualified retailers significantly undermine market competitiveness. As a result, most UK suppliers primarily offer two types of packages – fixed-price tariffs and variable-price tariffs – with multiple forms of pricing possible under each model [50]. These tariff products are designed to accommodate diverse consumer preferences and consumption behaviors. Nevertheless, consumers often face challenges such as information asymmetry and high search costs when choosing among competing offers. With the progressive rollout of smart meters, however, retailers are now able to analyze consumption patterns with greater precision and design more targeted tariff products.

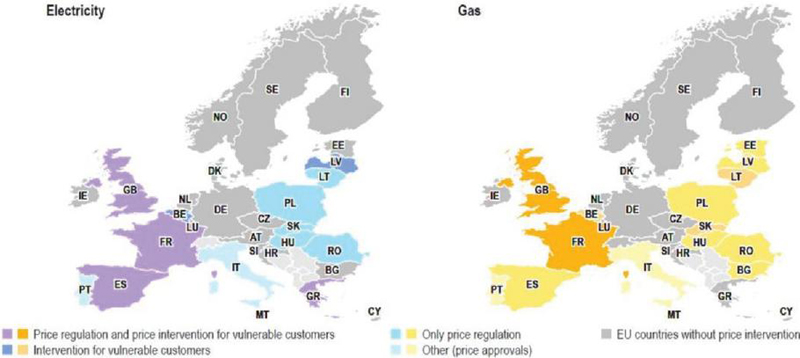

In 2020, as shown in Figure 6, the UK was finalizing its exit from the European Union while also undergoing significant changes in its electricity retail market. Although the UK had been the first European country to fully liberalize electricity supply, the government reintroduced a broad price cap after the 2016 Competition and Markets Authority (CMA) inquiry to protect customers of the Big Six suppliers. This move toward re-regulation has sparked heated debate, with both the CMA’s assessment and the price cap itself facing considerable criticism in academic and policy circles.

Figure 6 Existence of price intervention in electricity and gas in 2018. Source: ACER/CEER.

Leading firms such as British Gas leverage brand trust and economies of scale to introduce sophisticated tariff packages that bundle renewable energy options and integrated energy services, targeting consumers who value stability and additional services. In contrast, smaller suppliers typically pursue “flexible pricing” strategies, offering simpler packages such as ToU tariffs or dynamic discount models to appeal to price-sensitive customers. This differentiation – “large incumbents with complex packages” versus “small challengers with flexible offerings” – illustrates the alignment between market position and consumer segmentation. Large incumbents use scale advantages to build service barriers, while smaller suppliers rely on agility to address niche demand. Together, they provide an intuitive case study of how “competitive structure and tariff design” interact in retail electricity markets [51].

3.4 The Practice of Retail Tariff Packages in Japan

Japan initiated electricity market reforms in the 1990s, completing a 16-year process that culminated in the full liberalization of the retail electricity sector [51]. The Japanese government promoted transparency and fair competition through a series of regulatory policies.

Retailers in Japan have developed a wide range of tariff packages tailored to different consumer segments, along with various value-added services. Major tariff options include inclining block tariffs, ToU tariffs, and weekend discount packages designed for office workers. However, consumers often face information asymmetry and high search costs when selecting among these options, which constrains their ability to identify and switch to more favorable packages [52].

Following the complete liberalization of both the electricity and urban gas markets, bundled sales strategies – combining electricity with gas or other services – have become highly popular. Reiko (2022) conducted an empirical study on the impact of such bundling strategies on consumer switching behavior in Japan’s retail energy market. The findings suggest that bundling increases consumer switching costs and thereby reduces the likelihood of switching to alternative suppliers [53].

3.5 The Practice of Retail Tariff Packages in China

Since the issuance of the landmark “Document No. 9” in 2015, which established the framework of “controlling the middle, liberalizing both ends,” pilot provinces such as Guangdong and Zhejiang took the lead in introducing two foundational products: peak–valley ToU tariffs and tiered pricing packages. In 2021, the National Development and Reform Commission released the Notice on Further Improving the ToU Pricing Mechanism, requiring regions to scientifically define peak and off-peak periods and rationally determine price differentials. This policy strengthened the linkage between ToU tariffs and the spot market, giving rise to hybrid packages such as “fixed price + floating share.” For instance, Jiangsu Province launched the E-Power Contract, which combines fixed rates with spot market-based adjustments to improve efficiency in risk sharing.

Since 2015, research on tariff design and consumer behavior has deepened. Empirical analyses confirmed that acceptance of ToU tariffs depends on multiple factors, including tariff complexity, sensitivity to price volatility, and market information transparency, while ToU mechanisms have been shown to incentivize households to shift consumption to off-peak periods, thereby improving overall system efficiency [54]. Building on this, combined peak–valley designs were proposed to encourage boundedly rational users to proactively adjust their electricity use, which not only increased trading revenues but also enhanced service precision [55].

New modeling approaches have further emphasized consumer-oriented optimization. One line of work constructed user load-shifting models and applied a novel GO heuristic algorithm to solve the retailer’s optimization problem. Simulations based on utility company data demonstrated that this approach strengthened retailer competitiveness by incorporating user utility and choice behavior into revenue modeling. In parallel, behavioral analyses using the Technology Acceptance Model (TAM) revealed that user attributes and product characteristics jointly shape retail tariff preferences, and that multidimensional drivers significantly influence business interaction models in the retail market [57].

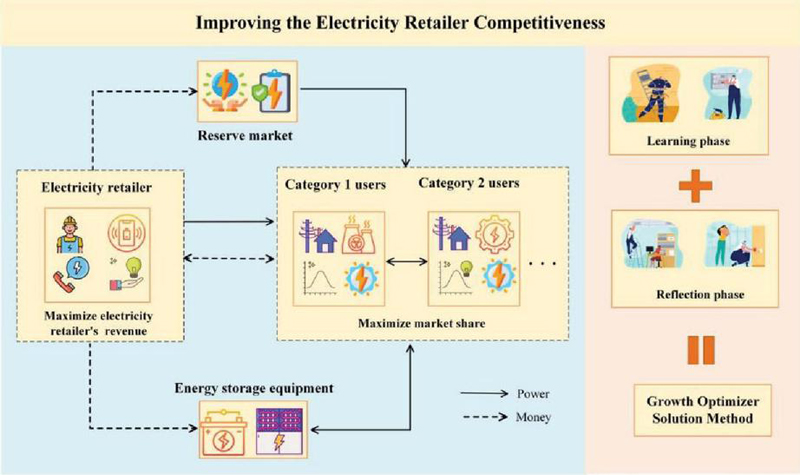

To further optimize competitiveness, retailers must accurately determine user demand, design reliable service price parameters, and align them with both profit maximization and customer retention. A decision-making model based on TOPSIS has been developed for this purpose, targeting the dual objectives of revenue maximization and market share expansion. The GO optimization algorithm, with its learning–reflection iterative process, enables global optimization within this framework. As illustrated in Figure 7, this approach provides a systematic pathway for retailers to enhance competitiveness while meeting user needs.

Figure 7 Schematic diagram of improving the competitiveness of electricity retailers [56].

To facilitate cross-country comparison and to highlight structural heterogeneity across institutional contexts, Table 4 synthesizes the key features of retail pricing models in representative markets, including pricing structures, regulatory instruments, customer segmentation strategies, and the degree of digitalization. The comparative overview illustrates how mature markets emphasize dynamic and hybrid tariff innovations enabled by smart metering and flexible regulation, whereas emerging markets continue to rely more heavily on lifeline tariffs, cross-subsidies, and administratively guided price formation. This consolidated perspective helps clarify the institutional pathways through which different jurisdictions pursue cost-reflectiveness, risk allocation, and equity objectives.

Table 4 Comparative overview of retail pricing models in representative markets

| Dominant | Regulatory Tools | Customer | Digital | |

| Country/Region | Tariff Types | & Oversight | Segmentation/Targeting | Infrastructure Maturity |

| Australia | TOU tariffs, flexible tariffs, subscription add-ons | AER oversight, retail competition rules, consumer protection guidelines | Segmentation based on socio-economic groups; optional smart-meter-enabled plans | High AMI penetration in Victoria; uneven across other states |

| United States (Texas / ERCOT) | Fixed price, variable price, real-time/ wholesale pass-through, prepaid electricity | PUCT oversight; market-based competition; price-cap mechanisms during scarcity | High heterogeneity; optional EV plans; inertia due to search/ switching costs | Advanced smart-meter rollout; extensive API-based tools from retailers |

| United Kingdom | Fixed tariffs, standard variable tariffs, TOU and CPP pilots | Ofgem price cap, supplier licensing, market transparency mandates | Large suppliers offer bundled/ green packages; smaller firms emphasize flexible pricing | National smart-meter rollout in progress; growing dynamic-tariff pilots |

| Japan | Tiered pricing, TOU, weekend/ lifestyle packages; bundled electricity–gas | METI oversight; consumer switching rules; capacity cost adjustments | Strong segmentation by household type, lifestyle, and bundled energy services | Advanced metering; V2G and home-energy-management integration |

| China | TOU tariffs, tiered pricing, fixed + floating hybrid packages | NDRC regulation, provincial pilots, gradually expanding spot-market linkage | Industrial/ commercial segmentation; emerging EV-specific pricing pilots | Rapid AMI deployment; strong utility-driven digital platforms |

| Country / Region | Dominant Tariff Types | Regulatory Tools & Oversight | Customer Segmentation / Targeting | Digital Infrastructure Maturity |

4 Core Design Mechanisms of Retail Tariff Packages

4.1 Marginal Cost Reflection

At the heart of retail tariff package design lies the principle of marginal cost reflection, which seeks to transmit generation, transmission, and environmental costs accurately to end-users. This mechanism enables efficient resource allocation and guides demand-side responses. Marginal-cost-based pricing, rooted in long-term system planning, distinguishes between capacity costs and energy costs, and employs structures such as ToU tariffs and two-part tariffs to reflect the cost differentials of supply across time periods and voltage levels.

4.1.1 Energy charges

Short-term marginal costs in electricity systems are generally composed of three elements: energy costs, which include the fuel and variable operating and maintenance expenses of the marginal generating unit; congestion costs, which reflect the shadow prices of transmission constraints; and loss costs, associated with marginal transmission losses [58]. Within this framework, energy charges represent the real-time fuel and O&M expenditures of generation. Evidence from theoretical and applied studies suggests that marginal-cost-based real-time pricing, when supported by smart metering infrastructure, can reduce peak demand by approximately 12%–18% [59].

The implementation of such pricing mechanisms requires advanced metering and data management infrastructure. High-performance servers, redundant database systems, and secure storage arrays ensure data integrity, while GPS-synchronized front-end processors provide millisecond-level accuracy. Combined with high-speed communication networks and indexing optimization, these systems significantly enhance the efficiency of database management, statistical reporting, and settlement processes, thereby supporting precise energy measurement and billing [60]. Moreover, as renewable penetration rises, particularly when wind and solar exceed 30% of total generation, an additional volatility premium becomes necessary to cover reserve and balancing costs, preventing the externalization of system risks [61].

4.1.2 Capacity charges

Cramton and Stoft (2006), in The Design of Markets for Generation Capacity Adequacy, argued that capacity market design must avoid the “missing money” problem, emphasizing that long-term marginal costs must fully cover the fixed costs of capacity investment. This includes capital recovery for generation units, grid expansion costs, and reliability insurance, with capacity charges ideally accounting for 28%–35% of retail tariffs to ensure long-term adequacy [62].

According to Wang Yongping et al. (2020) from Shenzhen Power Supply Bureau, the “contracted capacity + actual demand” dual-track design (35 RMB/kW·month) reduced redundant expenditures for industrial users by 12% and improved equipment utilization by 15% [63]. More recently, Zhang Hongji (2024) addressed the challenge of cost recovery for pumped-storage power plants under renewable integration. He developed a joint pricing model that considers both spot and ancillary services markets, proposing a VCG-based cost allocation mechanism grounded in utility proportion. Simulation results showed that this method effectively covered plant costs and provided a fair basis for market-based pricing of pumped storage [64].

4.1.3 Environmental and policy surcharges

Environmental and policy add-ons – such as carbon-intensity-based surcharges, renewable consumption incentives, and policy-driven renewable funds – serve both to incentivize low-carbon electricity use and to internalize the externalities of carbon-intensive loads. Research by Pang Jun, Song Peng, and Chen Qixin indicated that mandatory green certificate trading could substitute for feed-in tariff subsidies but deliver only limited carbon reduction effects. Moreover, renewable subsidies tended to depress carbon prices, requiring “stepwise tightening of total caps” to mitigate distortions, alongside the establishment of a “green premium transmission mechanism” [65–67].

Germany, as an industrial powerhouse, has long prioritized climate action and decarbonization, spearheading the Energiewende with the target of achieving near carbon neutrality by 2045. Legally, the country enacted and repeatedly revised the Renewable Energy Act (covering feed-in tariffs, subsidies, and grid access), introduced the National Hydrogen Strategy and related action plans, and in 2022 passed a comprehensive package of energy transition laws. These policies have driven impressive results: by 2023, renewables accounted for more than 50% of total electricity consumption – an increase of 5.6 percentage points over 2022 – while installed renewable capacity grew by 12%. However, challenges persist, including the fiscal burden of subsidies pushing up retail prices, intermittency-induced grid balancing pressures, delayed storage deployment, and project approval bottlenecks in certain regions [68, 69].

4.2 Risk Sharing and Hedging

4.2.1 Subscription-based packages

Subscription-based packages adopt a “fixed monthly fee + variable usage fee” model, transferring part of the price volatility risk from consumers to retailers. The design principle is that market price risk is borne by retailers, who rely on their expertise in forecasting and risk management to hedge in wholesale markets using financial instruments such as electricity futures and options. This creates a mechanism of secondary risk transfer. According to O’Connell, Chief Product Officer of Octopus Energy, in the empirical study UK Household Demand-Side Response, the “subscription-based models + floating energy charge” model (£20 per month) allowed users to save an average of £142 annually, with a contract renewal rate of 92% [70].

Similarly, in the mobility sector, Li Bin of NIO proposed the Battery-as-a-Service (BaaS) subscription model, which separates the battery from vehicle ownership (battery leasing + energy charges). This approach significantly reduces the upfront cost of EV purchases while ensuring consumer affordability and system flexibility [71].

4.2.2 Price collar design

Price collars are designed by setting upper and lower bounds on retail electricity tariffs, providing a “safety valve” against extreme price fluctuations. When market prices fall below the lower bound, consumers pay the actual lower price; when they rise above the upper bound, the retailer absorbs the excess cost; within the set range, consumers pay according to market prices. Demand-side management programs based on this principle allow consumers to respond to price signals at different times, thereby reducing their electricity bills [72].

The underlying logic is that retailers and consumers agree on a risk-sharing arrangement, while retailers hedge extreme risks by purchasing insurance products or establishing risk reserves. This protects consumers from exposure to extreme market volatility while maintaining a viable profit margin for retailers. Guo Ye et al. (2022) further proposed a dynamic adjustment algorithm based on a 70% load factor threshold, which enables adaptive tariff adjustments under varying system conditions [73].

4.3 Fairness Adjustment

4.3.1 Social tariff mechanisms

Current electricity pricing systems in many regions are characterized by fragmented classifications, relatively low tariff levels, dispersed regulatory authority, and persistent cross-subsidies – all of which hinder efficient allocation of power resources [74]. Establishing a market-oriented pricing mechanism is therefore critical. This includes advancing market reforms, improving forecasting of consumption for agency-purchase users with regular deviation reporting, and designing targeted subsidy transmission pathways to safeguard the electricity rights of low-income households through cross-subsidization.

Fabra, Professor of Economics at the University of Barcelona, analyzed France’s four-tier regressive tariff subsidy, showing that it reduced electricity burdens for low-income households by 18% [75]. In China, Lin Boqiang of Xiamen University (2020) revealed striking disparities in regional subsidy allocations, reaching 87.5% (15 kWh/month in Guangdong vs. 8 kWh/month in Yunnan) [76]. Meanwhile, electricity trading centers are strengthening their platforms to monitor market and price changes in real time. Internationally, measurement approaches also diverge across sectors: linear metering dominates in public service areas, while block tariffs are more prevalent in residential consumption. With the rise of digital technologies, classical modeling tools can now be combined with big data to design more equitable and transparent social tariff systems [77].

4.3.2 “Better offer” disclosure

The “better offer” mechanism enhances fairness in consumer choice by improving information transparency. Giulietti, Professor at the University of Warwick, in Consumer Switching Behavior in European Energy Markets, demonstrated that the UK’s mandatory disclosure of the Annual Potential Saving Statement (APSS) – showing potential yearly savings on bills – led 38% of consumers to switch to cheaper plans [78].

Building on this logic, joint bidding models that incorporate multiple risk factors have been proposed to optimize retail electricity offers. Such models can quantify the risk preferences of generators, enabling risk-managed participation in both energy and ancillary service markets. By addressing the inefficiencies and instability of traditional pricing systems, these optimized models enhance tariff strategies, ensuring effective peak shaving and valley filling while improving overall system efficiency [79].

4.4 Digital Foundations

4.4.1 Smart metering

High-frequency data collection has become the cornerstone of modern demand-side response and dynamic billing, providing the granularity necessary for distributed resource aggregation and virtual power plant (VPP) scheduling. The effectiveness of ToU pricing is contingent upon access to interval data at scales of 15 minutes or less, which enables both accurate measurement and real-time adjustment of user consumption [80]. In China, the development of a “metering cloud” architecture has reduced system fault response times to within 15 minutes, significantly enhancing reliability [81]. Nationwide deployment has also reached unprecedented scale: with more than 500 million smart meters in operation, the system generates approximately 480 terabytes of new data each day, though less than 20% of this information is currently leveraged for operational or market optimization purposes [82].

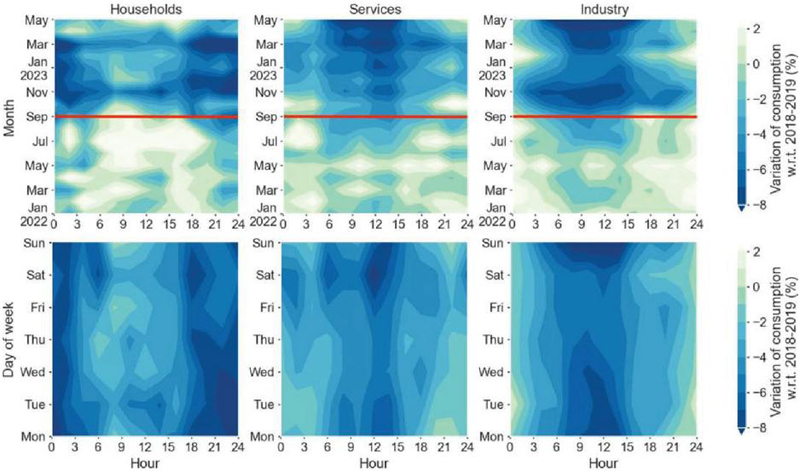

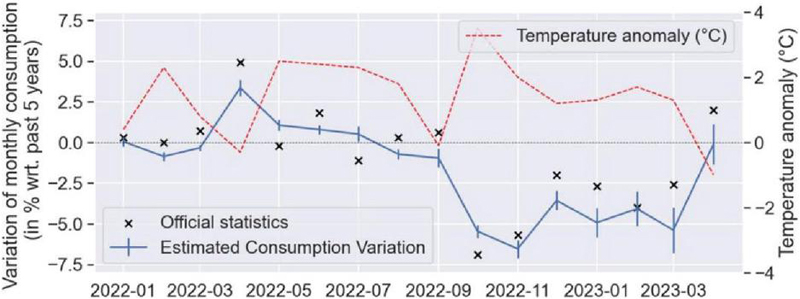

The responses of different categories of consumers to energy-saving activities vary with temperature, time of day, and day of the week (Figure 8). Recent empirical evidence further demonstrates the value of smart metering: Figure 5 from a Swiss case study shows that electricity savings estimated from real-time meter data closely matched official SFOE statistics, capturing a winter reduction of 4.9% compared to the reported 3.9%, thus validating the reliability of smart meter–based national consumption assessments (Figure 9) [83].

In addition, simulation studies based on the HELICS platform have developed a co-simulation framework for interactive energy markets that integrates multiple systems and models. Results indicate that a double-blind auction mechanism enabled 40% of users to achieve higher revenues than under net metering policies, while simultaneously increasing distribution company income by 3%. This framework provides a quantitative analytical tool for the design of distribution-level electricity markets [84].

Figure 8 Cross-sectional view of relative electricity consumption (%). The figure reports the estimated hourly changes in electricity use compared with the 2018–2019 reference period. Values are expressed as percentages and cover households, services, and industry, shown against months (top row) and days of the week (bottom row). The bottom row uses the 2018–2019 winter (October to March) as the reference period. The red line marks the dates of energy-saving campaigns.

Figure 9 Monthly variation in national electricity consumption. The estimated consumption values (blue line), derived from smart meter data without weather adjustments, are compared with the official SFOE statistics (black crosses). Vertical bars indicate the 95% confidence interval for each observation. Deviations from long-term temperature norms are represented by the red dashed line [83].

4.4.2 Open APIs and data authorization

Open data-sharing mechanisms break the monopolistic control of retailers over user data and promote third-party service innovation. Article 8 of the EU Data Act requires energy companies to provide standardized API interfaces. Similarly, Tencent Cloud and China Southern Grid’s Energy Operating System 3.0 White Paper announced the release of 12 API categories, and after integrating with nine automotive companies, the number of third-party applications increased by 300%.

However, data privacy protection is the cornerstone of open API development. Under the EU’s General Data Protection Regulation (GDPR), energy consumption data may only be shared with “explicit consumer consent,” highlighting the balance between openness and privacy in digital energy ecosystems.

4.4.3 Personalized energy insights

Personalized tariff recommendations based on users’ historical consumption data can mitigate information asymmetry and reduce market inefficiencies. By integrating data from multiple electricity subsystems into unified architectures and applying advanced analytical models, personalized insights support multi-stakeholder decision-making and operational efficiency improvements, thereby accelerating the digital and intelligent transformation of electricity markets [84].

For example, a report from State Grid Jiangsu Power showed that personalized “energy health reports” reduced household electricity consumption by 8.2% and lowered peak air conditioning load by 19% [85]. Similarly, the “Power Big Data Laboratory” of State Grid Zhejiang developed a “Household Energy Efficiency Optimization” service that analyzes large-scale user consumption patterns and provides customized efficiency plans, achieving an average energy savings rate of 8.7% [86].

4.5 Consumer Response and Distributional Effects

4.5.1 Peak load reduction effects

A substantial body of research shows that real-time and dynamic pricing can effectively reshape electricity consumption by signaling users to shift their load, thereby achieving peak shaving, valley filling, and overall grid optimization. By setting higher tariffs during peak hours and lower tariffs during off-peak periods, consumers are incentivized to adjust their electricity use accordingly [87]. Within demand response programs, reinforcement learning methods have been applied to construct price-generation functions that take into account market and capacity constraints. Using proximal policy optimization algorithms, aggregators are able to optimize strategies that maximize profits while reducing system peak load [88]. Under ToU pricing schemes, higher-income consumers with flexible schedules are often more willing to shift the operation of energy-intensive appliances from peak to off-peak periods [89].

4.5.2 Income differences and adoption rates

Adoption of dynamic pricing packages is strongly correlated with household income. High-income groups typically possess a greater proportion of smart appliances and enjoy more flexible schedules. As a result, they are less economically sensitive to price volatility and instead place higher value on convenience and environmental benefits, making them more likely to choose green and flexible tariff options [90]. Conversely, low-income groups are constrained by high upfront costs and barriers to retrofitting rental housing, which limit their ability to adjust consumption. Their heightened sensitivity to electricity expenses, coupled with limited access to market information, further restricts timely adoption of favorable tariff offers [91].

4.5.3 Regulatory intervention and fairness safeguards

Consumer responses to retail tariff innovations are shaped by more than just price. Factors such as energy literacy and environmental awareness also influence household decision-making. For instance, low-income groups – driven by a stronger focus on electricity bills – tend to react more sensitively to price changes, while high-income groups, despite being less economically constrained, may respond positively to green tariffs out of environmental commitment [92]. These dynamics underscore the unequal impacts of dynamic tariffs across different income segments.

To balance efficiency gains with social equity, governments can provide subsidies to help low-income households acquire energy-efficient appliances, thereby enhancing their demand flexibility. At the same time, regulatory frameworks need to strike a balance between improving overall system responsiveness and safeguarding vulnerable groups, ensuring that dynamic pricing contributes to both efficiency and fairness in retail electricity markets.

5 Evolution and Innovation of EV Charging Packages

5.1 Global Market Evolution Pathways

The proliferation of electric vehicles (EVs) has not only reshaped patterns of energy consumption in the transportation sector but also driven structural innovation in retail electricity tariff design. EV charging packages have evolved beyond simple electricity pricing structures into integrated service models that combine pricing mechanisms, user behavior management, cross-sectoral collaboration, and digital platforms. Globally, the evolution of EV charging packages exhibits a phased trajectory: from retailer-led models utility-led models retailer–OEM collaborations unlimited subscription plans. These models are not mutually exclusive; rather, they overlap and intertwine, forming a diversified commercial ecosystem.

(1) Retailer-Led Models

The UK, as one of the most liberalized retail electricity markets, has incubated a number of innovative retailers. A representative example is Octopus Energy’s Intelligent Go plan. Its mechanism relies on the coordination of the vehicle battery management system (BMS), grid interface, and user application, enabling automated off-peak charging through smart scheduling. According to the company’s Smart Charging Annual Report, this model reduced annual average charging costs to £172 for participating users, with more than 150,000 vehicles enrolled [93]. Beyond cost savings, retailer-led models also tend to integrate broader carbon neutrality narratives, offering value-added services such as green electricity tracking and carbon footprint monitoring to enhance customer loyalty.

(2) Utility-Led Models

In the United States, Pacific Gas and Electric (PG&E) introduced the EV2-A tariff under the approval of the California Public Utilities Commission (CPUC), representing a classic transition pathway for traditional utilities. The tariff sets off-peak rates at $0.25/kWh and requires users to install smart charging stations to enable demand control and local dispatch [94]. Unlike the flexibility of retailers, utility-led models leverage broad system coverage and strong dispatching capacity. During grid peak hours, utilities can directly adjust charging loads across tens of thousands of smart chargers through aggregation platforms, thereby achieving large-scale peak shaving and valley filling. Such models demonstrate the irreplaceable role of utilities in ensuring grid reliability and system balance, where pricing authority serves system stability rather than individual customization.

(3) Retailer–OEM Collaborative Models

In Japan, Tokyo Electric Power Company (TEPCO) collaborated with automakers such as Nissan and Toyota to launch integrated service packages combining energy and vehicle services. The EV Life Plan bundles vehicle purchase incentives, charger installation, and differentiated electricity tariffs into a single product. TEPCO’s EV Package Evaluation Report (2023) indicated that Toyota’s bundled plan (¥0.23/kWh + free charger installation) led to 91% of charging occurring during off-peak hours, with a five-year retention rate of 92% [95]. This model highlights the natural advantage of OEMs at the customer entry point, while illustrating how retailers can enhance customer stickiness through cross-industry alliances. Collaborative models help stabilize demand-side consumption groups and strengthen corporate resilience against wholesale market volatility.

(4) “Unlimited Charging” Subscription Models

Subscription-based approaches have become a recent highlight in EV tariff innovation. Australia’s AGL Energy introduced the EV Add-On package, offering unlimited public charging nationwide across more than 2,000 charging stations for a subscription-based models (AUD 89), along with discounts for home charging. This model increased public charging utilization by 35% but reduced private home charger utilization by 12%, reflecting a shift in consumption scenarios [96]. While “unlimited charging” greatly enhances user experience and loyalty, its sustainability depends on both network scale economies and wholesale market price stability. Some studies warn that in highly volatile electricity markets, subscription models may increase hedging costs for retailers, necessitating complementary policy or market tools to maintain balance.

5.2 Pricing and Configuration Mechanisms

EV charging packages are no longer limited to differentiated price structures; they have gradually developed into a comprehensive set of mechanisms addressing risk-sharing, bill stability, demand response, and system integration. The overarching goal is to balance user experience and predictability of bills while maximizing the contribution of EV loads to power system flexibility management.

(1) Super Off-Peak Pricing + Controlled Charging

The theoretical basis of super off-peak tariffs lies in the principle of “peak–valley arbitrage.” By directing charging demand to periods of abundant renewable generation or low system load, these mechanisms simultaneously relieve grid stress and enhance renewable energy absorption. According to the Spanish Energy Agency’s White Paper on Demand Response (2021), when the peak-to-valley price ratio exceeds 1:4, users’ willingness to shift charging increases by 52% [97].

In recent years, several European countries have combined super off-peak tariffs with controlled charging schemes, requiring users to install remotely controllable smart chargers that allow grid operators to adjust charging power directly. Empirical studies in Denmark and the Netherlands indicate that such mechanisms effectively align EV loads with wind and solar generation variability, reducing peak loads by as much as 15–20%.

(2) Block Subscription and Bill Stability

Block subscription models, which combine prepaid quotas with per-unit charges for excess usage, reduce consumer exposure to price volatility. A typical example is ChargePoint’s Plus Membership in the United States, offering 250 kWh of electricity per month for a flat fee of USD 49.99, with additional usage billed at standard rates. Research by Fitzgerald et al. at the University of California, Berkeley, found that this model increased charging frequency by approximately 19%, but 18% of users consumed less than the included quota, effectively subsidizing heavier users [98].

Bill stability mechanisms further emphasize predictability. For instance, Engie Group in France introduced the Facture Fixe EV product, which allows households to set fixed monthly bills based on historical consumption. The company’s 2022 annual report showed that the product reduced residential customer churn by 12.3%, underscoring the importance of stable expectations in enhancing customer loyalty [99].

(3) Peak Dynamic Pricing and Demand-Side Management

Dynamic pricing plays a central role in demand response programs. In California, the Independent System Operator (CAISO) operates an Emergency Peak Pricing (EPP) scheme, under which electricity prices can rise to as high as USD 2.0/kWh when system load surpasses critical thresholds, incentivizing users to curtail non-essential usage [100].

However, studies have also shown that dynamic pricing may exacerbate distributional inequalities. Recent policy analyses recommend adopting “tiered pricing” strategies: providing low-income households with a fixed, low-price basic electricity allowance to cover essential consumption, while applying dynamic rates to usage beyond that threshold. High-income households, on the other hand, could be fully exposed to dynamic pricing, encouraging participation in demand response through storage and smart appliances [101].

(4) Vehicle-to-Grid (V1G / V2G) Integration

Vehicle-to-Grid (V2G) has emerged as a frontier in charging package configuration mechanisms.

V1G (Unidirectional interaction): Charging is managed in an orderly manner to shift load and reduce distribution network stress.

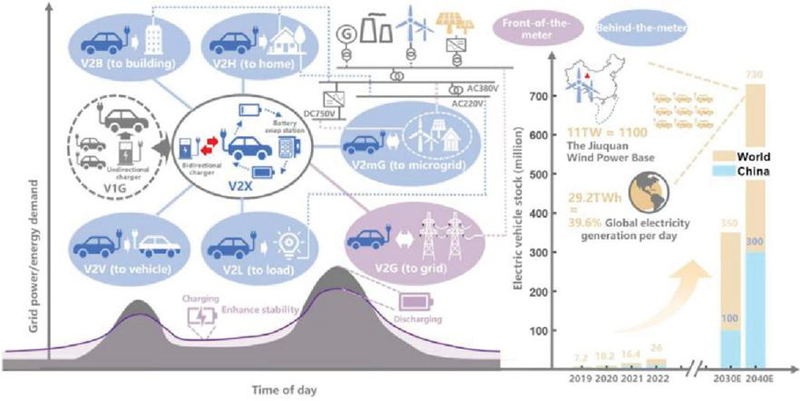

V2G (Bidirectional interaction): Vehicles charge during off-peak periods and discharge during peak demand, creating the value of “mobile storage” and transforming EV fleets into distributed flexibility resources (as shown in Figure 10).

Figure 10 The concept of V2G interaction and the potential power and energy capabilities of V2G [102].

Technically, V2G integration depends on bidirectional flows of energy and information between vehicles, chargers, and the grid. Recent studies show that in high-penetration scenarios, a fleet of 100,000 V2G-enabled EVs can provide peak-shaving capacity equivalent to that of a medium-sized pumped hydro storage facility [103].

Figure 11 China’s latest virtual power plants. Note: The colors of the provincial overlays indicate the leading market type.

China has also begun to explore this area. For example, in Guiyang, researchers constructed a network model integrating EV charging infrastructure with multilayer traffic networks and GIS data. By clustering points of interest (POI) and assigning node identifiers, they achieved joint simulation of traffic and power systems, providing a validation platform for future large-scale V2G applications in coordinated traffic–energy scheduling [104]. Figure 11 further illustrates user-side and independent storage participation in ancillary service markets such as day-ahead, intraday, real-time response, reserves, frequency regulation, capacity, and power quality [102].

5.3 Customer Segmentation Strategies and Digital Support

The design of EV charging packages is gradually shifting from single-price products toward personalized service systems. In this transition, three pillars have emerged as the core drivers of customer segmentation and value creation: data-driven demand profiling, cross-sector collaboration enabled by open APIs, and personalized recommendation with gamified incentives.

(1) Data-Driven Demand Profiling

With the widespread adoption of smart metering and in-vehicle sensor technologies, both retailers and research institutions can now conduct high-resolution analyses of charging behaviors across different user groups. In the United States, mobility and vehicle data have been used to distinguish between ride-hailing drivers – who display high-frequency fast-charging demand – and private car owners, who rely more heavily on overnight slow charging. In the European Union, clustering analyses have revealed distinct user segments, with some favoring public chargers for emergency replenishment while others exhibit strong cost-sensitivity [105]. In Japan, segmentation is built around vehicle types: battery electric vehicles (BEVs) require access to dense fast-charging networks, while plug-in hybrid vehicles (PHEVs) can more easily accommodate slow-charging scenarios.

A large-scale study by Strbac and colleagues at Imperial College London, based on GPS data from 100,000 UK EV users, further identified three archetypal groups: commuters, commercial users, and low-frequency drivers. Their research recommended differentiated charging packages tailored to these groups – for instance, off-peak discounts and fixed-bill options for commuters, bulk fast-charging discounts for commercial fleets, and low-fee basic packages for infrequent users [106].

(2) Open APIs and Ecosystem Collaboration

The opening of API interfaces and the growth of ecosystem partnerships have transformed EV charging packages from isolated pricing products into intelligent multi-stakeholder ecosystems. According to Gartner, ChargePoint’s API achieves 91% accuracy in predicting charger availability, significantly alleviating congestion at public stations [107]. In China, XPeng Motors’ “reserve-to-lock” function raised charger arrival success rates to 97.6%, demonstrating how API-enabled platform mechanisms improve user experience.

In Europe, BMW has partnered with virtual power plant operator Next Kraftwerke, integrating open vehicle APIs with grid dispatch systems. This collaboration reduced V2G response times to just 3.2 seconds, enabling EV fleets to participate directly in Germany’s secondary frequency regulation market [108]. Such mechanisms highlight the transition of EVs from passive electricity consumers to active resources within the power system.

(3) Personalized Recommendations and Gamified Incentives

Digitization has also advanced charging tariffs from price differentiation toward behavioral incentives. Tokyo Electric Power Company (TEPCO) introduced a demand response subsidy scheme in which users receive notifications during grid stress periods to reduce charging. Compliance is rewarded with bill rebates or bonus points, enabling a distributed “virtual power plant” with more than 100,000 EVs responding in a single event [109].

In the United Kingdom, BP Pulse launched a “charging points” reward system that converts off-peak charging behaviors into redeemable vouchers or mileage credits. This gamified mechanism has significantly increased participation in off-peak charging. Beyond strengthening customer interaction and engagement, it also generates precise behavioral feedback for retailers, thereby establishing a closed loop of data-driven insights behavioral incentives tariff iteration.

5.4 Performance Evaluation and Distributional Effects

EV charging packages are not only a tool of tariff design but also serve as an important mechanism for demand response, investment recovery, and social equity. Their performance is typically assessed along three dimensions: peak load reduction, cost savings and investment recovery, and adoption rates under income heterogeneity.

Peak Load Reduction

Within demand response frameworks, charging packages are widely used to achieve peak–valley load balancing. Some studies have applied reinforcement learning methods to construct price-generation functions and, through Proximal Policy Optimization (PPO) algorithms, determine tariff parameters under market and capacity constraints. This enables aggregators to maximize profits while simultaneously reducing peak load [110].

Empirical evidence indicates significant income-based differences in the effectiveness of TOU pricing. Higher-income households with greater flexibility tend to shift high-consumption appliances – such as washing machines, water heaters, and EV charging – into off-peak periods. In contrast, lower-income households, constrained by limited equipment or housing conditions, often exhibit weaker responsiveness [111]. This divergence implies that the system-level benefits of peak load reduction may be unevenly distributed across socioeconomic groups.

Cost Savings and Investment Recovery

The impact of dynamic pricing on household electricity expenditures remains contested. On one hand, several studies suggest that dynamic tariffs reduce bills for price-sensitive consumers by 5–15%. On the other hand, evidence also shows that households with limited response capabilities may face higher overall costs [112]. This discrepancy arises from the dual mechanism of dynamic pricing: while it creates opportunities for arbitrage through off-peak tariffs, actual cost savings depend heavily on users’ cognitive awareness, capacity to invest in enabling technologies, and behavioral flexibility.

According to the UK National Audit Office (NAO), the average cost of smart terminal retrofits is approximately £89 per household. Under a 4:1 peak-to-valley price ratio, the payback period for such investments can be shortened from seven years to five years, demonstrating that strong price signals can significantly accelerate the recovery pathway [113].

Income Differences and Adoption Rates

Adoption of dynamic packages is highly correlated with income levels. High-income groups typically own a greater share of smart appliances, enjoy more flexible schedules, and value environmental benefits, making them more likely to adopt green and flexible tariff options [114]. By contrast, low-income households face significant barriers, including upfront costs, constraints on housing retrofits, and limited access to information. As a result, they may not only miss out on potential savings from dynamic pricing but may also bear greater bill volatility risks under competitive retail markets [115].

These distributional effects suggest that without adequate policy support – such as subsidies, educational initiatives, and baseline electricity guarantees – dynamic pricing and smart charging packages, while improving system efficiency, may inadvertently exacerbate social inequality.

6 Emerging Trends and Innovation Directions

With the accelerating global energy transition and transport electrification, retail electricity packages are evolving from traditional time-based pricing tools into comprehensive mechanisms that support system flexibility, market innovation, and consumer protection. Future development is simultaneously driven by technological advances, regulatory innovation, and social equity concerns. Six key directions can be identified(as shown in Table 4).

6.1 Locational Marginal Cost Pricing

Under the rapid growth of distributed energy resources (DERs) and flexible loads, traditional average pricing fails to reflect local marginal costs. Several European countries have initiated pilots where Distribution Locational Marginal Pricing (DLMP) is directly mapped into retail tariffs [116]. For example, New York State’s “Value of Distributed Energy Resources” tariff incorporates the locational value of solar PV and storage into nodal prices, guiding investment towards grid-constrained areas and reducing costly distribution upgrades.

6.2 Deep Vehicle–Grid Integration Tariffs

Electric vehicles (EVs) are becoming the fastest-growing and most dispatchable load segment. Through ultra-off-peak pricing with automated scheduling or bidirectional Vehicle-to-Grid (V2G) schemes, charging demand can be shifted to periods of renewable surplus, while vehicle batteries simultaneously participate in frequency regulation, peak shaving, and capacity markets [117]. A joint pilot by Octopus Energy and Nissan in the UK demonstrated that V2G participants achieved annual bill savings of around 30%, while providing the grid with flexibility comparable to that of a mid-sized storage plant.

6.3 Transactive Energy and P2P Settlements

Enabled by blockchain and centralized trading platforms, prosumers (users who both consume and generate electricity) can now engage in peer-to-peer (P2P) energy trading within local or virtual communities [118]. Platforms such as Power Ledger in Australia and the Yokohama Local Energy Community project in Japan have shown that P2P models not only enhance renewable energy integration but also transform retailers from “energy sellers” into platform operators and balancing service providers. Future retail packages may evolve into “transactional memberships,” where subscribers gain access to distributed trading and green certificate settlement.

6.4 Hybrid “Subscription + Dynamic” Billing

In Nordic and Australian markets, subscription-based models combined with real-time overage pricing have rapidly gained popularity. This hybrid billing model increases bill predictability for consumers while enabling retailers to aggregate flexible loads for wholesale market participation, partially hedging against price volatility [119]. More importantly, it provides low-income households with a “stable bill” transition pathway, gradually familiarizing them with dynamic tariffs while maintaining social equity.

6.5 AI-Driven Personalized Packages

Artificial intelligence and big data analytics are reshaping retail tariff design. Advanced metering and load disaggregation algorithms enable retailers to identify user-specific behaviors and elasticity in real time, thereby generating automated tariff recommendations [120]. Some companies have already developed AI-driven “dynamic recommendation engines” that integrate reward points, carbon labels, and gamification to enhance customer engagement. For instance, EDF’s “AI Smart Bill Advisor,” launched in 2023 for 400,000 households, dynamically adjusted ToU blocks and increased customer satisfaction by 18%.

Table 5 Description of innovation vectors

| Innovation Vectors | Concept Description | Demonstration Project |

| Electric Vehicles | Late-night ultra-low prices + controlled charging windows | Octopus Intelligent (UK); Drive-On (California) |

| Retail-Level Node Pricing | Detailing transmission and distribution network congestion costs to the user side will incentivize DER deployment. | VDER-P2 (New York); Wholesale Club (Texas) |

| Transactional Energy/P2P | Blockchain or platform-based inter-user settlements and packaged ancillary services | Power-Share (Japan); Powerledger (Australia) |

| Subscription-Dynamic Hybrid | “Netflix-style” credit limit + floating top-up | Nordic Fixed Fee + Spot Floating |

| AI-Based Precision | Machine learning clustering to match user flexibility and assets | Pilot programs in Spain, South Korea, and Singapore |

6.6 Regulatory and Risk Governance Innovation

With the rapid expansion of dynamic pricing and digital retail platforms, price volatility, data privacy, and cross-sector competition have emerged as key regulatory concerns. Policymakers are responding with instruments such as price caps, stabilization funds, API encryption standards, and new market entry rules to balance efficiency improvements with consumer protection [121]. The European Union’s Electricity Market Design Reform Directive (2024) explicitly requires retailers to offer both fixed-price and dynamic contracts, while guaranteeing consumers the right to switch contracts at any time, thereby ensuring that innovative tariff models expand in a safe and sustainable manner.

7 Conclusions

The evolution of retail electricity pricing has moved far beyond the traditional average-cost recovery paradigm, developing into a multi-layered framework that integrates marginal-cost reflection, risk-sharing, and distributional fairness. This review traced the historical development of tariff models, summarized international regulatory practices, analyzed the underlying design mechanisms, examined the rise of EV-specific charging schemes, and synthesized emerging trends shaped by digitalization and system flexibility. Retail tariff design is now characterized by experimentation and rapid technological integration; it is increasingly tied to real-time data, automated decision-making, and cross-sector coordination. While these developments promise substantial efficiency gains, they also introduce new challenges in consumer protection, equity, and regulatory oversight.