The Disruptive Innovation Potential and Business Case Investment Sensitivity of Open RAN

Tsvetoslava Kyoseva1,*, Vladimir Poulkov1 and Peter Lindgren2

1Technical University Sofia, Bulgaria

2Aarhus University, Denmark

E-mail: ts.kyoseva@gmail.com; vkp@tu-sofia.bg; peterli@btech.au.dk

*Corresponding Author

Abstract

Every telecom constantly faces the dilemma of when to invest in the next generation infrastructure network and how the investment would be monetized. The telco value proposition comprises products, services, processes, technologies, and network infrastructure. This paper explores making the business case out of Open RAN investment for a 5G network, where Open RAN is further researched if telcos perceive it as radical or disruptive innovation. As part of the research, different telecom companies are approached with a set of questions. The results are analysed and mapped in a Business Model Innovation chart. Furthermore, this paper also covers an analysis related to evaluating the sensitivity of how profitable a telco could be depending on Open RAN TCO investment for 5G deployments and the number of customers using value propositions – products, services and processes. Two sensitivity scenarios are simulated so various combinations could be observed before taking any further decision for Open RAN 5G business model implementation.

Keywords: 5G, business model innovation, disruptive innovation, open RAN, telecommunications, total cost of ownership.

1 Introduction

Last decade, telecom operators were focused on making their networks more into the cloud and driven by software. They have moved from vertically integrated networks to virtual network functions (VNFs) and cloud-native network functions (CNFs) running on pure cloud infrastructure. The research business Analysys Mason forecasts that virtual RAN (vRAN) will be the fastest-growing investment in operators’ cloud networks, from 293 million USD in 2021 to 12,1 billion USD by 2026 [1]. Until it becomes so, the radio access network (RAN) stands against the heavy cloudification process happening in other network domains mainly because of its performance requirements and complexity. However, the separation of RAN software from fixed-function hardware became technically and economically possible due to technological advancements in hardware and CNFs [2]. However, this is not the first attempt in that direction. Until now, base stations were decomposed in deployment by more than a single vendor per site, based on standardized reference architectures. In the third generation (3G), the Wideband Code-Division Multiple Access (WCDMA) separates RAN to Radio Network Controller (RNC) and base station (e.g., NodeB), making possible one-to-many connections between those network elements. In the fourth Generation (4G) deployments, all multivendor connections between RAN base stations and core networks (CN) based on a standardized interface have commonalities. What was still left proprietary were the interfaces in RAN among proper nodes. Despite all the activities, the mature solutions implemented in base stations are delivered by only one vendor. All experts in the industry refer to that as vendor lock-in.

Besides the virtualization and cloudification, some components, e.g., antenna systems, will remain physical. However, many other RAN functions can be virtualized and deployed in cloud-native infrastructure. In addition, two major industry initiatives and standards such as O-RAN and Open RAN, together with the most important current business model ecosystem (BMES) and domain players, made significant progress in specifying and standardizing the functional disaggregation of the RAN into a centralized unit (CU), distributed unit (DU), and radio unit (RU). This is expected to result in a more diverse vendor and technology based BMES. Such BMES will take a focal place around decentralized general hardware and open cloud platforms that connect these all disaggregated network components. This is a radical business model innovation (BMI) approach from current one-vendor, application-based, pre-integrated RAN architecture [1].

Many operators claim their motivation to pursue the opportunity to offer new services with 5G in various consumer and industry segments using next-generation RAN capabilities. Such as ultra-low latency, network slicing, and other technologies like edge computing. 5G is going to take a cornerstone part in increasing the usage of broadband connectivity. Also, it is expected government and private sector to be digitally transformed. However, operators face the challenge of significant CAPEX and OPEX spending. This is because of a constant increase of network sites using traditional network technologies without a “wow” product or service to build the business case including CAPEX and OPEX calculation for verifying investment return. This presses operators to rethink how they design, develop, and support their networks, and here is where Open RAN takes place.

The number of subscribers of mobile networks is higher than the world’s total population [2]. In unison with that, the forecasts show that the number of cells and sites will continue to grow due to the implementation of new frequency bands and network densification in general. According to [3], it is forecasted that 8,8 billion mobile subscriptions will be active in 2026. It shows that more networks that are deployed as centralized are a necessity. That is why Open RAN development proves the willingness of all industry players: operators, vendors, neutral hosts, integrators, private businesses, etc., to open the RAN architecture to eliminate potential obstacles to further developments. Such openness is expected to be guaranteed by a specification of proper interfaces between logical nodes and the introduction of new network elements which can incorporate intelligence through Artificial Intelligence/Machine Learning (AI/ML).

As to market analysis [3], the biggest driver for the adoption of OpenRAN is to reduce the total cost of ownership (TCO), followed by reducing the time to deploy new services, improve scaling/elasticity, support new enterprise revenue, improve ROI case for vRAN, improve the business case for mobile edge services. They all have a 30% to 40% response rate and could be categorized in two directions: a/ efficiency of infrastructure investment and b/ optimizing cost.

The RAN is estimated to be around 60% of CAPEX and OPEX for MNOs. The new generation of mobile communications is leveraging several technology trends. Suppose more BMI’s are delivered in that segment [4].

As a result of previous research on types of BMI’s in the telecom industry, the most innovations are in the infrastructure [5]. For a new implementation to be treated as an innovation, it is assumed it should meet the BMI framework by analysing each dimension of complexity, radicality, and reach. As a result, the most significant portion of BMI’s done by telecom operators, 67% were identified as infrastructure innovations.

The concept of both disaggregated HW and SW and open interface are these key trends, and they are the focus of this paper’s research [5]. Due to the expected increase in data traffic usage, it became an essential topic for implementing 5G and all other following generation networks.

This leads to two important initiatives for each telco that are expected to be part of their future strategies: a/ making a business case out of infrastructure investment and b/ optimizing operations’ costs.

The structure of the paper is as follows: in Section 2, we review the O-RAN concept. In Section 3, we describe the applied research methodology for determination of the disruptive innovation potential and business case investment sensitivity. In Section 4, we present the results of the research and related analysis, and finally, in Sections 5 and 6, we formulate our conclusions and directions of future work.

2 Open RAN

2.1 Open RAN Definition

There are two terminologies in the field with a similar naming convention [6]. Open RAN, also written as O-RAN, is the initiative of the O-RAN alliance that aims to define open interfaces of the disaggregated RAN architecture. Open and virtualized interoperable RAN specifications are the main focus of the group. The O-RAN alliance works with other industry bodies like 3GPP and ONF to facilitate a holistic end-to-end RAN solution.

Telecom Infra Project (TIP) has its project called OpenRAN, which aims to disintegrate all RANs from 2G to 5G by having multivendor interoperable solutions built on general-purpose hardware called commercial off-the-shelf (COTS). OpenRAN does not define new open interfaces but speeds up adoption and deployments through existing open interfaces. In that respect, it works together with the O-RAN Alliance to reuse their interfaces, doing no overlapping work.

The work over RAN virtualization is happening not today since there are also distributed RAN (D-RAN), centralized RAN (C-RAN or Cloud RAN), centralized and virtual RAN (vRAN), and the latest centralized, spread, and open RAN (O-RAN).

Open RAN will be used for this paper’s simplicity, meaning all the above.

There are a lot of benefits Open RAN is expected to bring to nest generation networks deployment. The most important of them are listed here [2]:

• Multivendor ecosystem (hardware and software disaggregation)

The multivendor approach means disaggregating the software from the hardware, which in practice means that different vendors could deploy other elements of RAN. Even though many new players have become part of the ecosystem, their number is still not significant enough to assure a real multivendor ecosystem [7].

• Cost reduction

Even though a vast range of cost reduction, between 20% and 40%, is forecasted by different bodies and research organizations, it should be noted that the TCO reduction goal with Open RAN is still not straightforward to be achieved [1]. That is maybe the main reason why operators are cautious about the operational and technology hurdles and need guidance on completing the promised cost savings. Open RAN represents a significant departure from the traditional way operators design, procure, deploy and manage their large and complex RAN. It also changes operators’ relationships with their partner suppliers. Operators do not have a standard plan for how to manage the TCO for implementing Open RAN technology.

• Interoperability

But still, a complete and pre-tested ecosystem that can provide an open, standards-based full-featured stack to reduce integration costs and time to deploy is not ready [1].

• Zero-touch automation and distributed orchestration

Open RAN relays on zero-touch automation and orchestration from the beginning about remote and automated deployment and software installation, then preparation for the operation, tests, and validations, and ongoing live operations like self-healing, self-optimization, updates, and upgrades with continuous integration (CI) and continuous delivery (CD) (CI/CD) [1].

• Open and programable interfaces

Open interfaces mean it is easier to swap one vendor’s hardware or software for another because of the interfaces between them. This lowers the risk, especially if an operator wants to work with a new or small supplier, making it more viable to diversify the supply chain, even for critical elements such as RAN VNFs or radios. It also futureproofs the network. One of O-RAN’s work groups is focused on creating an open, interoperable fronthaul interface, which will enable the integration of DUs and RUs from different vendors and is essential to allow a multivendor ecosystem [3].

• Open software

Open platforms provide access to a broader base of innovation than traditional platforms and accelerate progress, as demonstrated in enterprise open-source communities. Smaller operators, in particular, may enhance their ability to influence requirements and specifications through open alliances [3, 8].

• Commercial off-the-shelf hardware (e.g., x86, ARM CPUs)

COTS means using generic, non-telco-specific hardware units that reduce operational and training costs incurred from running and managing vendor-specific HW units. It also unburdens the operator of both vendor lock-in and tight to proprietary HW configuration issues. The last usually results in high operational costs and the limitation of HW reuse across the telco network [9].

• Mobile edge computing (MEC)

Edge computing is a distributed computing environment that brings computation and data storage closer to the data sources. Mobile Edge Computing (MEC) aims to position computing and storage resources on the RAN edge to improve content and application delivery for 4G and 5G network users [10]. MEC paradigm environment is characterized by very low latency, high bandwidth, and real-time access to radio network information. That is why it enables the deployment of new applications and services such as IoT, video analytics, and connected cars. Deploying distributed data centers capable of content caching and processing is vital for achieving low latency in mobile networks, which is also one of the defining characteristics of 5G.

• Energy efficiency

For many operators, energy consumption has been with the highest operating costs, thus one to be considered significantly. The situation is that telecom energy industry usage has to decrease because it currently consumes around 3% of global energy. Also, 3GPP’s 5G specification requests a 90% reduction in energy use. The focus is expected to be on mobile communication networks where the dominating energy consumption comes from the radio access network. The future connected society consists of sensors embedded in cars, drones, health, and wearable devices, which will all use mobile networks to communicate. Furthermore, all devices would interact with people and with each other. According to Chochliouros et al. [11], radio access consumes 50,6% of overall telco energy consumption, followed by 23,3% for data centers.

• Improved security

Open source software brings security challenges regarding its open nature but also has advantages, like fast functionalities delivery due to the possibility for code customizations. The 5G customer use cases like self-driving cars, smart power grids, and buildings make security a tremendous concern [12]. Moreover, the use of non-telco-specific hardware comes with its security complexity. That said, the Open RAN security concerns have no easy solution, but all bodies involved took that topic with utmost importance.

• Enabling or speeding up innovations

Investing in the RAN to meet the demands of these new generation applications can also speed up application development and end-user adoption [10].

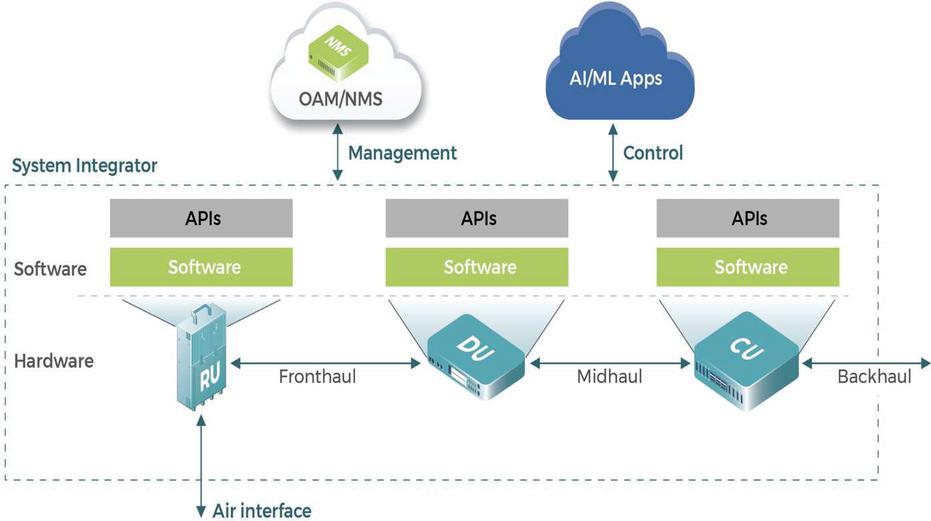

Figure 1 Open RAN reference architecture (Source: Telecom Infra Project) [14].

2.2 Open RAN Target Architecture

There are different options for OpenRAN implementation. It mainly depends on if the implementation is greenfield or brownfield, where the last means there is an infrastructure in place that should be considered in the implementation project. OpenRAN architecture is depicted on Figure 1 [13, 14].

Also, there are different OpenRAN implementation scenarios depending on what location are CU and DU [15]:

• Distributed CU/DU

• Distributed DU, Central CU

• Central DU and Central CU

In all done researches, the implementation of Open RAN is compared to the so-called traditional RAN. How OpenRAN is compared to the conventional RAN can be seen in Table 1 [16]:

While major focus now is related to the calculation of the percentage cost optimization compared to the traditional RAN, this paper will analyze and model the profit sensitivity with the breakthrough of Open RAN investment [1]. All TCO model calculation demonstrates significant cost savings for Open RAN compared to traditional one. Still, operators should target new revenue opportunities to improve the Open RAN business case, primarily because with Open RAN technology, barriers to delivering new revenue-generating services at the edge are removed.

Table 1 Open RAN comparison with the traditional RAN

| Traditional RAN | RAN with 1st Level Disaggregation | Disaggregated O-RAN |

|

• Closed proprietary system • No open interfaces • No interoperability |

• Proprietary system • Some disaggregation • Partially virtualized • No interoperability |

• Further disaggregation • RAN cloudification • Open APIs • Multivendor interoperability |

2.3 Open RAN Products and Services

The most significant potential source of revenue because of Open RAN comes from the forecasted growth in private businesses’ spending on public edge cloud computing services. Various use cases are expected to assure near-real-time communication and privacy to users across different industry verticals, like industry 4.0 services such as robotics, manufacturing automation, and autonomous cars. Analysys Mason calculates that the revenue from these edge services will grow between 2019 and 2030 to reach 23,5 billion USD [1]. Likewise, ultra-reliable low latency communication services are one of the defining features of 5G. Such services are smart cities, automotive services, manufacturing, and transport and logistics [17]. Improving the current services for machine to machine communications and smart cities has been identified as a 6G target. The considered services are holographic communications, high-precision manufacturing, sustainable development, and intelligent environments [18]. Critical use cases, though, include better connectivity for smartphones (faster data connectivity, alongside VR/AR), logistics tracking, and specific applications that use data heavily in indoor environments that require low mobility, e.g., smart buildings [19].

3 Research Methodology

3.1 Research Methodology Part 1 (Open RAN Business Model Innovation)

The applied research methodology in this paper consists of two parts. First representatives with technical and business roles from 5 European operators have been asked questions via online form. The questionnaire follows the BMI framework and the purpose of the questionnaire is to identify whether the telecom perceives Open RAN as the next disruptive innovation or not. The questioned operators represent the following countries Bulgaria with three operators, Austria and Switzerland.

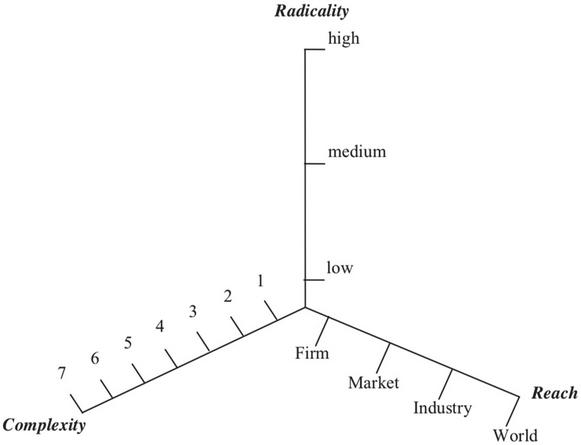

The 3-dimensional BMI is depicted in Figure 2 below [20, 21].

Figure 2 A 3-dimensional business model with reflection on achieved innovativeness.

Table 2 Incremental and radical orientation in the proposed BMI framework

| Complexity Dimension | ||

| Part of BMI | Incremental BM Innovation | Radical BM Innovation |

| 1. Value proposition (Products, Services, Processes of products and services) | What the Business is doing but in a better way | Business is doing something differently |

| 2. Users and Customers | Existing users, customers, and markets | New users, customers, and markets |

| 3. Value chain function | Exploitation (lean, continuous improvements) | Exploration (open, diversified) |

| 4. Competencies | Familiar (e.g., technology) | New and unfamiliar (e.g., technology) |

| 5. Partner network | Familiar and/or existing partner network | New networks (alliances, joint ventures) |

| 6. Value formula | Incremental cost-cutting in existing processes | New processes to generate revenues, or radical cost-cutting in existing processes |

| 7. Relations | Continuous improvement of existing relations in the distribution channels | New relations to new channels are built |

The three dimensions cover the ranges to the explained degree below:

• Radicality – where a low score of 1 is incrementally new, a middle score of 2 is radically new, and a high score of 3 is disruptively new.

• Reach – where a low score of 1 is considered new to the Business (firm), a middle score of 2 is regarded as new to the marketplace and/or the industry, and a high score of 3 is considered new to the world.

• Complexity covering 1–7 BM Dimensions – ranging from a low score of 1 where change happens in 1–4 BM dimensions simultaneously, a middle score of 2 where changes occur in 5 BM Dimensions simultaneously, and a high score of 3 where any change happens in 6–7 BM dimensions simultaneously.

The questions and their incremental and radical (disruptive) meaning from the Complexity dimension, part of the 3-dimensional BMI, are listed and explained in Table 2.

3.2 Research Methodology Part 2 (Open RAN Business Case Sensitivity Analysis)

In this section a Business case for expected new services is calculated based on assumptions. This forms part two of the current research, where sensitivity analysis is done regarding telecom profitability. The purpose of that research part is to prove that even with significantly reduced TCO, telecom has a real opportunity to introduce new products and services with a positive revenue impact. The optimal results are searched for the combination of:

• How sensitive is the Profit based on Revenue and TCO?

• How sensitive is the Profit based on the Number of customers and TCO?

To be able to execute sensitivity, a set of assumptions was made based on infrastructure simulation [1]:

• TCO optimization of 30% calculated by modelling Open RAN for medium-sized incumbent Tier-1 in a developed market.

• Open RAN modelling is based on centralized vCU, 1700 total number of RAN sites at the end of the third year (mix between urban and city), and 35% 5G coverage of territory at the end of the third year.

• The business plan is calculated for three years.

• CAPEX assumptions consider the cost for RAN hardware, software, and backhaul.

• OPEX assumptions consider the cost of support and maintenance, additional FTE costs, and power costs.

Table 3 Business plan modelling for Open RAN implementation

| Revenue from (in ’000 USD) | 1 | 2 | 3 |

| Upsell current data plans | 31,680 | 31,680 | 31,680 |

| Private networks | 500 | 500 | 500 |

| Smart bildings | 500 | 500 | 500 |

| Industrial networks | 500 | 500 | 500 |

| Support and Maintenance | 300 | 300 | 300 |

| Total Revenue per year | 33,480 | 33,480 | 33,480 |

| Total Revenue for 3 years | 100,440 | ||

| TCO (CAPEX+Opex) for 3 years | 60,000 | ||

| Profit for 3 years | 40,440 |

The revenue model was done by modelling the customer base and offering new products and services, as shown in Table 3 below. The considerations about offering new products and services that will generate additional revenue are:

• Upsell 20% of all current data plans with 1 USD/month for the whole period of three years.

• Offer private networks for businesses that would like to have their own private 5G network. The assumption is that the telco will have one such customer per year with a service revenue of 500k USD per implementation. An example of such a network is the airport businesses.

• Offer smart buildings with a variety of sensors. A rough estimation of 5 new building clients with a 5G network per year is provisioned for three years. Each client is charged 100k USD one time.

• Offers for industrial networks, e.g., mining that would like to automate their processes with ML/AL, where robots are expected to go underground instead of people. A network with OPEN RAN is to be built especially for them. The price for such a network is assumed to be 250k USD once, and the telco is projected to gain two new clients each year for three years.

• Revenue coming from support and maintenance of those new services compounded by 20% annually on a revenue basis.

4 Research Results

4.1 Results from Part 1 (Open RAN Business Model Innovation)

The following outcome is depicted question by question in the sections below, applying the questionnaire methodology. The research was done with five European telecom operators, three of them located in Bulgaria, one in Austria, and one in Switzerland. Four out of five respondents have a technical role and one with a business role in the telecom.

4.1.1 Value proposition question

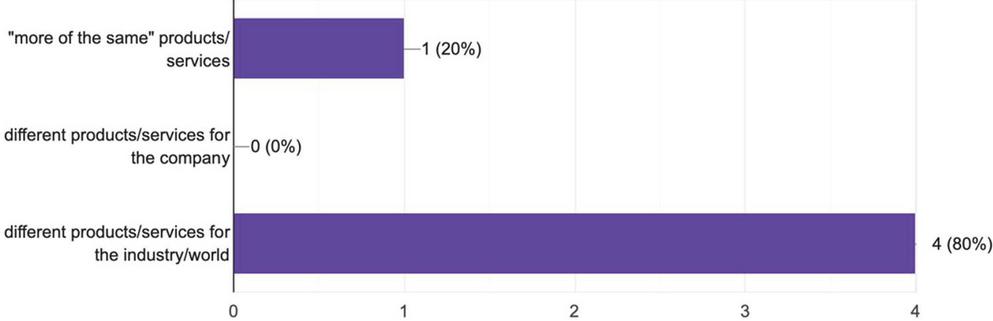

The first question is related to the value proposition, which says that with Open RAN, telecom operators will be able to offer what kind of products and services. Four out of five telecoms responded that with Open RAN, they expect to be able to provide different products and services for the whole industry. Only one telco reckons that with Open RAN, it would be able to offer “more of the same” products and services. N this question, no one from the respondents thinks that different products and services would be offered, but for the company only. Visualization of all responses is provided in Figure 3.

Figure 3 Value proposition question – With Open RAN telecom operators are going to be able to offer what kind of products and services?

4.1.2 Target customers question

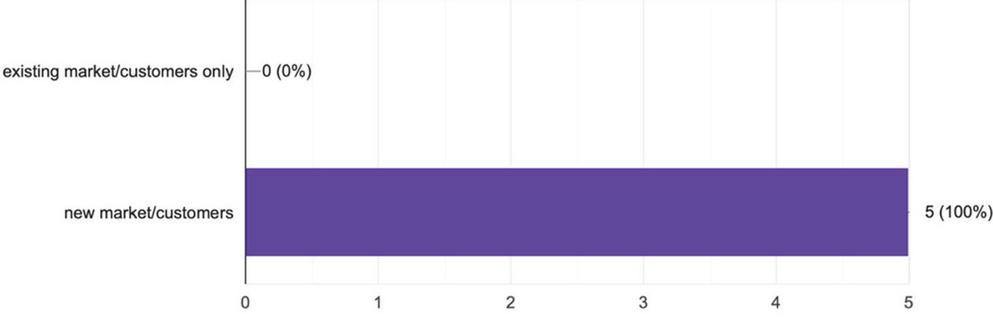

The second question from the questionnaire is about telco target customers with the Open RAN concept. The question itself researches with Open RAN telecom operators are going to be able to address what kind of market/customers. Here all five asked telecoms supposed that they would have the opportunity to address new markets and customers respectively. No one sees Open RAN would target existing markets and customers only. All responses are depicted in Figure 4.

Figure 4 Target customers’ question – With Open RAN telecom operators are going to be able to address what kind of market/customers?

4.1.3 Customer relationship question

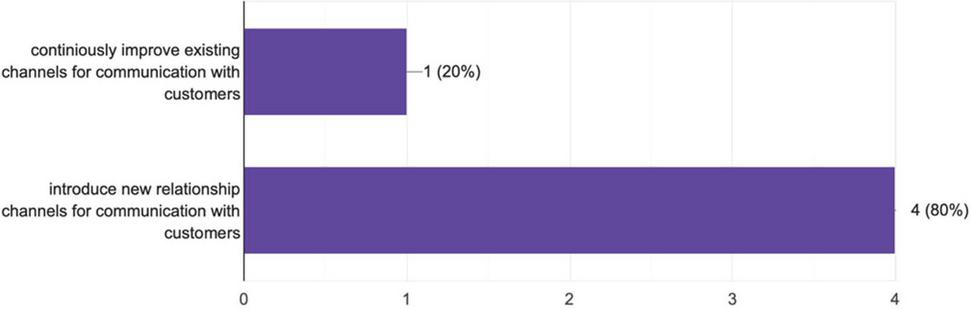

The third question addressed how the telco communicates with its customers. The question says: with Open RAN, telecom operators are going to be able to build what kind of relationship with their customers. Four of five telecoms consider Open RAN would allow them to introduce new relationship channels for customer communication. Only one response foresees that with the implementation of Open RAN, it will be able only continuously to improve existing channels for communication with customers. Results are visualised in Table 5

Figure 5 Customer relationship question – With Open RAN telecom operators are going to be able to build what kind of relationship with their customers?

4.1.4 Value chain architecture question

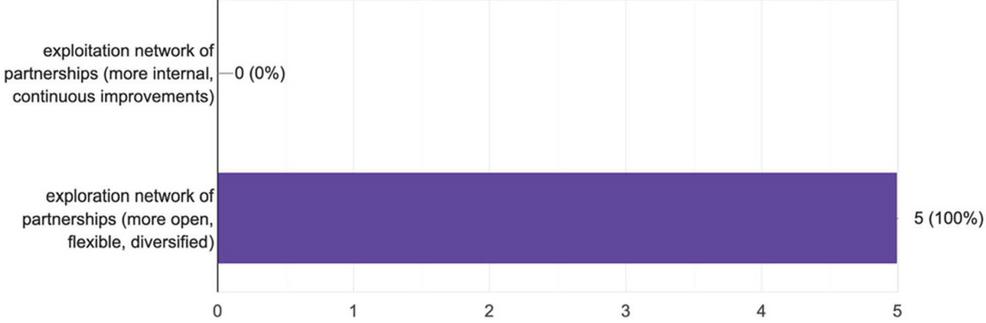

The next question asked the telecoms what kind of value chain they would experience with Open RAN deployment. All five operators are unanimous that they will be able to explore the more open, flexible, and diversified network of partnerships. No one considers the future value chain to be more internal and with only continuous improvements. Results from this question are shown in Figure 6.

Figure 6 Value chain architecture question – With Open RAN telecom operators are going to be able to apply what kind of value chain?

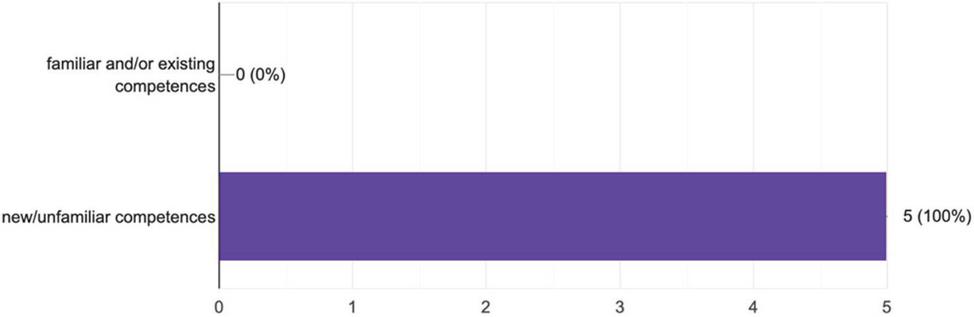

4.1.5 Core competences question

Core competences are the target of the following question from the research. The telcos were asked with Open RAN what competencies they would be able to apply. All five answers say that new and unfamiliar to that moment competences are expected. Respectively, no one thinks they could cope with Open RAN with existing competences. Figure 7 below summarizes responses to that question.

Figure 7 Core competencies question – With Open RAN telecom operators are going to be able to apply what kind of competencies?

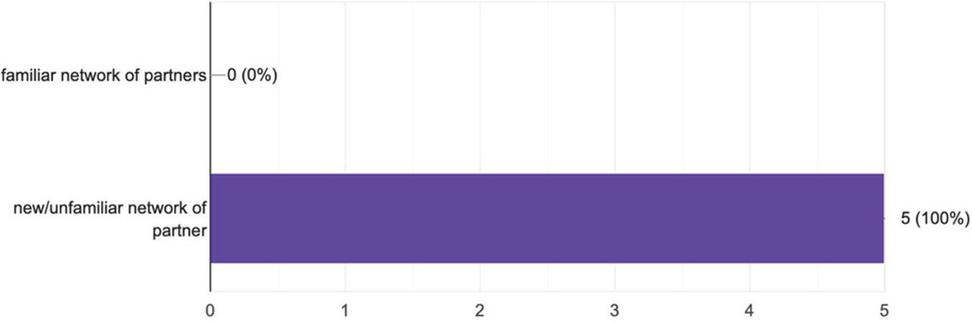

4.1.6 Partner network question

The telco partner network is the subject of study in the next question. With Open RAN, telecom operators can apply what kind of partner network?” reads this question. Again, all answers say that the Open RAN partnership network is expected to be new and unfamiliar at that moment. Figure 8 resumes the answers in that category.

Figure 8 Partner network question – With Open RAN telecom operators are going to be able to apply what kind of partner network?

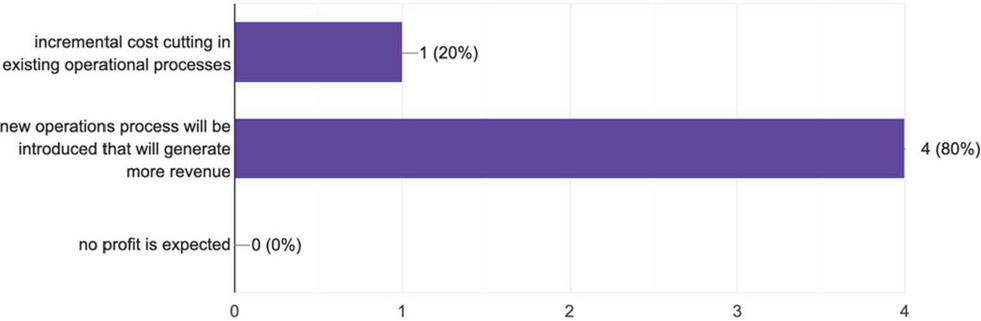

4.1.7 Profit question

Perhaps one of the essential issues explored in this research work is profit. The telcos were asked, “With Open RAN telecom operators are going to be able to apply what kind of Profit?” Four of five telecoms consider that a new process will be introduced with Open RAN to generate more revenue. Only one telco thinks that Open RAN would lead to incremental cost-cutting in existing operational procedures, and no one foresees no profit from Open RAN in general. Figure 9 shows all answers.

Figure 9 Profit question – With Open RAN telecom operators are going to be able to apply what kind of Profit?

4.1.8 Innovativeness reach question

The next question validates to whom do telcos consider Open RAN to be new, which shows the innovativeness reach. Four out of five operators believe that Open RAN is unique for the market and the industry, and only one supposes this is a new concept for the world. No one implies that innovativeness is only new for the telco. Figure 10 presents all the responses.

Figure 10 Innovativeness reach question – To whom do you consider Open RAN is new?

4.1.9 Innovativeness radicality question

The last question investigates whether Open RAN is incremental, radical, or disruptive innovation. Four out of five telcos opine that Open RAN is a radical innovation, and only one supposes it is an incremental one. No one believes Open RAN is a disruptive innovation in this research group. Figure 11 shows all responses.

Figure 11 Innovativeness radicality question – How do you perceive Open RAN in terms of innovativeness?

All the answers from the questionnaire are mapped in the BMI framework. Scores for Radicality, Reach, and Complexity are depicted in Table 4.

Table 4 BMI scoring for Open RAN

| BMI Score | 1 | 2 | 3 |

| Radicality | 2 | ||

| Reach | 2 | ||

| Complexity: | 3 | ||

| Value proposition | 3 | ||

| Target customers | 3 | ||

| Customer relationship | 3 | ||

| Value chain | 3 | ||

| Core competences | 3 | ||

| Partner network | 3 | ||

| Profit | 3 |

Figure 12 BMI scoring visualization for Open RAN.

Taking the score results from Table 4 is visualized in Figure 12. All Radicality, Reach, and Complexity dimensions form a point in the cube’s upper surface, meaning that Open RAN is perceived as somewhere between radical and disruptive innovation. It makes a particular impression that this technology generally impacts all components of the complexity axis.

Even though no one considers Open RAN a disruptive innovation, all seven dimensions from BMI’s complexity axis are expected to be generally impacted means that the telecom business model is expected to be disrupted.

4.2 Results from Part 2 (Open RAN Business case Sensitivity Analysis)

Two variable parameters are used for this sensitivity analysis of Profit: Revenue for three years and TCO investment for three years. All the combinations can be observed in Table 5:

Table 5 Profit sensitivity analysis based on revenue and TCO

| in ’000 USD | Revenue for 3 Years | |||||||

| 20,440 | 40,440 | 60,440 | 80,440 | 100,440 | 120,440 | 140,440 | 160,440 | |

| 20,000 | 440 | 20,440 | 40,440 | 60,440 | 80,440 | 100,440 | 120,440 | 140,440 |

| 40,000 | (19,560) | 440 | 20,440 | 40,440 | 60,440 | 80,440 | 100,440 | 120,440 |

| 60,000 | (39,560) | (19,560) | 440 | 20,440 | 40,440 | 60,440 | 80,440 | 100,440 |

| 80,000 | (59,560) | (39,560) | (19,560) | 440 | 20,440 | 40,440 | 60,440 | 80,440 |

| 100,000 | (79,560) | (59,560) | (39,560) | (19,560) | 440 | 20,440 | 40,440 | 60,440 |

| 120,000 | (99,560) | (79,560) | (59,560) | (39,560) | (19,560) | 440 | 20,440 | 40,440 |

| 140,000 | (119,560) | (99,560) | (79,560) | (59,560) | (39,560) | (19,560) | 440 | 20,440 |

| 160,000 | (139,560) | (119,560) | (99,560) | (79,560) | (59,560) | (39,560) | (19,560) | 440 |

| 180,000 | (159,560) | (139,560) | (119,560) | (99,560) | (79,560) | (59,560) | (39,560) | (19,560) |

| 200,000 | (179,560) | (159,560) | (139,560) | (119,560) | (99,560) | (79,560) | (59,560) | (39,560) |

| TCO (CAPEX OPEX) for 3 years. | ||||||||

For example, if a TCO investment of 60 million USD is made in Open RAN for 5G, the telecom should reach at least a Revenue of 80,44 million USD to be on a significant profit. When the TCO is 60 million USD, but the number of customers is 40 million, the telco is expected to be on a loss of 19,56 million USD.

Further sensitivity analysis is done for Profit from the perspective of two other variable parameters Number of customers in millions and TCO investment done for three years. For the previous example of a 60 million TCO investment for three years, the telecom should reach at least 30 million customers for three years to gain a cumulative profit of 16,68 million USD. With the same investment and 20 million customers, the telecom is expected to lose about 7,08 million USD. From here, it could be concluded that the smaller the telco is, the harder it is to compensate the investment in Open RAN infrastructure; nevertheless, its optimized cost by 30%. All the combinations are depicted in Table 6:

Table 6 Profit sensitivity analysis based on number of customers and TCO

| in ’000 USD | Number of Customers (in ’000) | |||||||||||

| 1,000 | 5,000 | 10,000 | 20,000 | 30,000 | 40,000 | 50,000 | 60,000 | 70,000 | 80,000 | 90,000 | 100,000 | |

| 10,000 | (2,224) | 7,280 | 19,160 | 42,920 | 66,680 | 90,440 | 114,200 | 137,960 | 161,720 | 185,480 | 209,240 | 233,000 |

| 20,000 | (12,224) | (2,720) | 9,160 | 32,920 | 56,680 | 80,440 | 104,200 | 127,960 | 151,720 | 175,480 | 199,240 | 223,000 |

| 30,000 | (22,224) | (12,720) | (840) | 22,920 | 46,680 | 70,440 | 94,200 | 117,960 | 141,720 | 165,480 | 189,240 | 213,000 |

| 40,000 | (32,224) | (22,720) | (10,840) | 12,920 | 36,680 | 60,440 | 84,200 | 107,960 | 131,720 | 155,480 | 179,240 | 203,000 |

| 50,000 | (42,224) | (32,720) | (20,840) | 2,920 | 26,680 | 50,440 | 74,200 | 97,960 | 121,720 | 145,480 | 169,240 | 193,000 |

| 60,000 | (52,224) | (42,720) | (30,840) | (7,080) | 16,680 | 40,440 | 64,200 | 87,960 | 111,720 | 135,480 | 159,240 | 183,000 |

| 70,000 | (62,224) | (52,720) | (40,840) | (17,080) | 6,680 | 30,440 | 54,200 | 77,960 | 101,720 | 125,480 | 149,240 | 173,000 |

| 80,000 | (72,224) | (62,720) | (50,840) | (27,080) | (3,320) | 20,440 | 44,200 | 67,960 | 91,720 | 115,480 | 139,240 | 163,000 |

| 90,000 | (82,224) | (72,720) | (60,840) | (37,080) | (13,320) | 10,440 | 34,200 | 57,960 | 81,720 | 105,480 | 129,240 | 153,000 |

| 100,000 | (92,224) | (82,720) | (70,840) | (47,080) | (23,320) | 440 | 24,200 | 47,960 | 71,720 | 95,480 | 119,240 | 143,000 |

| 110,000 | (102,224) | (92,720) | (80,840) | (57,080) | (33,320) | (9,560) | 14,200 | 37,960 | 61,720 | 85,480 | 109,240 | 133,000 |

| 120,000 | (112,224) | (102,720) | (90,840) | (67,080) | (43,320) | (19,560) | 4,200 | 27,960 | 51,720 | 75,480 | 99,240 | 123,000 |

| 130,000 | (122,224) | (112,720) | (100,840) | (77,080) | (53,320) | (29,560) | (5,800) | 17,960 | 41,720 | 65,480 | 89,240 | 113,000 |

| 140,000 | (132,224) | (122,720) | (110,840) | (87,080) | (63,320) | (39,560) | (15,800) | 7,960 | 31,720 | 55,480 | 79,240 | 103,000 |

| 150,000 | (142,224) | (132,720) | (120,840) | (97,080) | (73,320) | (49,560) | (25,800) | (2,040) | 21,720 | 45,480 | 69,240 | 93,000 |

| 160,000 | (152,224) | (142,720) | (130,840) | (107,080) | (83,320) | (59,560) | (35,800) | (12,040) | 11,720 | 35,480 | 59,240 | 83,000 |

| 170,000 | (162,224) | (152,720) | (140,840) | (117,080) | (93,320) | (69,560) | (45,800) | (22,040) | 1,720 | 25,480 | 49,240 | 73,000 |

| 180,000 | (172,224) | (162,720) | (150,840) | (127,080) | (103,320) | (79,560) | (55,800) | (32,040) | (8,280) | 15,480 | 39,240 | 63,000 |

| 190,000 | (182,224) | (172,720) | (160,840) | (137,080) | (113,320) | (89,560) | (65,800) | (42,040) | (18,280) | 5,480 | 29,240 | 53,000 |

| 200,000 | (192,224) | (182,720) | (170,840) | (147,080) | (123,320) | (99,560) | (75,800) | (52,040) | (28,280) | (4,520) | 19,240 | 43,000 |

| TCO (CAPEX OPEX) for 3 years. | ||||||||||||

5 Conclusions

As previously researched, Equipment vendors and System integrators are doing innovative services, while Telecom Operators and Service/Product vendors mainly deliver infrastructure innovations. This is proved with this research group as well. As a result of the survey conducted among this group of European operators on how they perceive Open RAN as a technology, it can be summarized that they all consider it disruptive BMI. Everyone hopes that through it, they will be able to optimize their costs and have the opportunity to offer new products and services.

The sensitivity analysis of whether there would be a return on investment in such technology shows that the profitability of a certain amount of money could only be recovered if the telco has more than a certain number of subscribers. This means that smaller telcos would be unable to recoup such an investment. This would either create a trend of consolidation between smaller telcos or takeovers and mergers so that their subscribers can benefit from the future services coming with the implementation of Open RAN. Another trend that could result from this is for cost innovation to happen in an open wound so that smaller operators can afford the investment. This could occur if more new and alternative providers of Open Ran technology come to market.

6 Future Research

Regardless of the analysis presented here, this is only one starting point of what may continue to be researched. Future studies could be done in several directions. One central area of research is the multiple architecture deployment combinations relative to the size of the telecom company. From the current research in this paper, it is clear that future investments in next-generation infrastructure become unprofitable below a specific telecom size. Does this mean that smaller telcos are looking to consolidate or merge with larger ones to achieve greater synergy in infrastructure investment? This is an exciting topic for future analysis.

Another big area is the future role of system integrators in implementing and maintaining all next-generation infrastructures. Due to the focus of this paper on telecom profitability, this expected trend for the crucial role of system integrators is not considered at all. But it is likely that the specific skills necessary for implementing and managing future networks will be brought precisely by the system integrators, who have quite developed cloud skills from the systems in the software industry.

Acknowledgement

The authors would like to acknowledge the support of the EU Project Motor 5G, Grant agreement ID: 861219 and the “Intelligent Communication Infrastructures R&D Lab” at Sofia Tech Park, Bulgaria (https://sofiatech.bg/en/).

References

[1] Yigit G., Chappell C., Bellis A., Monniaux G, Open RAN could deliver up to 30% TCO savings for operators with the right platform strategy and skill set, Analysys Mason, 2022.

[2] Wypioìr D., Klinkowski M., Michalski I., Open RAN – Radio Access Network Evolution, Benefits and Market Trends, Applied Sciences, 2022.

[3] Gabriel C., Kompany R., Open RAN: ready for prime time, Analysys Mason, 2021.

[4] Parallel Wireless, Everything you need to know about Open RAN, 2020.

[5] Kyoseva T., Lindgren P., Poulkov V., Radical and Disruptive Telecom Projects Based on Business Model, Innovation, River Publisher, Journal of Multi Business Model Innovation and Technology, Vol. 4, No. 3. pp. 179–214, doi: 10.13052/jmbmit2245-456X.432, 2018.

[6] Open RAN tutorial, https://telcocloudbridge.com/blog/open-ran-tutorial/https://telcocloudbridge.com/blog/open-ran-tutorial/

[7] Altiostar, RAN Transformation with Open Interfaces and Disaggregation, 2021.

[8] Faletski, I., Yes, You Can Make Money with Open Source, Harvard Business Review, 2013.

[9] Lee Y., Lee H., Lim J., vRAN Value Proposition and Cost Modeling, Samsung, 2020.

[10] Vierimaa O., Master’s Thesis “Cost Modeling of Cloud-Based Radio Access Network”, Aalto University School of Electrical Engineering, 2017.

[11] Chochliouros I., Kourtis M., Spiliopoulou A., Lazaridis P., Zaharis Z., Zarakovitis C., Kourtis A., Energy Efficiency Concerns and Trends in Future 5G Network Infrastructures, Energies, 2021.

[12] Paul H. Masur and Jeffery H. Reed, Artificial Intelligence in Open Radio Access Network, IEEE, 2021.

[13] Eriksson M., Is Open RAN the silver-bullet for the wireless industry?, Tietoevry, 2021.

[14] Telecom Infra Project, https://telecominfraproject.com/openran

[15] Mavrakis D., The road to Open RAN productization, ABI research/ Telecom Infra Project, 2021.

[16] VIAVI Solutions, O-RAN: An Open Ecosystem to Power 5G Applications, 2021.

[17] Brown G., Hodges J., Perrin S., 5G network & services strategies 2020 operator survey, Heavy Reading, 2020.

[18] Semov. P., Koleva P., Tonchev K., Poulkov V., Cooklev T., Evolution of Mobile Networks and C-RAN on the Road Beyond 5G, IEEE, 2020.

[19] The Goldman Sachs Group, 5G Moving from the lab to the launchpad, 2018.

[20] Taran Y., Boer H, Lindgren P., Towards a Business Model Innovation Typology, Aalborg University, Centre for Industrial Production, Denmark, 2012.

[21] Lindgren P., Advanced Business Modelling, Journal of MultiBusiness Model Innovation, River Publisher, 2016.

Biographies

Tsvetoslava Kyoseva is a PhD student at Technical University, Sofia, Faculty of Telecommunications. Her research field is in the area of disruptive innovations in the telecommunication industry. She graduated Master Degree of Telecommunications in Technical University, Sofia and holds an MBA in Innovation and Entrepreneurship at the University of Vienna. Mrs. Kyoseva is an experienced Innovations & Business Development practitioner, whose 20-year career path encompasses numerous managerial positions in renowned international telecom and tech companies. She was the lead of the first Telco Innovation Center in Bulgaria and has since worked with a large number of knowledge incubators and universities in the field of product innovation, beta-testing and market validation. She joins Methodia – a company providing innovative solutions for Utility and Telecom industries – in the spring of 2014 leading the Business Development, Projects & Innovations Department, while currently heads the company as a CEO.

Vladimir Poulkov PhD has received the M.Sc. and Ph.D. degrees from the Technical University of Sofia (TUS), Sofia, Bulgaria. He has more than 35 years of teaching, research, and industrial experience in the field of telecommunications, and has managed numerous industrial, engineering, R&D and educational projects. He has been Dean of the Faculty of Telecommunications at TUS and Vice Chairman of the General Assembly of the European Telecommunications Standardization Institute. He is Head of the “Teleinfrastructure” R&D laboratory at TUS, Head of the “Intelligent Telecommunication Infrastructures Laboratory” at Sofia Tech Park, Chairman of the “Cluster for Digital Transformation and Innovation”, Bulgaria. He is Senior IEEE Member and Fellow of the European Alliance for Innovation.

Peter Lindgren holds a full Professorship in Multi business model and Technology innovation at Aarhus University, Denmark – Business development and technology innovation and is Vice President of CTIF Global Capsule(CGC). He is Director of CTIF Global Capsule/MBIT Research Centre at Aarhus University – Business Development and Technology and is member of Research Committee at Aarhus University – BSS. He has researched and worked with network based high-speed innovation since 2000. He has been head of Studies for Master in Engineering – Business Development and Technology at Aarhus University from 2014–2016 and member of the management group at Aarhus University BTECH 2014–2018. He has been a researcher at Politechnico di Milano in Italy (2002/03), Stanford University, USA (2010/11), University Tor Vergata, Italy (2016/2017) and has in the period 2007–2011 been the founder and Centre Manager of International Centre for Innovation www.ici.aau.dk at Aalborg University, founder of the MBIT research group and lab – http://btech.au.dk/forskning/mbit/ – and is cofounder of CTIF Global Capsule – www.ctifglobalcapsule.org.

Journal of Mobile Multimedia, Vol. 19_4, 985–1008.

doi: 10.13052/jmm1550-4646.1943

© 2023 River Publishers