Impact of Disruptive Technology on Sustainable Enterprise Resource Planning (S-ERP)

Chulalux Soprakan and Supaporn Kiattisin*

Information Technology Management, Faculty of Engineering, Mahidol University, Salaya, Phuttamonthon, NakhonPathom, Thailand

E-mail: supaporn.kit@mahidol.ac.th

*Corresponding Author

Received 16 April 2020; Accepted 10 February 2021; Publication 18 June 2021

Abstract

In the 21st century, we face the disruptive technology in several ways; meanwhile, the business industry still needs a sustainable system for their ultimate goal as a competitive advantage in terms of differentiation focus or cost focus. This research provides the impact result once business utilizes emerging technology in their company. For the methodology, we use factors in technology adoption from the innovation diffusion theory (IDT) for new-technology selection. In the case study, we use simulation robotic process automation (RPA) installation in the routine business process to estimate business impact. Accounting tools such as payback method (PP), net present value (NPV), internal rate of return (IRR) are used to estimate cost savings and return on investment. RPA is one of many technologies that can work collaboratively with the existing enterprise resource planning (ERP) system, new technology, and business process improvement (BPI) process. The experience results show that the RPA provides time-saving 14 times in total processes with payback result in 3.6 years and 52% IRR.

Keywords: Digitalization in business, sustainability, enterprise resource planning (ERP), sustainable development goals (SDGs), robotic process automation (RPA).

1 Introduction

In the last four decades, the development of science and technology was leading to economic growth. The digital era is an era of the fundamental transformation of business processes and practices. One of the most fundamentals of digital transformation in the manufacturing environment is the development of enterprise resource planning (ERP) systems, which integrate flows of information and communication through the organization to streamline the firm’s business processes at all levels [1]. Once the domain of large international firms, ERP systems are increasingly being adopted in globalized markets and developing countries and by small- and medium-sized enterprises (SMEs) [1–3]. But there was a lot of impact and damage to world resources. At present, all aspects of development will have a goal for sustainable growth together including business, industry, environment, and society. The United Nations (UN) has set a framework for enhancing the standard of living of people around the world. These target frameworks called sustainable development goals (SDGs) were launched in September 2015. This goal is used as a framework for driving the world for 15 years [4].

The triple bottom line (TBL) approach is one principle notion highlighted to operationalize sustainability [15]. The traditional firms require the digital competencies to sustain in their business. Traditionally, the conceptual relationship between ERP and supply chain management (SCM) mainly focused on the concept with ERP cycles that impact the SCM system [5].

The sustainability development exposition is related to three engagement goals: environmental, economic, and social. The SDGs, which were adopted by the UN General Assembly in 2015 for application to 2030, include ambitious goals of eliminating poverty and hunger; acting for health, education, and gender equality along with clean water and sanitation and affordable clean energy; improving industry, innovation, and infrastructure; reducing inequality; developing sustainable cities; and meeting a variety of other climate and political goals [6].

There is still infrequency in academic research to study sustainable information system solutions such as sustainable enterprise resource planning (S-ERP). Project implementation lifecycle method is the framework to enlarge from traditional ERP into S-ERP [7]. Business, process, service, and data are enterprise interoperability barriers concern of sustainable enterprise [8]. Today, digitalization is influenced by routine lifestyle [9]. Mobile multimedia, or media communication via mobile technology and mobile data service, has become one of the most common sources of entertainment, news, and information around the world. By 2019, there was an estimated 4 billion mobile Internet users around the world, accounting for 52% of the world’s web traffic [10]. Mobile multimedia is particularly prevalent in Asia and Africa, where mobile networks have rolled out ubiquitous connectivity in the absence of traditional land-based Internet connectivity. Mobile apps, or programs designed to work on mobile platforms and through mobile data, are highly popular as a consequence of the high rate of mobile multimedia adoption. According to one estimate, there were 204 billion app downloads in 2019 or an average of about 51 downloads per user [11]. Therefore, it can be stated that mobile apps, which connect to the global multimedia network, are one of the most effective platforms today. One of the areas where ERP has been implemented in practice is robotic process automation (RPA) [12–14].

This study is organized as follows. Section 2 presents a literature review that is presented in terms of ERP, sustainability development, S-ERP, SCM, business model, and what is to be developed in terms of 17 goals to transform our world [4]. This paper investigates the linkage between S-ERP, SCM that impact the sustainability perspective the target that responsive to SDGs goals. Automating routine work in ERP areas such as accounting and finance, payroll and benefits, and application processing, as well as sales-related clerical work, helps increase processing speed, eliminate human error, and improve efficiency, allowing the firm to devote its human workforce to areas with much higher value [13].

2 Literature Review and Related Research

This section will represent related review of the research.

• In general, the research methodology is a literature review. An assortment literature search was conducted using Scopus and Web of Science, and searching keywords are one or any combinations of “Enterprise resource planning” + “(sustainab*)” + “Supply chain management” + “Business Model”+ “Measu*” + “RPA.” Initially, 100 articles were found after preliminary screening of the title and the abstract.

2.1 Sustainability

An example of a commonly used sustainability theory is the TBL model, which argues that businesses must consider not just economic performance but also environmental and social performance in their business activities [15]. Although sustainability is patently important, various theoretical frameworks of sustainability have not been effective at mitigating environmental damage or having other real-world effects [16]. This problem may be attributable to the lack of conspiracy theories and the disconnection between theory and practice. Business interest in sustainability has also been slow to emerge, even though partnerships and reporting have been a concern since the turn of the century [15]. Sustainable SCM has only been a major concern of either business or academic study since around 2010 [17]. The effective implementation of sustainability is still a concern.

2.2 Enterprise Resource Planning

ERP systems are “complex software packages that integrate information and business processes within and across functional areas of business” [18]. ERP systems, which are complex, expensive, and demand high levels of user and technology resources from the organization, have historically been the domain of large companies [18]. Increasingly, however, ERP systems are implemented in smaller firms in developing countries, as the technology has become less expensive and more usable [1–3].

2.3 Sustainable Enterprise Resource Planning

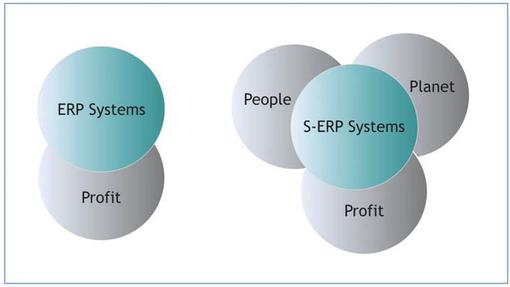

Modern firms must meet not just economic objectives but also environmental objectives, both for their sustainable business activities and to meet institutional goals such as the SDG [15, 19]. This can be a complex challenge; for example, firms implementing sustainability goals in their supply chain may face significant integration and implementation issues, which are not well-understood to date [20–22]. S-ERP systems are IT systems that are designed to integrate information flows and processes in the organization to achieve environmental sustainability, incorporating sustainability into the ERP model (Figure 1) [7, 23, 24]. Specifically, S-ERP systems are designed to overcome challenges that firms have with collecting and analyzing information effectively to optimize operations for sustainability objectives [7]. S-ERP systems are mostly in use by larger firms but may also be used in some cases by smaller firms to achieve specific environmental objectives [25]. As with a standard ERP, S-ERP is a complex process that requires detailed planning and organizational resources and may be prone to failure [23, 24, 26]. There are also significant gaps in implementation practice including technology, engineering, computational, information, and computational barriers [27]. Thus, while standard ERP systems are a mature technology, S-ERP technologies are just beginning to develop.

Figure 1 Philosophy of ERP and S-ERP systems [24].

2.4 Robotic Process Automation

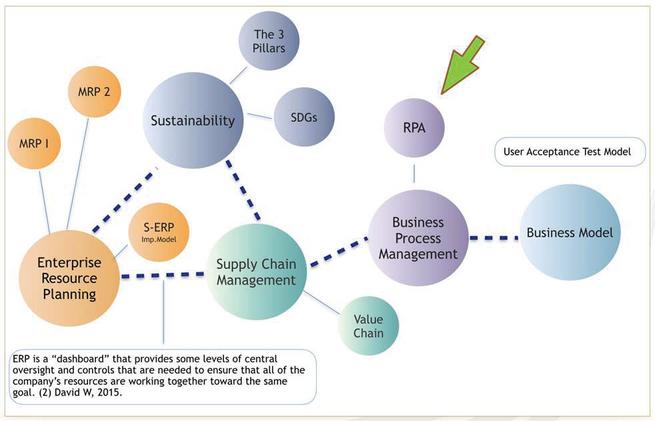

Another emerging technology is that of RPA. RPA, or automation of routine administrative and business functions such as accounting and finance and some human resource functions, has only emerged as a business practice within the past few years [13, 28]. RPA is one of a constellation of related business process management tools, which have similar aims but different processes (Figure 2). RPA is not a physical robotics process but, instead, depends on artificial intelligence technologies for the facilitation of decision-making [29]. The drive for RPA is based on business objectives to improve the efficiency of back-office operations, which serve as support functions for the firm’s value chain [29]. For example, RPA allows firms to centralize, standardize, and relocate back-office processes and automate them to improve efficiency. To date, there has been little academic research published on RPA, although there have been case studies at organizations such as Telefónica/O2 (a telecommunications company) and a business process outsourcing (BPO) firm which have demonstrated its use and effectiveness [29, 30]. Therefore, like S-ERP, RPA is an immature technology. However, given that it is designed to free human workers for higher-value work, it has the potential to contribute to SDG goals including business innovation and human capital improvement.

Figure 2 The constellation of business-oriented services; ERP, sustainability, S-ERP, SCM, business process management (BPM) to business process improvement (BPI).

In this study we simulate a new technology installation by applying RPA in routine business process to determine improvements in everyday operations efficiency and cost.

2.5 Innovation Diffusion Theory

The innovation diffusion theory (IDT) is a process model of innovation adoption [31, 32]. The IDT model argues that the initial adoption decision is a five-stage process, in which knowledge and persuasion surrounding the technology result in a decision to adopt the technology; following this adoption decision, implementation either confirms or rejects the expected benefits. However, innovations are not adopted in a vacuum; instead, social capital (or skills and resources) and networks of opinion leaders determine whether a technology is viewed as adoptable. At some point, the innovation reaches critical mass and becomes a mainstream technology rather than an innovation; it then becomes mature and then declines and is superseded by new technologies [31, 32]. However, IDT does not imply that innovation diffusion is inevitable; in fact, most innovations fail to diffuse and do not make it through a full lifecycle, while others may be discontinued early in the lifecycle [33].

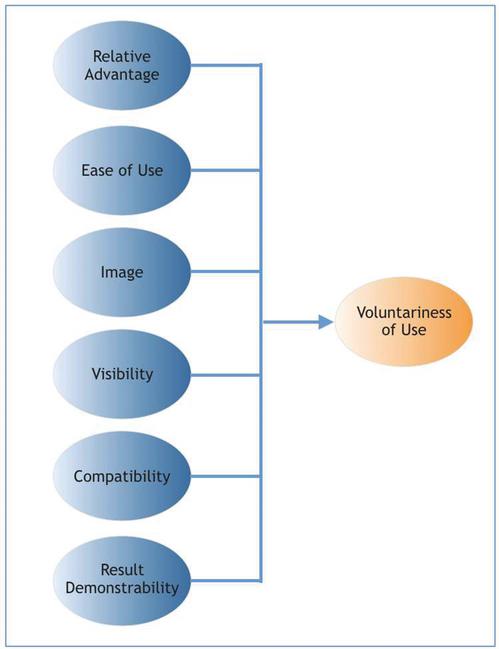

This raises the question of what factors influence the adoption decision and ultimately the diffusion of the technology. Some of the factors that may influence the adoption of an innovation include the relative advantage the technology offers, its ease of use, its image, compatibility with existing systems, demonstrability of results, and visibility of results [31]. Some of these dimensions, such as ease of use, are consistent with individual models of technology adoption such as the unified theory of acceptance and use of technology (UTAUT) and technology acceptance model [34–36]. However, the IDT acknowledges that diffusion of innovations between businesses is not solely driven by individual preferences, but also by organizational imperatives [31]. For example, one case showed that adoption of 3D printing technology was driven by the relative competitive advantage that the technology gave the firm over its major competitors, along with ease of use and trialability (which was a way to test the system and ensure it met organizational needs) [37]. Another study, investigating the adoption of management accounting, found that relative advantage including costs and benefits, along with individual benefits, influenced adoption, but compatibility, complexity, observability, and trialability also influenced adoption [38]. Therefore, these dimensions may apply differently to different technologies, but there is likely to be some aspects of each included.

Figure 3 Factors in technology adoption according to IDT (adapted from [31]).

IDT is a complex theoretical model and does suffer some weaknesses. For example, bias may be introduced into the results if only a single level of analysis (for example, only organizational or individual adoption) is considered [39].

There are also some gaps in the model. For example, although the IDT does include aspects like trialability and visibility of results, it does not include the more straightforward metric of perceived usefulness, which measures what the technology can do for the organization and its users [34–36]. Finally, there is a fundamental issue of trust in the underlying technology, which can inhibit adoption in early stages before social proof emerges [31, 40]. Thus, the organizational adoption of an innovation is more complex than stated in the simple IDT. In this study, we will simulate a new technology installation based on IDT theory.

3 Methodology

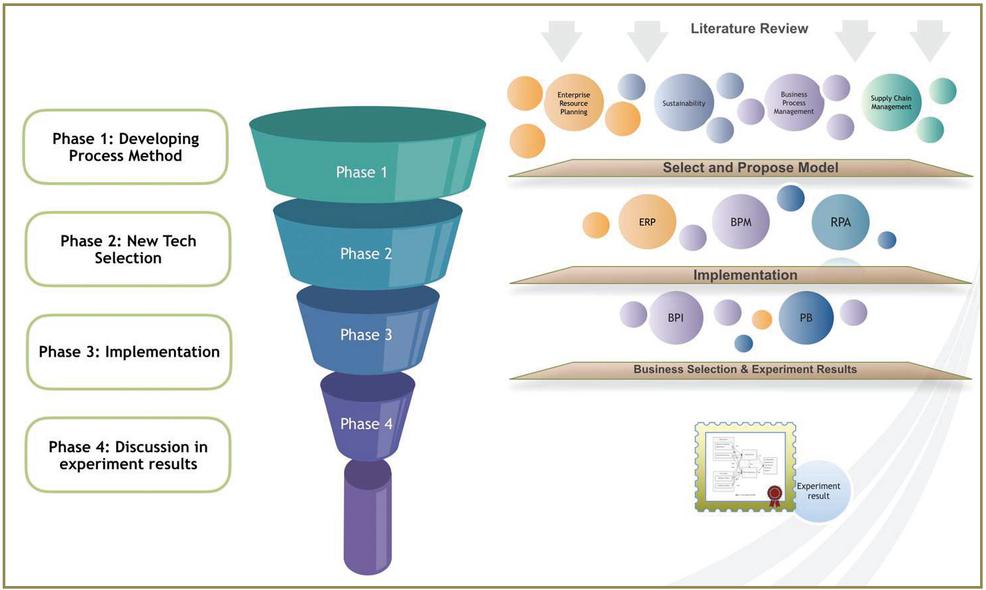

Phase 1: Developing process method. This phase uses author’s empirical knowledge starting with ERP, project management (PM), and IT management to select projects conceived for the experiment. This paper focuses on S-ERP that is the conclusion of PM and ERP [7].

Phase 2: New technology selection. This phase selects one of the disruptive technologies that impact post-modern ERP based on seamless process and data accuracy [41]. RPA and several immerging technologies, such as open character recognition (OCR), Internet of Things (IoT), and application program interface (API), were decided for implementation phase.

Phase 3: Implementation. The Key importance in the phase is business process improvement (BPI) for process selection. The project team consists of Project Manager, IT Application Manager, Business Process Owner (BPO), RPA Implementer, Managing Director (MD), and Financial Analyst.

Phase 4: Discussion in experiment results. After RPA implementation, we compare time-saving and cost-saving. These imperatives include the need to generate competitive advantage or a way to use the firm’s resources in a way that competitors cannot match [42–44] and result analysts. The solutions concentrate on emerging technology acceptance 2 of Implementers, 2 of Management, and 2 of BPO.

Figure 4 Research methodology for experiment phase.

The objective of this phase is to analyze the proper activity and select the routine task list for the RPA implement. For these selected processes flows, we need hands-on routine activity from the employee jobs to robotics jobs without any lean process activity to prove the time-saving rate and goal to enterprise cost saving (Figure 4).

3.1 Case Study

ABC Company is the services unit industry; they have more than 10 branches with 10–12 employee headcounts per branch for building management. They consist of back office activity, document support, and building engineering services. In this phase, we focus on routine back office process workflow that needs to be improved by RPA (Table 1).

Table 1 Services unit process flow selected to RPA implementation

| Number of Process Flow | |||

| Department | Total Number of Process Flow | Human | Robot |

| Admin | 17 | 15 | 2 |

| Accounting | 22 | 9 | 13 |

In the ERP business process selection, we are mapping process with ERP module and use several emerging technologies per selected back office business workflow, including with OCR, IoT, and API to complete the business process in terms of process-related. The highlight selected process is billing process under account receivable (AR) module. We implement 100% human process by using smart water-meter to collect usage data before interface data via API to the enterprise ERP system.

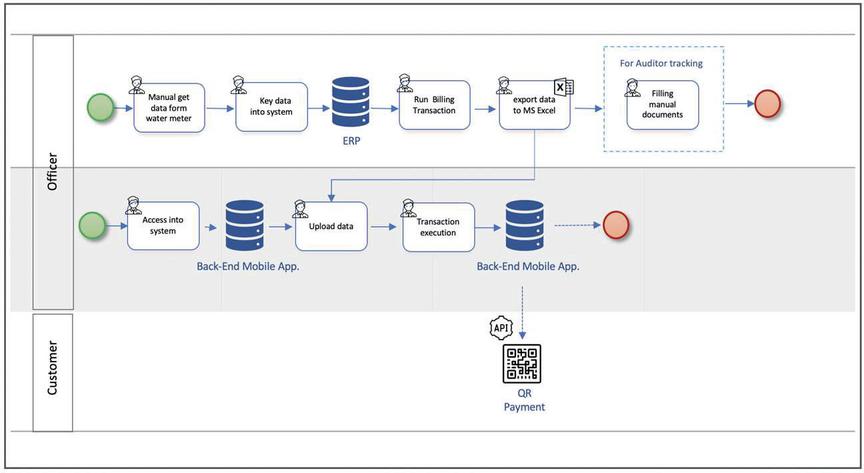

The using case was carried out on a process for the generation of a billing via mobile application by using QR payment feature. The existing process described in Figure 5 starts by the billing water usage for monthly expense billing process. Once time schedule’s payment cycles a document support – officer goes to the physical water-meter to do data collection in the worksheet by manually taking note in his worksheet. And he does record into MS-Excel template for uploading into ERP system within the module AR transaction – billing. Then he executes the billing transaction by the customer list. Once done, the officer needs to export data for auditor tracking and keep filing into MS-SharePoint.

Figure 5 As – is AR module – billing process via mobile application with QR payment.

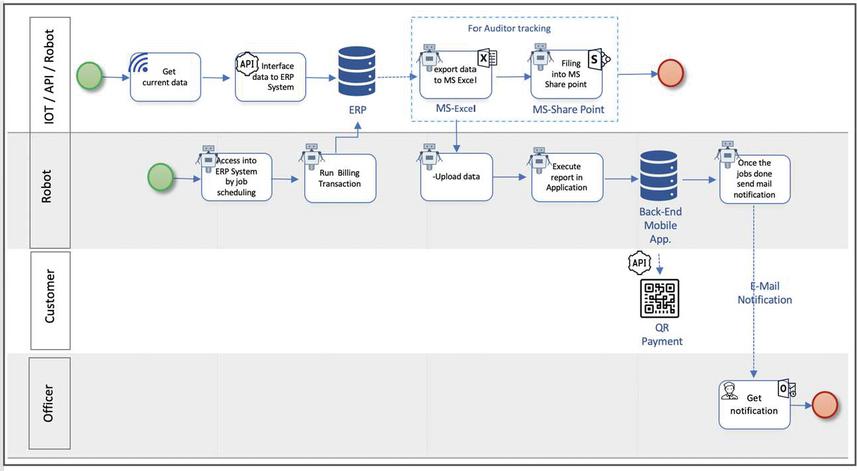

In this case, we allow to use mobile application to QR payment feature. In this century, digital technology disrupts the existing information technology in several ways. Moreover, we allow to use mobility with Financial Technology (FIN-Tech), IoT in smart water meter, API, RPA, ERP system, Microsoft SharePoint (MS-SharePoint), and Microsoft Outlooks as well.

For the sample scenario, we implement RPA to replace the user manual transaction (see Figure 6). The smart water-meter installation works together with API to interface data into Living OS_ERP System. RPA automates the transaction, starting from accessing the ERP system, executing the billing transaction, exporting data to fill the forms, and using the exported billing data to upload into the backend of the mobile application module ‘bill to customer’. The bill is then sent directly to the customer with the QR payment feature. When the job is done the RPA process end job by sends an e-mail notification.

Figure 6 TO-BE automated process AR module, billing process via mobile application with QR payment.

To analyze the financial feasibility for the divisions and prioritize investment, including making sure the investment decisions are appropriate and effective, there are financial tools that have been developed previously. First, we have estimated cash flow projections that are expected to occur in the future, and then we calculate through various important tools as follows: payback period (PP), net present value (NPV), and internal rate of return (IRR).

3.2 Payback Period (PP)

The time required for the cash inflows generated from the project to compensate for the initial cash flow is called the payback period. There are two ways to calculate the payback period which are as follows.

3.2.1 Averaging method

Divide the cash flows that are supposed to receive every year into the initial expenses for the assets. This method works best when cash flows are supposed to be stable in subsequent years.

3.2.2 Subtraction method

Remove the single annual cash flow from the existing cash flow until the payback period is reached. This method works best when cash flow is expected to change in the years to come. A significant growth in future for many years may result in incorrect payback periods if using the method for finding averages.

Please note that, for both cases, the calculation based on cash flow does not account net income (the subject is non-cash adjustments). The periods of payback concept are generally used to create budgets and finance. But it is also used to check the cost of energy saving technology. PP can be used by senior managers to select from among many potential investments, since even large companies cannot fund all investment opportunities. The reason is that the board of directors wants to ensure that the organization does not invest in a risky venture. Microsoft Excel is the simplest way to calculate PP.

The formula we will use to compute a PP is as follows:

3.3 Net Present Value

NPV refers to the present value of future cash flows from an investment or project [45]. NPV is discounted, meaning that it is calculated with respect to the discount rate, adjusting the future cash flows to current value [45]. NPV can be calculated using the following equation:

where R is returns in time period t, and i is the discount rate in time period t [46]. NPV is used in management decision making to compare and select investments based on estimated total cash flows [47].

3.4 Internal Rate of Return

The IRR is a modification of the NPV which estimates the discount rate at which the present cash flows would be zero [45]. This rate can be estimated using the same equation as NPV but solving for I rather than R [46]. Like NPV, IRR is used to compare the future cash flows of the proposed investment projects in order to select the project that will have the best return, given the available funding options for each project [47].

4 Results

4.1 Time Savings

The first set of results (Table 2) addresses the average processing time for each of the types of routine business processes where the RPA experiment was conducted. The four types of business processes included electricity usage information report, water usage information report, telephone usage information report, and monthly reports. As this analysis shows, the use of RPA significantly reduced the amount of time required on average for processing of each of these types of reports. For the electricity usage information report, the RPA process took 30 seconds on average compared to 60 seconds for the human process, representing a reduction of 50% in time. For the water usage information report, the RPA process took approximately 20 seconds compared to 60 seconds for the human process, representing a reduction in time of 66.7%. For the telephone usage information report, the RPA process took approximately 40 seconds, compared to 60 seconds for the human process, for a reduction in time of 33.3% for the process. The most extreme reduction was seen in the monthly report process, which took 90 seconds for the RPA process compared to 3600 seconds (or 1 hour) for the human process. This was a reduction in time of 97.5%. Thus, the results of the experimental process showed that all RPA processes had a significant reduction in time, ranging from 20 seconds (for the telephone usage information report) to 58.5 minutes (for the monthly report). Thus, the analysis continued to the calculation of savings.

Table 2 Processing time experiment results

| Evaluated Process Time | ||||

| Function/Activity | % | Human | RPA | |

| 01 | Electricity usage information | 50 | 60 seconds | 30 seconds |

| 02 | Water usage information | 66.67 | 60 seconds | 20 seconds |

| 03 | Telephone usage information | 33.33 | 60 seconds | 40 seconds |

| 04 | Monthly report | 97.50 | 3600 seconds | 90 seconds |

4.2 Financial Projections

The financial calculations (Table 3) show that the payback period (PP) of the project is 3.16 years. The NPV is 8,537,819 baht, leading to an IRR of 52%. Given that the risk-free rate in Thailand is 1.27% as of the time of writing (January 2020) [48], it would be exceptionally surprising if the company had to pay a high enough interest rate that it would not at least break even on its cash flows with a 52% IRR. Ultimately, this project is estimated to have a net five-year savings of 567,464 baht with an initial capital outlay of 702,200 baht, indicating that this is a relatively high return investment even within the first five years. Thus, the initial assessment of the project’s financial projections indicates that the project is financially viable.

A more detailed assessment of the program cost and savings explains how these savings are achieved in the first five years (Table 4). The cost savings associated with the project comes from the reduction in staff for the administrative department from 22 members to 13 members, representing a manpower savings of 9 full-time staff members. This reduction in staff results in the first year in a savings of 25,000 baht/month per staff member or 2.7 million baht over the course of the year. The estimated annual growth rate of these savings is 2%, which was taken from the firm’s financial records, which indicated that administrative staff receives an average of 2% annual raise. Thus, by the end of year 5, the annual savings is 2,955,567 baht per annum.

Table 3 Financial calculations and results summary

| Calculation | Finding |

| Initial capital investment | 702,200 baht |

| Payback period | 3.16 years |

| NPV | 8,537,819 baht |

| IRR | 52% |

| Net savings (five years) | 567,464 baht |

Table 4 Achievement of savings over the first five years of the project

| Program Year | |||||

| Cash in | 1 | 2 | 3 | 4 | 5 |

| Cost savings | |||||

| Growth rate (2%) | 1.00 | 1.02 | 1.04 | 1.06 | 1.08 |

| Site cost (9 FTE) | 9 | 9 | 9 | 9 | 9 |

| Admin (25,000 baht/month) | 2,700,000 | 2,754,000 | 2,809,080 | 2,865,262 | 2,922,567 |

| Total | 2,700,000 | 2,754,000 | 2,809,080 | 2,865,262 | 2,922,567 |

| Cash out | |||||

| Program cost | 150,700 | 150,700 | 150,700 | 150,700 | 150,700 |

| Implementation | 627,200 | ||||

| PC set | 75,000 | ||||

| Admin and selling expenses | 72,904 | 72,904 | 72,904 | 72,904 | 72,904 |

| Profit sharing | 1,296,000 | 1,296,000 | 1,296,000 | 1,296,000 | 1,296,000 |

| Center admin | 348,000 | 354,960 | 362,059 | 369,300 | 376,686 |

| Center finance | 648,000 | 660,960 | 674,179 | 687,663 | 701,416 |

| Total | 3,217,804 | 2,535,524 | 2,555,842 | 2,576,567 | 2,597,706 |

| Net cash | (517,804) | 218,476 | 253,238 | 288,694 | 324,860 |

| Cumulative Net cash flow | (517,804) | (299,328) | (46,090) | 242,604 | 567,464 |

The cash out related to the project includes the program cost (fixed at 150,700 per annum for the first five years). During year 1, it also includes the implementation costs (estimated at 627,200 baht) and the PC hardware setup required for the program (estimated at 75,000 baht). During all five years, there are administrative and selling expenses, profit sharing, and admin and finance center costs that accrue to the program from its operations. These annual operational costs rise at the same rate of 2% used to estimate the increase in staff savings.

The net cash flows in Table 4 show that, on an annual basis, the project is only in the negative in year 1, which is due to the 702,700 baht cost associated with implementation and PC setup. In all four subsequent years, the cash flow of the project is positive. The cumulative cash flow, however, remains negative for three years, as cash flows (savings) accrue to pay back the initial investment.

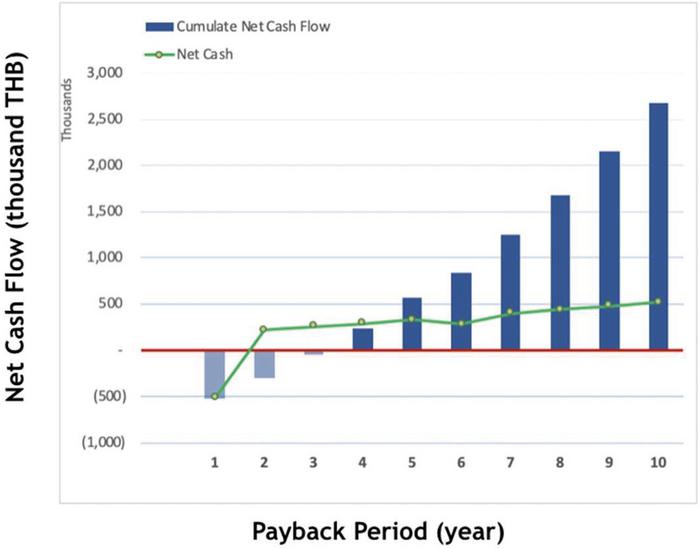

The payback period is illustrated in Figure 7. As it shows, the net cash flow remains negative throughout the first three years of the project. However, after this point, the project becomes positive in its revenues and continues to rise each year as the cumulative net cash flow rises. By year 10, it is estimated that the annual net cash flow will reach 516,834 baht in savings from the staff reduction associated with RPA. By this point, the cumulative net cash flows (net savings) will have reached 2,675,722 baht. Given that the net savings at five years was 567,464 baht (Table 3), this shows that the savings accelerate in the second half of the estimation cycle. Overall, the ten-year cumulative net cash flows for the project are 3.81 times the initial investment of 702,200 baht.

In summary, the financial analysis of the project demonstrates that it is not only financially feasible as an initial investment but that the cost savings associated with the project would be significant, especially in the second five years of the project.

Figure 7 Experiment result.

5 Discussion

This study had two key findings. The first key finding was that RPA represented significant time savings, reducing the amount of time required for a sample report between 33.3% and 97.5% and, in the case of the longest report, reducing the runtime from 1 hour to about 1.5 minutes. The second key finding is that the project would be financially feasible, generating cumulative cost savings of 567,764 baht by the end of year 5 and 2,675,722 baht by the end of year 10. The cost savings were generated by the reduction in manpower of the administrative workforce from 22 staff members to 13 staff members, resulting in the elimination of nine positions.

These findings are broadly consistent with what is known about RPA and its effect on process time and cost but did show that the case firm had better results compared to other studies. For example, one study investigated the effect of RPA on back office business processes [30]. These authors showed that while RPA did result in productivity improvements, it did not actually reduce the amount of time required for the project or report. It is likely that this difference is due to inherent differences in the efficiency of the respective case organizations, particularly since the case organization in the present research had inefficient processes (particularly the monthly report process, which was where the majority of the gains were seen). Another study, however, did show some significant improvements in the amount of time required for the project [29]. Therefore, these results were consistent with the limited expectations set by the literature on RPA in process.

RPA is still a relatively new process, having only emerged within the past several years as a discrete practice (although it is based on somewhat older technologies) [13, 28]. This means that there is still a lot to learn about RPA and what situations it is most effective in. From the findings of this research, it is possible that even if only the most costly and lengthy processes a firm runs were replaced, the RPA could be beneficial, as the total time savings (and therefore the total cost savings) were significantly higher for this report compared to any other. However, with so little research having been previously conducted on RPA and its implementation [29, 30], this is not certain. Thus, this research has supplemented the academic literature on RPA and how firms benefit from it, but there is still much research to be done in this area.

These results, unlike previous studies conducted, have demonstrated the potential financial savings of RPA for the adopting organization, showing that adoption would be feasible for firms that could achieve the level of efficiency gains as the case firm did. However, it is not certain to what extent this business case for the adoption of RPA would influence its adoption speed. Wilcocks, Lacity, and Craig noted that RPA as a process paradigm only emerged in around 2012, and, as of 2015, it was still at a very low level of adoption by firms. This has not changed significantly in recent years, with little evidence of an explosion in the adoption of RPA. This raises the question of how RPA is viewed by firms and whether it will be adopted as a business practice [29].

IDT can be applied to consider the current situation of RPA and its likely future. IDT describes the process of innovation and its interaction with the surrounding environment [31, 32]. Perhaps, one of the most important insights for RPA during its innovation phase (pre-widespread adoption) is that at this stage, diffusion is a social process in addition to a technological process and an economic decision [31, 32]. Thus, even though firm managers may be able to rationally assess the feasibility of RPA adoption and the (potential) economic gains that could result from its adoption, there may as yet be inadequate social support for the adoption of the process. Another complication of RPA is that it is dependent on the adoption of other technologies, particularly ERP systems. This is problematic because the implementation of ERP systems is complex and not fully understood and, therefore, prone to failure [20–22]. The result of this is that the technology may not be considered easily implemented or used, which is a prerequisite for technology adoption at the firm level [34–36]. Thus, in order to achieve mainstream adoption as an innovation technology, it is not enough that RPA should be useful or cost-effective. Instead, it needs to be more easily implemented than it is today.

6 Conclusion

This research investigated the implementation of RPA in a case firm in Thailand. The results of the study were generated from experimental application of RPA in the four most commonly used administrative reports in the firm. The findings showed that the implementation of RPA could save the firm anywhere between 20 seconds and 58.5 minutes in production of a report, representing a reduction of between 33.3% and 97.5% of the total time required for these critical reports. Based on these time savings, it is projected that the firm could achieve savings of around 2.7 million baht per annum (increasing with inflation) due to the reduction of administrative workforce from 22 staff members to 13 staff members. This resulted in a payback period of 3.16 years, along with an estimated five-year cost savings of 567,464 baht. Thus, from a practical point of view, the implementation of RPA to automate some of the most complex and troublesome parts of the firm’s reporting and administrative work was cost-effective. In conclusion, this research has shown the practical value of RPA from a business perspective, demonstrating that it has the potential to save firms significant time and money that outweigh the financial cost of implementation.

The most important implications of this research are for practice. Specifically, the findings provide a strong business case for RPA, particularly for firms that already have an ERP system in place and that have high administrative overheads associated with its use. Firms that could benefit most from RPA are those with detailed manual processes for everyday reporting, which follow a process that cannot be fully coded into an automated report but which have set parameters that could work well with the AI basis of RPA. These firms should investigate RPA and consider whether the returns would be worth it for them. This research also has academic implications because it is one of the first studies that have assessed the suitability of RPA in an empirical perspective. The findings showed that RPA does have strategic benefits, which is new knowledge considering the novelty of RPA as a business process and the lack of academic knowledge surrounding the topic.

This research does have some important limitations. As a case study, the findings only apply to a single firm. This means that other firms, which may have more efficient (or less efficient) processes, may not recognize the same level of concern. Another limitation is that the findings only apply to firms that already have ERP systems in place since implementation of ERP would be considerably more expensive and difficult. The limitations open up some opportunities for additional research. For example, more studies could be conducted that investigate the characteristics of RPA implementation and what kinds of firms could benefit most from implementation. Another area for future research is investigation of the adoption of RPA and what factors have influenced firms to adopt the process, including both technology and social factors, as this is still poorly understood.

References

[1] C.J. Costa, E. Ferreira, F. Bento, and M. Aparicio, “48.Enterprise resource planning adoption and satisfaction determinants”, Comput Human Behav, vol. 63, pp. 659–671, 2016.

[2] S. Ranjan, V.K. Jha, and P. Pal, “Application of emerging technologies in ERP implementation in Indian manufacturing enterprises: an exploratory analysis of strategic benefits”, Int J Adv Manuf Technol, vol. 88, pp. 369–380, 2017.

[3] I. Vlachos, “SMEs E-business Behaviour: A Demographics and Strategic Analysis”, J. Enterp. Resour. Plan. Stud., vol. 21, pp. 1–21, 2012.

[4] United Nations, 2015, Available from https://www.un.org/development/desa/disabilities/envision2030 (accessed 02.12.18).

[5] H.A. Akkermans, P. Bogerd, E. Yucesan, and L.N. Wassenhove, “The impact of ERP on supply chain management”, Eur. J. Oper. Res., vol. 146, pp. 284–301, 2003.

[6] United Nation, “Transforming Our World: The 2030 Agenda for Sustainable Development. A New Era World: The 2030 Agenda for Sustainable Development, A New Era in Global Health, 2020, Available from https://doi.org/10.1891/9780826190123.ap02

[7] A.G. Chofreh, F.A. Goni, A.M. Shaharoun, S. Ismail, and J.J. Klemeš, “Sustainable enterprise resource planning: Imperatives and research directions”, J. Clean. Prod., vol. 71, pp. 139–147, 2014.

[8] Y. Ducq, D. Chen, and G. Doumeingts, “A contribution of system theory to sustainable enterprise interoperability science base”, Comput. Ind., vol. 63, pp. 844–857, 2012.

[9] P. Saunders, D. Ganly, and M. Guay, “Strategic Roadmap for Postmodern ERP. Gartner, Inc.”, ID: G00327361, 2018, Available from www.gartner.com/doc/384665/-strategic-roadmap-postmodern-erp (accessed 14.06.18).

[10] Statista. “Mobile Internet usage worldwide-statistics and facts”. 2019a, Sep 11, Available from https://www.statista.com/topics/779/mobile-internet/

[11] Statista. “Mobile app usage-statistics and facts”. 2019b, Aug 1, Available from https://www.statista.com/topics/1002/mobile-app-usage/

[12] B. Diepeveen, J. Matcher, and B. Lewkowicz, “Robotic process automation-Automation’s next frontier”, Fron. Artif. Intel. App., vol. 212, pp. 108–119, 2016.

[13] KMPG, “Robotic Process Automation (RPA) What Is RPA and Digital Labor?”, [WWW Document], 2018.

[14] T. Torlone, R. Howell, F. Ip, and A. Mahajan, WEase of deployment”, PwC., vol. 39, pp. 61–70, 2016.

[15] J. Elkington, “Cannibals with forks: The triple bottom line of 21st century business”. Gabriola: New Society Publishers, 1998, pp. 37–51.

[16] S.E. Wallis and V. Valentinov, “What is Sustainable Theory? A Luhmannian Perspective on the Science of Conceptual Systems”, Found. Sci., vol. 22, pp. 733–747, 2017.

[17] P. Beske-Janssen, M.P. Johnson, and S. Schaltegger, “20 Years of Performance Measurement in Sustainable Supply Chain Management-What Has Been Achieved?”, Supply Chain Manag., vol. 20, pp. 664–680, 2015.

[18] J.K. Nwankpa, “ERP system usage and benefit: A model of antecedents and outcomes”, Comput. Human Behav., vol. 45, pp. 335–344, 2015.

[19] UN Department of Public Information, “Transforming Our World: The 2030 Agenda for Sustainable Development. A New Era World: The 2030 Agenda for Sustainable Development, A New Era in Global Health”, 2018, Available from https://doi.org/10.1891/9780826190123.ap02

[20] G. Büyüközkan, and F. Güçer, “Digital Supply Chain: Literature review and a proposed framework for future research”, Comput. Ind., vol. 97, pp. 157–177, 2018.

[21] D. Ivanov, A. Das, and T. Choi, “New flexibility drivers for manufacturing, supply chain and service operations,” Int. J. Prod. Res., vol. 56, no. 10, pp. 3359–3368, 2018.

[22] M. Seuring and M. Müller, “From a literature review to a conceptual framework for sustainable supply chain management,” J. Clean Prod., vol. 16, pp. 1699–1710, 2008.

[23] A.G. Chofreh, F.A. Goni, and J. Klemeš, “A roadmap for Sustainable Enterprise Resource Planning systems implementation (part III)”, J. Clean. Prod., vol. 174, pp. 1325–1337, 2017.

[24] A.G. Chofreh, F.A. Goni, S. Ismail, A.M. Shaharoun, J. Klemeš, and M. Zeinalnezhad, “A master plan for the implementation of sustainable enterprise resource planning systems (part I): concept and methodology”, J Clean Prod, vol. 136, pp. 176–182, 2016.

[25] B. Shirazi, “Towards a sustainable interoperability in food industry small & medium networked enterprises: Distributed service-oriented enterprise resources planning”, J. Clean Prod., vol. 181, 109–122, 2018.

[26] A.G. Chofreh, F.A. Goni, and J. Klemeš, “Sustainable enterprise resource planning systems implementation: A framework development,” J. Clean Prod., vol. 198, pp. 1345–1354, 2018.

[27] G. Weichhart, A. Molina, D. Chen, and L.E. Whitman, “Challenges and current developments for sensing, smart and sustainable enterprise systems,” Comput. Ind., vol. 79, 2016, doi:10.1016/j.compind.2015.07.002.

[28] EY, “Robotic process automation - Automation’s next frontier”, [WWW Document], 2016.

[29] L.P. Willcocks, M. Lacity, and A. Craig, The IT function and robotic process automation, London: The London School of Economics and Political Science, 2015.

[30] S. Aguirre and A. Rodriguez, Automation of a Business Process Using Robotic Process Automation (RPA): A Case Study. In: J. Figueroa-García, E. López-Santana, J. Villa-Ramírez, and R. Ferro-Escobar (Eds), “Applied computer sciences in engineering,” WEA 2017. Communications in Computer and Information Science, vol. 742. Springer, Cham, 2017.

[31] E.M. Rogers, “Diffusion of Innovations”, London: Free Press, 2003.

[32] E.M. Rogers, A. Singhal, and M.M. Quinlan, “Diffusion of Innovations 1”, An Integr. Approach to Commun. Theory Res., vol. 23, pp. 415–434, 2019.

[33] J.W. Dearing and J.G. Cox, “Diffusion of innovations theory, principles, and practice”, Health Aff., vol. 37, pp. 183–190, 2018.

[34] Q. Ma and L. Liu, “The Technology Acceptance Model”, J. Organ. End User Comput., vol. 16, pp. 59–72, 2011.

[35] V. Venkatesh, M.W. Morris, G.B. Davis, and F.D. Davis, “User acceptance of information technology: Toward a unified view”, MIS Q., vol. 27, pp. 425–478, 2003.

[36] V. Venkatesh and F.D. Davis, “A theoretical extension of the technology acceptance model: Four longitudinal field studies”, Manage. Sci., vol. 46, pp. 186–204, 2000.

[37] Z.R. Marak, A. Tiwari, and S. Tiwari, “Adoption of 3D printing technology: an Innovation Diffusion Theory perspective” Int. J. Innov., vol. 7, pp. 87–103, 2019.

[38] R.L. Burritt, C. Herzig, S. Schaltegger, and T. Viere, “Diffusion of environmental management accounting for cleaner production: Evidence from some case studies”, J. Clean. Prod., vol. 224, pp. 479–491, 2019.

[39] M. Omidi, Q. Min, and A. Omidi, “Multi-level analysis framework for reviewing IDT-based studies”, Cogent Bus. Manag., vol. 4, pp. 2–12 2017.

[40] T.A. Wani, and S.W. Ali, “Innovation Diffusion Theory Review & Scope in the Study of Adoption of Smartphones in India”, J. Gen. Manag. Res., vol. 3, pp. 101–118, 2015.

[41] M. Guay, State of North Carolina JLOC on IT, Gartner 2008.

[42] M.E. Porter, “Technology and competitive advantage”, J. Bus. Strategy, vol. 5, p. 60, 1985.

[43] M.E Porter, “Competitive Strategy”, New York: The Free Press, 2008.

[44] M.E. Porter and M.R. Kramer, 2019. Creating shared value: how to reinvent capitalism and unleash a wave of innovation and growth, In: G.G. Lenssen anf N.C. Smith, (Eds.), “Managing Sustainable Business” Berlin: Springer Science Business, 2019, pp. 323–346.

[45] T. Arnold, “A pragmatic guide to real options”, New York: Springer, 2014.

[46] P. Vernimmen, P. Quiry, M. Dallochio, Y. Le Fur, and A. Salvi, “Corporate finance: Theory and practice” (3rd ed.), Hoboken, NJ: John Wiley and Sons, 2011.

[47] K. Berman, J. Knight, and J. Case, “Financial intelligence: A manager’s guide to knowing what the numbers really mean”, Boston, MA: Harvard Business Review Press, 2013.

[48] Trading Economics. “Thailand Government Bond 10Y” 2020 Sep 11, Available from https://tradingeconomics.com/thailand/government-bond-yield

Biographies

Chulalux Soprakan received 1st class honors in her B.Acc. degree in Accounting from Dhurakij Pundit University, Thailand in 1995. She also received MBA degree with 100% Scholarship in Accounting from Dhurakij Pundit University, Thailand in 2003. She has working experience over 24 years in IT management area as well as solid knowledge of accounting system program, business process and digital transformation. She is currently a Ph.D. student in Technology of Information System Management. Her areas of research interests include information technology management, robotic process automation, enterprise resource planning, digital transformation and business process improvement.

Supaporn Kiattisin received her B.Eng. degree in applied computer engi- neering from the Chiang Mai University, Chiang Mai, Thailand, in 1995, the M.Eng. degree in electrical engineering and the Ph.D. degree in electrical and computer engineering from the King Mongkut’s University of Technology Thonburi, Bangkok, Thailand, in 1998, and 2006, respectively. She is currently the program director of Technology of Information System Management Division, Faculty of Engineering, Mahidol University, Thailand. Her research interests include computer vision, image processing, robot vision, signal processing, pattern recognition, artificial intelligence, IoT, IT management, digital technologies, big data and enterprise architecture with TOGAF 9 certification. She is a member of the IEICE and TESA. She served as a Head of the IEEE Thailand Chapter in Biomedical Engineering. She also served as the Chairman of the TimesSOC Transaction Thailand. She has expertise in enterprise architecture (EA), data sciences, information technology in E-government and digital economy (DE).

Journal of Mobile Multimedia, Vol. 17_4, 749–772.

doi: 10.13052/jmm1550-4646.17413

© 2021 River Publishers