Active Infrastructure Sharing – A Key Enabler of Wireless Networks

Tilak Raj Dua

Director General, TAIPA, New Delhi, India

E-mail: tilakrajdua@gmail.com

Received 28 September 2020; Accepted 30 November 2020; Publication 26 January 2021

Abstract

Innovations and dynamic technological developments motivated the era of Information and Communications. We have witnessed revolution in communication and pattern as well as in the need of connecting world. Telecom industry is always been the core of digitization. Current pandemic situation has reflected new business and connectivity models and huge dependency on the telecom sector. The telecom network enables virtual work and meetings, education, financial transaction, e commerce, health, social meetings, webinars etc. Apart from the common usage for entertainment in terms of OTT, social media – the telecom network has become fundamental to contactless transactions – telemedicine, contactless courier delivery, online shopping etc. This paper presents an overview of telecom infrastructure model, concept of infrastructure sharing and its advantages. It also discusses various factors affecting infrastructure sharing.

Keywords: Telecom, infrastructure, sharing infrastructure, IoT, 5G.

1 Introduction

We are amid the greatest information and communications revolution in human history. The global telecommunication market is transforming towards a digital, sharing and interconnected economy. The transformations around the globe is driven by innovations and dynamic technological developments, which have been fuelled by omnipresent telecom networks and services.

The Covid-19 situation has led to huge surge in data consumption, with almost all the services and businesses – becoming dependent on telecom connectivity – due to possibility of various services on the broadband network. The telecom network enables virtual work and meetings, education, financial transaction, e commerce, health, social meetings, webinars etc. Apart from the common usage for entertainment in terms of OTT, social media – the telecom network has become fundamental to contactless transactions – telemedicine, contactless courier delivery, online shopping etc. The technology evolution to 5G would make possible a lot more services and applications – like remote surgery, contact less cars, IoT applications, Fixed Wireless broadband, drone technology besides enabling Industrial revolution 4.0. Going forward, the digitalisation has become a necessity and not a choice.

Telecom sector in India has witnessed a tremendous growth in the past decade with an exponential increase in the number of subscribers; India is the second largest telecom market in the world and is growing at a rapid pace.

Inclusion, access and opportunities presented by telecom services have expanded its reach to the poor and disadvantaged sections of society. In the coming years, the telecom services will contribute significantly towards inclusive development of the world economy.

1.1 Telecom Infrastructure Industry

Telecom tower industry is a distinct and important segment of the telecommunication sector. The telecom infrastructure is the prime enabler of expanding telecom services within countries.

Telecom infrastructure such as telecom towers, fibres, and cables play an important role in facilitating connectivity by the network operators to the subscribers.

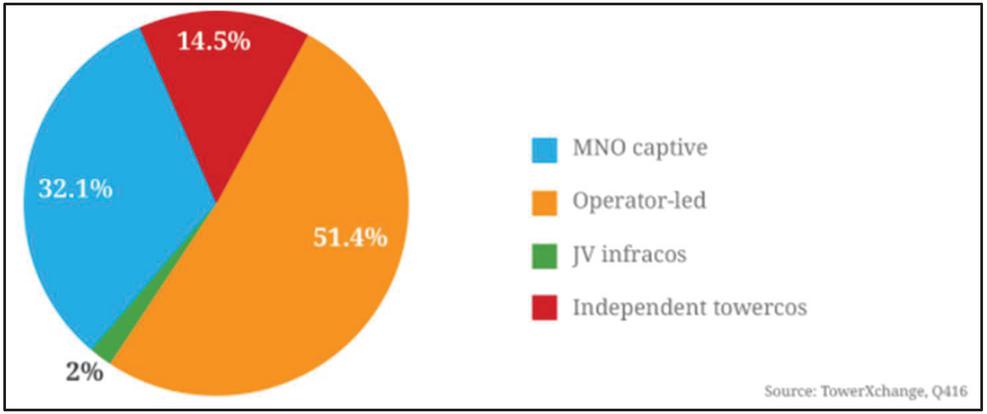

Globally, there are 4,082,452 telecom towers while Asian tower market comprises of 2,842,851 towers out of which 2,183,800 are owned or operated by tower-cos, representing 77% of the total count of Asia.

Figure 1 Ownership of towers globally.

Globally, the aggregate site count between FY 14-16 for the entire tower industry across the globe have grown at about 14.61% CAGR, driven by a combination of organic and inorganic growth. Further, according to TowerXchange, the telecom tower ‘asset class’ can be currently valued at USD 278.7 billion representing an important player/sector in the industry.

Further, Asia remains one of the fastest growing region for the telecom tower market and for expansion of the independent towerco business model. The transition towards sharing continues to gain momentum. Indonesian market continues to scale and mature; Protelindo’s acquisition of 2,500 towers from XL brings towerco penetration in this market to 64%, while Balitower and STP are driving the rollout of thousands of infill sites.

The regulatory environment for towercos and infrastructure sharing varies from mature tower markets such as India and Indonesia where the regulatory regime is well established, to regulatory environments still drafting policy like in Bangladesh, where independent towercos are developing new business model. In Asia, the tower count varies from 1.7 million for China, 4.5 lakh in India, to 6000 towers in Nepal.

There are several players in global tower market such as SEATH & Golden towers in Vietnam, China Tower Corporation in China, IBS towers in Indonesia, ATC, Bharti Infratel & Indus in India, Apollo towers in Myanmar among others.

In India, which is the currently the world’s second largest telecom market, telecom infrastructure is majorly installed and maintained by Infrastructure Providers who are registered with the Department of Telecommunications as Infrastructure Providers Category – I. IP-Is have installed close to 5 90 000 towers housing more than 22 lakh BTSs and enabling connectivity to more than 1.2 billion subscribers. The push towards 4G is driving the need for MNOs raise capital to fund spectrum and rollout critical telecom infrastructure

Telecom infrastructure is the backbone of the entire telecom sector and with the advent of new technologies such as Internet of Things, Machine to Machine Communication, Smart Cities, Fifth Generation technology, etc. it is going to play a vital role.

Presence of a robust telecom infrastructure, which is shareable, will lead to an expeditious roll out of the emerging technologies in the coming years.

2 Infrastructure Sharing & Its Benefits

Telecom, being a capital expenditure intensive business, needs huge investment year-on-year for growth and expansion. Sharing of infrastructure allows tower sites to host network equipment of multiple TSPs leading to capex and opex savings.

According to International Telecommunications Union (ITU), “the single biggest reason for Infrastructure sharing is to lower the cost of deploying ICT broadband network to achieve widespread and affordable access to broadband services”.

At present, the capital cost required for active infrastructure is around 60% while that of passive infrastructure is 40% of the overall capex. The costs will rise in the near future as the emerging economies expand their services into remote areas. Thus, sharing of infrastructure is inevitable to realize better margins.

Earlier a barter system used to exist wherein telecom towers were made available to individual telecom service providers leading to duplication of networks and high cost of rollout of services. However, the business model of passive infrastructure sharing is based on building, owning, operating and maintaining passive telecom infrastructure sites capable of hosting active network components of various technologies of multiple telecom operators. The model is time tested, proven, globally adopted and has been a trendsetter.

Over the years, infrastructure sharing have improved efficiencies and quality of services to the consumers at an affordable cost as the cost for provisioning the infrastructure could be shared amongst the operators.

Under this model, the telecom infrastructure is being shared with the operators on a non-discriminatory, transparent and in a cost- effective manner.

2.1 Sharing Concept in India

In India, the concept of “Tower Sharing” was initiated through Project “MOST” (Mobile Operators Shared Towers) by Union Ministry of Urban Affairs and Ministry of Communications, Government of India.

Under Project MOST, the telecom infrastructure is shared in an unbiased way with the telecom service providers; thereby maintaining competition and facilitating connectivity simultaneously. Sharing concept in India has led to optimal utilization of telecom infrastructure and has promoted a healthy competition.

Realizing the advantages of the sharing concept, Department of Telecommunications allowed the sharing of active telecom infrastructure like Antenna, Feeder Cable and Transmission System as well.

Sharing of infrastructure is pivotal to realize the country’s bold initiatives such as Digital India and Smart Cities Mission. It allows expeditious rollout of telecom networks and will accelerate transforming India into a Digital Economy.

The sharing concept has become a trendsetter and is being emulated world-over.

2.2 Advantages of Infrastructure Sharing

2.2.1 Reduced Capital Expenditure

Reduction in capital expenditure which down the entry barriers to new service providers in the market. This ultimately benefits the customers in the form of reduced prices and better quality of services.

‘Affordable Telephony’ enabled by the sharing concept is one of the key reasons for the rise of telecom services.

2.2.2 Reduced Operational Expenditure

As end to end services are offered, the day to day to expense for maintaining the telecom infrastructure is reduced for the telecom network operators. The cost savings can be used to increase reach, provide innovative services and improve customer satisfaction aiming towards a higher ARPUs.

2.2.3 Reduced Time – to – Market

By leveraging existing infrastructure, which is deployed in telecom circles, a new operator can significantly reduce its cost and time required to begin its operations.

2.2.4 Increased Connectivity

Telecom infrastructure have been installed in far-flung remote areas of the country. The areas have erratic power supply and are difficult to access. Sharing of infrastructure allows network operators to provide connectivity in these remote areas and allows them to expand their areas of operation.

2.2.5 Cost & Energy Efficiencies

Infrastructure sharing among multiple operators ultimately allows network providers to focus on efficient operations of their services and address customer concerns in a much better way. The outsourcing of power requirements and maintenance of infrastructure allows the network providers to save significant cost and manage energy efficiently.

2.3 Global Market Drivers for Sharing

Mobile data traffic is growing at an exponential pace and it grew 60% year on year between Q1 2015 and Q1 2016. By 2021, monthly mobile traffic is expected to exceed 50 Exabyte.

The world is witnessing a paradigm shift towards technologies like 5G, Internet of Things, Smart Cities and e-Governances/Services. Emergence of such technologies will transform the countries into a digital economy and demand rollout of additional telecom infrastructure.

3 Types of Infrastructure Sharing

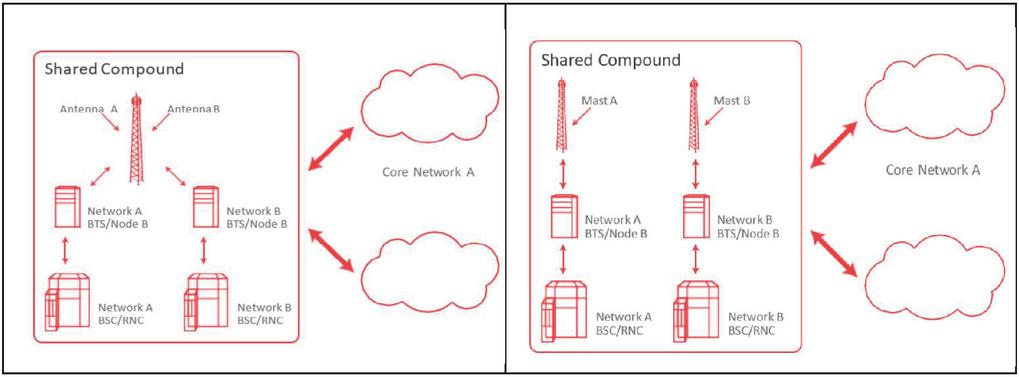

Network sharing may take many forms, ranging from passive sharing of cell sites and masts to sharing of radio access networks (RANs) and other active elements such as network roaming and the core.

Passive infrastructure sharing involves the following passive elements

• Shared towers for mobile networks (telecom tower)

• Shared ducts for fiber optic cables (duct)

• Shared use of fiber strands in FO cable (dark fibre)

• Shared access to buildings (right of way)

3.1 ITU Definition of Passive Infrastructure Sharing

Passive infrastructure sharing allows operators to share the non-electrical, civil engineering elements of telecommunication networks. This might include rights of way or easements, ducts, pylons, masts, trenches, towers, poles, equipment rooms and related power supplies, air conditioning, and security systems.

Active infrastructure sharing involves the following elements

• Radio Network Sharing

• Roaming,

• Wholesale Offers and Mvnos.

• Spectrum Sharing

Active infrastructure sharing involves sharing the active electronic network elements – the intelligence in the network – embodied in base stations and other equipment for mobile networks and access node switches and management systems for fibre networks. Sharing active infrastructure is a much more contested issue, as it goes to the heart of the value-producing elements of telecom business.

Network sharing may take many forms, ranging from passive sharing of cell sites and masts to sharing of radio access networks (RANs) and other active elements such as network roaming and the core. Telecom service providers or independent infrastructure providers/tower companies can execute further, active network elements sharing.

In telecom networks, the technology keeps on evolving continuously. Telecom service providers have not only to invest in spectrum, but also in new generation electronics, equipment’s to support next generation network. Spectrum is allotted through auction and therefore is a major capex for telecom operators. Sharing of active network elements, through independent infrastructure providers in addition to already prevalent passive sharing can significantly address the capex issue, besides reducing the capex and opex cost significantly. This will reduce the period to rollout the new technology and would provide a plug and play model to the telecom infrastructure provider.

3.2 Factors Influencing Infrastructure Sharing

Whilst technically it could be possible for operators to share any amount of equipment, implementation can be complex for some forms of sharing. This is particularly true where existing networks are being joined together as opposed to the rolling out of a new, single network. Considerations that must be addressed include the load-bearing capacity of towers, space within sites, tilt and height of the antenna and adverse effects on quality of service (QoS) when antennas are combined and differing standards employed by the equipment vendor. Therefore, site sharing, mast sharing and network roaming are the most common forms of infrastructure sharing due to their relative technical and commercial simplicity. RAN sharing is gaining commercial traction.

The strategic rationale for engaging in infrastructure sharing differs between new entrant and incumbent operators, 3G/4G/5G networks and mature and developing markets. The objectives differ based on type of market, technology evolution, emergence of independent infrastructure providers etc.

• MNOs in mature markets: Infrastructure sharing may reduce operating costs and provide additional capacity in congested areas where space for sites and towers is limited. It may also provide an additional source of revenue but may be limited by differing strategic objectives.

• MNOs in developing markets: Infrastructure sharing may expand coverage into previously un-served geographic areas. This is facilitated via national roaming or by reducing subscriber acquisition costs (SACs) by sharing sites and masts or the radio access network (RAN). Infrastructure sharing is also increasingly being used in congested urban centres where new site acquisition is difficult. However, it may be less likely to occur in markets where coverage is used as a service differentiator and, if mandated, could potentially reduce investment incentives for continued network roll-out.

• 4G /5G network operators: Operators are taking the opportunity to reduce capital and operational expenditure by sharing infrastructure from the start of the build-out. Sharing a new network removes the complexity and cost associated with replanning existing networks but requires commercial agreement on operations and upgrade costs.

• Third party infrastructure providers: Infrastructure funds are showing more interest in acquiring or establishing third party mast or radio network businesses.

4 Active Infrastructure Sharing: Regulator’s Outlook

Regulator’s interest in active infrastructure sharing is three-fold; it has efficiency, competition, and environmental aspects. The gains are listed below:

Table 1 Infrastructure sharing – cost savings

| Sharing Type | Savings in Capex | Savings in Opex |

| Passive infra. Sharing cost savings | 16% to 35% capex | 16% to 35% opex |

| Active infrastructure sharing | 33% to 35% Capex | 25% to 33% opex |

| (excluding spectrum) | ||

| Active infra sharing (including spectrum) | 33% to 45% Capex | 30% to 33% opex |

TRAI has recommended active infrastructure sharing in access network (excluding spectrum). Sharing of core network has not been recommended.

5 Evolution to 5G and Increasing Requirement of Active Infrastructure Sharing

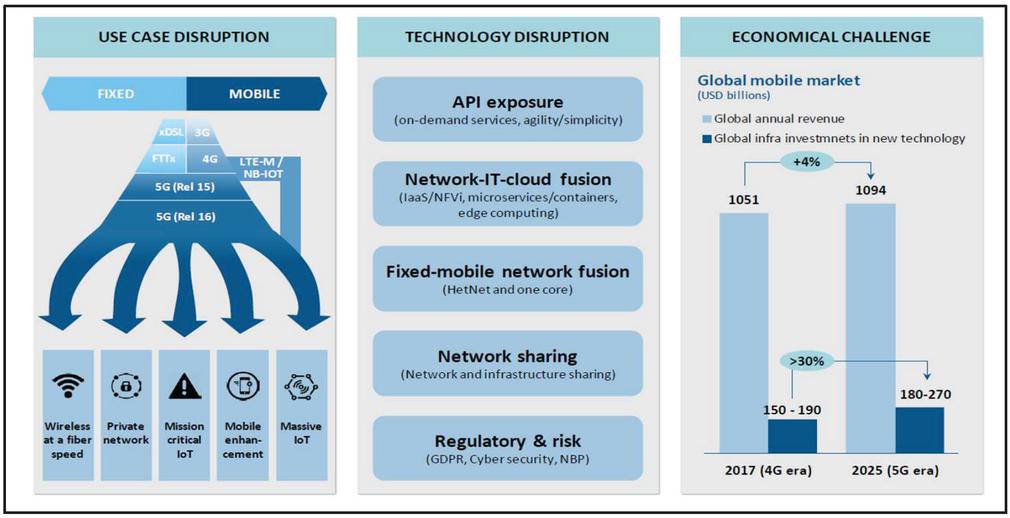

Technology evolution forces operators to transform their infrastructure and technology while placing significant pressure on financials. To compensate for market stagnation, operators must explore new areas of growth, such as fixed wireless access, deployment of 5G private networks and IoT. Some areas may seem risky at this stage, but competitive dynamics will likely encourage some operators to jump the gun.

These new use cases require a significant transformation and significant capex investments. Active infrastructure sharing by infrastructure providers/towers cos can bring in the much-needed investments into infrastructure while telecom service providers can focus on spectrum acquisition, services to customers, managing customer life cycle, customer complaints etc. Important areas that affect infrastructure are the convergence and densification of access network and edge computing. However, the key challenge will be securing shareholder returns.

The migration to high performing broadband-centric networks based on fibre, 4G/5G and new architecture has forced operators to rethink their infrastructure. Key aspects are:

• The trade-off between increasing site capacity through additional spectrum or densifying the network, which will necessitate the massive deployment of small cells. Verizon has tended to focus on densifying its network while T Mobile US has orientated towards a low-band spectrum strategy (in combination to a move to acquire Sprint and its medium band spectrum);

• Technology evolution to boost effective capacity per site, such as Carrier Aggregation, Massive MIMO and deployment of SON.

• Deployment of new NR radio technology on sites, increasing space occupancy in towers.

• Planning for edge computing, which initially requires data-centre capabilities at the edge of network and, in future, may expand to the site, opening the medium-term opportunity for edge carrier neutral data-centres.

New NR radio technology, small cells and edge computing all require additional capex and operational costs for operators. As such, operators are trying to improve investment and cost, which include optimization of footprint at site level.

Source: Tower Xchange: A Delta perspective

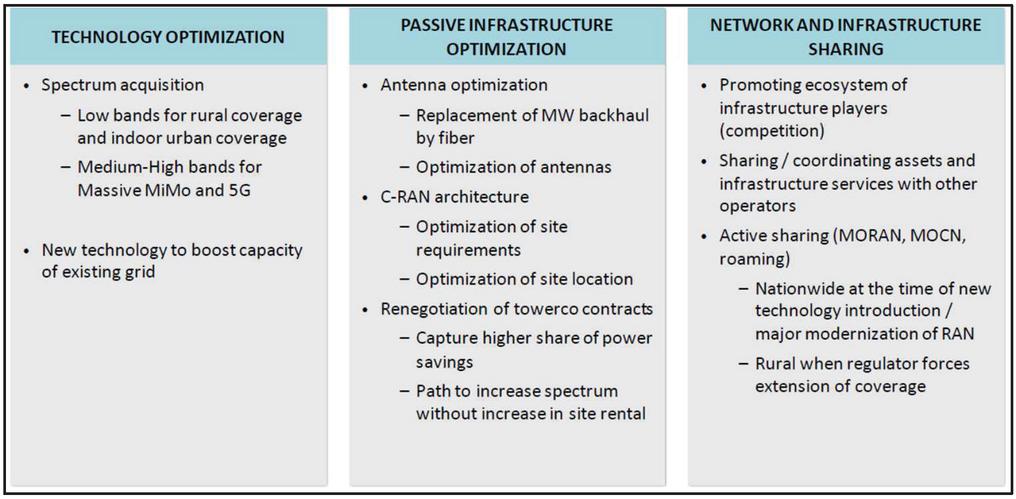

5.1 Main Drivers for Operator Infrastructure and Technology Cost Optimisation

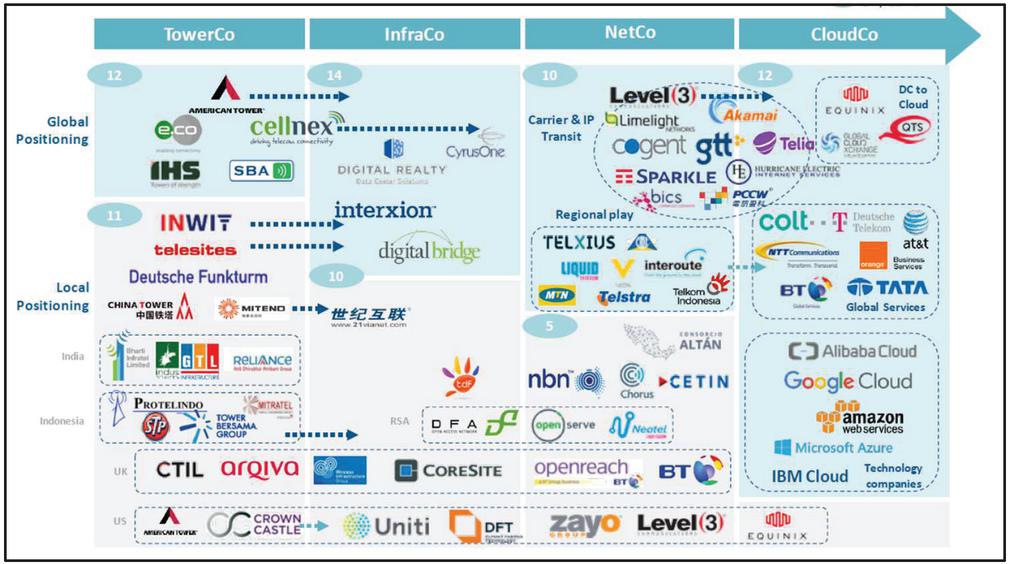

Technology evolution poses new requirements for infrastructure such as small cells, fiber-to-the-site, edge data centre. It also opens new opportunities for passive and active infrastructure sharing. Independent telecom infrastructure service providers/TowerCos may explore new business models such as small-cell-as-a-service or even the creation of rural/national NetCos – a similar model to Mexico’s carrier neutral Altan network.

The following diagram shows where some TowerCo have evolved into InfraCo. Some fiber-centric players (e.g. Uniti, Zayo) are exploring Towers and small cells. TowerCos have mainly explored ways to evolve their businesses by diversifying asset class (e.g. fiber and small cells) and migrating into services. The most common asset class diversification has been fibre rollout, while diversification into services has centred on DAS, power optimization and passive infrastructure optimization.

Source: Tower Xchange: A Delta perspective

India is expected to emerge a leading player in the virtual world and with government, enabling policies and regulations there is an accelerating move to shift towards 5G networks. 4G subscribers are forecasted to grow to 280 million by 2020.

As per analysts, total number of internet subscribers in India will cross 700 million by 2025. With the growing data consumption in the country, India will need 5G capability networks to meet the demand.

The deployment of 5G networks can be enabled only by installing a robust ICT ecosystem.

5.1.1 E – Services

Global economies are transforming themselves into a digital economy to facilitate better service delivery, transparency and accountability, empower people through information, improved efficiency and improved interaction among the business and the government.

Shift towards e-services will lead to ease of doing business, lead to better participation of citizens in policymaking, better implementation on policies on ground and faster clearance of business approvals.

5.1.2 Internet of Things

Internet of Things, popularly recognized as IOT, is an emerging disruptive technology of the 21st century. IoT allows exchange of information between real world devices and applications. It is estimated that about 50 billion devices would be connected by 2020. Further, accelerated penetration of smart city technologies will drive up demand for IoT devices to 1.6 billion by 2017, up from 39% from this year.

Telecom infrastructure will be the bedrock for successful implementation of technologies like IoT.

6 International Scenario – Active Infrastructure Sharing by Neutral Host

Some of Global Trends towards Active Sharing through a Neutral Host.

• New Zealand: New Zealand’s wholesale network operator, Chorus, is calling on the Government to begin formulating plans for a single 5G mobile network, which can be shared by all service providers, as it would not be sustainable for the country’s three mobile operators to roll out separate 5G networks due to the amount of investment needed.

• Denmark: In 2012, Telenor Denmark and Telia Denmark have signed a managed services contract with Nokia, which will manage their shared mobile networks run by a common infrastructure company TT-Netvaerket.

• USA: The use of independent wholesale infrastructure providers for the provision of small-cell networks has increased over the last few years. Wireless provider Crown Castle (USA), for example, increased its small-cell revenues by over 40% between 2015 and 2016 as mobile operators densify their networks ahead of 5G roll-out.

• Scotland: In September 2017, independent tower specialist Wireless Infrastructure Group, in collaboration with Telefónica, launched Europe’s first small-cell network supporting cloud RAN (C-RAN) for faster and higher capacity mobile services in the city centre of Aberdeen.

• Australia: The telcos in Australia have infrastructure sharing agreements with each other and with the main tower infrastructure providers. One of the main players within the active infrastructure sharing market is Broadcast Australia (BA). With a diverse portfolio of structures ranging from 30m to over 230m, it has the best regional and rural penetration among Australian tower companies. Servicing not just broadcasters, it provides infrastructure leasing and related services to the majority MNOs, NBN Co., as well as other telecommunications players.

7 Conclusions

Passive infrastructure sharing has emerged as a successful business model globally. The model has not only resulted in attracting investments to the telecom sector and reduction in capex/rollout costs but also resulted in considerable savings in operational expenditure for the telcos. The infrastructure sharing model has been made popular by independent tower cos who have developed expertise in quick rollout along with better management of energy functions. They have acted as neutral host to the competing telecom service providers, by sharing of passive infrastructure in a transparent, non-discriminatory, and efficient manner. Thus, world over, telecom service providers have aggressively hived off their passive assets into independent companies. In this process, not only the companies have become asset light and amassed funds for the network expansion / new technology rollouts, but also added economy and efficiency to the overall management and operations of the telecom sector. In this process, the telcos were able to concentrate on their core operations – i.e. marketing and customer care functions.

With the advent of technology, it is now possible to share the active elements of network as well, such as small cell, e node B, antenna etc. The active infrastructure sharing in addition to passive infrastructure sharing, presents an excellent opportunity of attracting investments to the sector and provide leverage to the telecom service providers to invest their resources in acquiring spectrum and monetising the new technology by developing customer/enterprise centric use cases and new applications. As the technology evolution is a regular phenomenon in the cellular mobile telecom services, the sharing of passive and active network infrastructure would become a role model for the overall sustainability of the telecom sector.

The wireless data consumption continues to surge at a phenomenal pace. In order to serve the ever-growing demand, the network resources would have to be added continually to add network capacity/invest into new technologies, which makes the telecom a highly capital-intensive business. The infrastructure sharing model can result into significant capex and opex savings, and result into enhanced viability of the telecom sector.

Biography

Tilak Raj Dua received his B.Sc. Engineering degree in Electronics from Punjab University, Chandigarh, India and Credential in Business Management and Export Management from Bhartiya Vidya Bhawan, Vadodara, India.

Mr. Dua is the recipient of “Evangelist Mobile Infrastructure Award” by Hon’ble Minister of Telecommunications, India. Mr. Dua has also completed specialisation courses such as Electromagnetic interference and Electromagnetic compatibility, Satellite communication, Microwave communication – Tropo scatter and Spectrum Management.

In Feb 2020, Mr. Dua was awarded “Amity National Leadership Award” For Industry Commitment Towards Green Technology.

Mr. Dua has Multidisciplinary understanding of the needs of the Telecom sector in the fields like Technology Selection, Technology Absorption, Technology Up gradation, Resolution of Regulatory issues, Telecom Licensing, Compatibility issues understanding between various technologies.

During his association with telecom sector, he has held very prestigious posts such as Deputy Director General, COAI, Director in Bharti Airtel Limited and Dy Director, Indian Air Force Limited.

Presently heading TAIPA as Director General, Mr. Dua is also associated with ITUAPT Foundation of India as co- chairman and with GISFI as its vice chairman.

His experience includes all facets of telecom be it Product Development, Business Development, Telecom Licensing, Regulatory issues, infrastructure sharing, Spectrum Related Issues, Efficient Utilization and Spectrum refarming etc. He has many first to his credit like finalization of joint ventures, technical collaboration, introduction of new product, launch of cellular services in India and finalization of license agreements/interconnect agreements.

Journal of Mobile Multimedia, Vol. 17_1-3, 141–156.

doi: 10.13052/jmm1550-4646.17137

© 2020 River Publishers