Exploring the Role of Behavioral Intention and Trust in Technology Adoption: A Meta-UTAUT Model Approach

Madhvendra Pratap Singh* and Mridulesh Singh

School of Business Management, Chhatrapati Shahu Ji Maharaj University, Kanpur, Uttar Pradesh, India

E-mail: madhvendra99@gmail.com; mriduleshsingh7@gmail.com

*Corresponding Author

Received 26 November 2024; Accepted 13 September 2025

Abstract

This paper discusses the adoption of the meta UTAUT model incorporating trust. The model consists of PE, EE, SI, FC, and trust as independent variables, attitude as a mediating variable, while BI and UB are the dependent variables. A sample size of 279 users drawn from urban and rural settings was conducted. The suggested model was experimented through structural equation modelling (SEM). The outcome of this study indicates that BI is positively affecting the UB and becoming the strongest predictor of it. Importantly, trust is also positively influencing BI and UB. FC and EE play vital roles in building the attitude of the user. EE, PE, and BI-even SI-found not so strong in predicting BI. BI as the strong predictor came in the finding so it can contribute in predicting the behaviour of the user. The study focused more on the role of trust and user experience.

Keywords: Behavioural intention, usage behaviour, trust, META-UTAUT, technology adoption, facilitating conditions, effort expectancy, social influence.

1 Introduction

Mobile payment systems have emerged as a solution to replace cash transactions in the digital financial landscape. They have successfully transformed how users conduct financial transactions across geographies. However, challenges persist at various levels in emerging economies, such as India.

The widespread influence of mobile device-based payment systems has surpassed all other innovations in human history, making them an integral part of contemporary society in the 21st century [41]. These developments have transformed the otherwise static processes of money transfer into digital versions accessible through mobile devices [41]. The technological advancements and a digitalized economy have propelled exponential growth in the mobile payment’s domain in India. This trend has been pivotal to the economic development process and facilitated financial inclusion, which has heretofore been unobtained for the poor strata of Indian society [10].

The paper looks forward to the rapid expansion and potential growth of the mobile payment wallet in the upcoming years. It is estimated that the compound annual growth rate (CAGR) of mobile payment wallets will reach 23.9% between 2023 and 2027. The adoption of such technologies, like mobile payment systems, is influenced by various factors [3]. The literature has looked at mobile phone usage from many different angles. For example, there is work on tracking travel patterns [27], studying digital financial services [20], and examining mobile commerce [25]. There is also considerable scholarly work on mobile learning and healthcare domains [4, 5, 23].

India, with its extensive population and the increasing penetration of smartphones, becomes an excellent test bed for investigating mobile payment adoption. The rapidly increasing mobile payment in developing countries makes this study relevant. With the introduction of mobile payments, it has now become easy to buy goods and services online by using Amazon or Flipkart websites, which helps in making a digital shopping process more efficient and satisfying [28, 35].

Much of the previous work on mobile payments in developing economies was focused on the technological, economic, and social factors influencing user behavior. The role of trust and behavioral intention in mobile payment systems is a gap in the literature that has not been explored much in emerging economies like India. Although trust is the most important element of technology adoption, its applicability in the model, like UTAUT, is relatively less in mobile payments. The proposed model intends to bridge this gap by further developing the META-UTAUT [11] model by integrating trust, providing further insight into factors that are driving behavioral intention towards mobile payment adoption in a developing country such as India [1]. This research contributes to filling that gap in the literature and advancing our understanding of digital financial inclusion in emerging markets.

This study addresses these knowledge deficiencies through three main objectives:

• To provide a detailed analysis of the technological adoption models currently in use and identify the underlying factors influencing Indian consumers’ behavior toward digital payment ecosystems.

• To study how trust impacts the growth of electronic payment practices [35].

• To validate the conceptual model designed for this study by gathering information from a relevant subset of Indian mobile payment users.

The results of this research are relevant for stakeholders in the mobile payments system, including the providers of payment systems, marketers, and policy makers.

2 Literature Review

The first to articulate the UTAUT framework was Venkatesh in 2003 to provide an adequate and more detailed model of explaining the technology adoption and usage process [43]. The META-UTAUT model developed by Dwivedi et al. in 2019 has also gained momentum on account of the complex and evolving characteristics of technology acceptance in emerging technological environments [11]. The META-UTAUT model upgrades the classical UTAUT model by bringing forth additional constructs, with emphasis placed on relevant applications in respective domains. In this study, we adapt and further extend the META-UTAUT model, and include Trust as another factor and then investigate its implications toward behavioral intention and usage behavior, all within mobile payment systems.

Performance expectancy (PE) – According to Venkatesh, PE is explained by the consumer’s expectation that technology will improve performance while performing any task [43]. According to the aforementioned assertion, PE is a crucial component for forecasting emerging technologies. Previous research has demonstrated the positive effects of physical education on motivating individuals to keep utilizing digital tools like the Internet [46]. PE is a reliable measure of how satisfied customers are with using digital payments [9, 25].

Effort expectancy (EE) – EE illustrates the ease of use of a technology and how it influences the desire to utilize it [43]. EE has a positive impact on users’ intentions to keep using mobile applications [12, 21]. Marinkovi´c confirmed that EE has a substantial impact on satisfaction with the continuation of using digital payments using a UTAUT-based model [25].

Social influence (SI) – SI is the degree to which people (such family, neighbours, and coworkers) encourage those who utilize a particular technology to do so [42]. SI, a prominent variable in UTAUT, has a considerable impact on users’ intentions to continue using digital apps [22].

Facilitating conditions (FC) – An individual needs both organizational and technological assistance in order to use technology effectively [43]. UTAUT initially thought that real usage behaviour was predicted by facilitating conditions. Perceived availability of resources, experience, and collaboration increases the potential for utilizing new technology. Facilitating circumstances reduce potential barriers to the adoption of technology. In India, the growing use of QR-based mobile payments has shown that certain supportive factors – like access to technology, financial assistance, and proper infrastructure – play a crucial role in shaping the willingness of street vendors from marginalized communities to start using mobile payment systems [29].

Trust – Trust has a significant role in determining usage patterns as well as behavioural goals. The idea of trust is crucial to mobile payment systems since users frequently have to give sensitive financial data to primary and tertiary systems. According to earlier studies, trust can enhance intentions for technology behaviour [36]. Although there are risks associated with mobile phones and they aren’t always safe, trust plays a significant role in how people use and are inclined to use them [46]. Customers are expected to provide both the first and third payment systems with sensitive financial information when making mobile payments [45]. In order to build behavioural intention, there must be an increase in trust.

Attitude (ATT) – A person’s attitude is exemplified by how positively or negatively they feel about a good or service. Online shopping, information systems and services [34] have all shown a substantial correlation between attitude and behaviour. Across a range of scenarios, including the use of e-wallets and mobile banking, attitude is a strong predictor of behavioural intention. Attitude had a direct impact on behavioural intentions in mobile banking, underscoring its significance in user acceptability [15]. A person’s attitude, whether favourable or unfavourable, can affect their choices and, eventually, their behaviour. Positive attitudes on mobile payment systems can therefore positively impact a user’s propensity to do a particular action.

Behavioural intentions to use mobile payment systems – A key component of the META UTAUT paradigm is the idea of BI, which measures a person’s motivation and inclination to engage in a particular behaviour [43]. Researchers believe that the range of personal reasons that influence a behaviour can be expressed through intention. Accordingly, the strength of an individual’s intentions is strongly correlated with the probability that they would execute the action that is the subject of those intentions. Numerous studies have demonstrated a strong correlation between BI and the actual adoption of electronic payments.

This study employs eight constructs – performance expectancy (PE), effort expectancy (EE), social influence (SI), facilitating conditions (FC), trust, attitude, behavioural intention (BI), and usage behaviour (UB) – adapted from the Unified Theory of Acceptance and Use of Technology (UTAUT) and its validated extensions. PE and EE assess expected performance benefits and ease of use, both of which are vital in evaluating mobile payment technologies [9, 43].

SI indicates how adoption is influenced by peers or important others, while FC reflects the infrastructure and technical support available, both of which are especially relevant in emerging economy contexts [25, 43]. Trust is added as an independent variable to address concerns over security and reliability, which are commonly cited barriers in mobile finance adoption [39, 46].

Attitude is included as a mediating construct that reflects users’ affective responses toward the technology, influencing their willingness to adopt [2, 32]. BI and UB remain foundational elements, capturing the intention to adopt and actual usage behaviour, as defined in the original model [43]. Together, these variables provide a comprehensive framework to analyse mobile payment adoption behaviour, particularly in the context of developing countries.

H1: ATT and BI are positively related.

H2: The Impact of BI on UB is positive.

H3: EE positively affects ATT.

H4: EE has a favourable impact on BI

H5: FC has a positive impact on ATT

H6: FC is positively related to BI.

H7: PE is positively related to ATT

H8: PE is positively related to BI.

H9: SI positively impacts ATT.

H10: SI will positively influence BI.

H11: Trust shall have a positive impact on BI.

H12: UB will be influenced positively.

3 Research Methodology

3.1 Research Design

The methodology of this study is based on enumerative tools and techniques to cross-check the intention to use mobile payment systems (MPS) among users in Uttar Pradesh. This research design facilitates the collection of empirical data, and the application of appropriate statistical tools helps in exploring the associations between independent, mediating, and outcome variables. The design ensures a systematic approach to understanding user behaviour and identifying the key determinants influencing mobile payment adoption.

3.2 Research Model

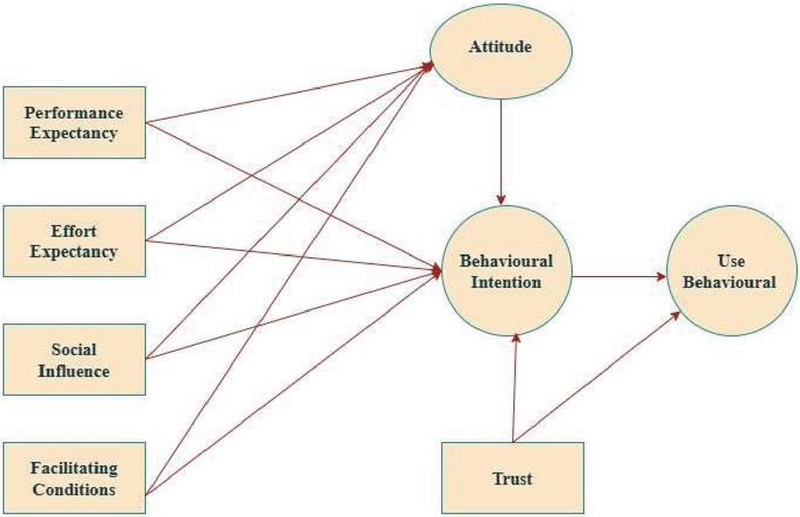

The research model for this study is grounded in the meta-UTAUT framework, originally proposed by Yogesh Dwivedi et al. [11]. The model includes Performance Expectancy (PE), Effort Expectancy (EE), Social Influence (SI), Facilitating Conditions (FC), and Trust as the independent variables, Attitude as the mediating variable, and Behavioural Intention (BI) and Usage Behaviour (UB) as the outcome variables. The study aims to assess the impact of these variables on individuals’ intentions to adopt and continue using mobile payment services.

The proposed research model builds upon the Unified Theory of Acceptance and Use of Technology (UTAUT), developed by Venkatesh et al. [43], which explains technology acceptance behaviour across diverse information systems. In this study, the model has been refined and contextualized for mobile payment adoption in India by integrating two additional constructs – Trust and Attitude – as suggested in the meta-UTAUT model by Dwivedi et al. [11]. This enhancement strengthens the framework by capturing psychological and behavioural aspects that are particularly crucial in understanding digital payment adoption among Indian consumers.

While the four foundational constructs of UTAUT – performance expectancy (PE), effort expectancy (EE), social influence (SI), and facilitating conditions (FC) – remain unchanged, this study integrates trust as an independent predictor and attitude as a mediating variable between the initial determinants and behavioural intention. Trust has become increasingly important in the domain of mobile payments, where users face elevated concerns regarding data security, privacy, and financial risk [39, 46]. Attitude, on the other hand, has been shown to reinforce behavioural intention when users evaluate mobile technologies based on personal relevance and ease of use [2, 32].

Figure 1 Presents the conceptual framework based on the meta-UTAUT model adopted from [11], incorporating trust and attitude

These model refinements support the specific aims of this research by addressing both technological and psychological dimensions of mobile payment adoption. Furthermore, the original structure of UTAUT remains intact, ensuring consistency with prior empirical findings while enhancing the model’s explanatory power through context-driven additions grounded in theory. The revised conceptual model reflecting these extensions is presented in Figure 1 and is discussed in detail in the methodology section.

3.3 Sampling

The process of data gathering made use of a structured questionnaire, and this was distributed over various cities in Uttar Pradesh, India. Virtual and physical methods were both used; however, most of the responses were gathered from virtual methods. 279 participants were sampled. Diligence was taken to make the data diverse in order to enhance the process’s standardization.

| Demographic | Percentage | Number of | |

| Characteristic | Category | (%) | Respondents |

| Age Distribution | 18–25 years | 20% | 56 |

| 26–35 years | 25% | 70 | |

| 36–45 years | 30% | 84 | |

| 46–60 years | 15% | 42 | |

| 60+ years | 10% | 28 | |

| Gender Distribution | Male | 55% | 153 |

| Female | 45% | 126 | |

| Occupation | Salaried Employee | 30% | 84 |

| Business Owner/Entrepreneur | 20% | 56 | |

| Self-employed/Freelancer | 15% | 42 | |

| Student | 20% | 56 | |

| Homemaker | 15% | 41 | |

| Educational Background | No formal education | 5% | 14 |

| Primary education | 10% | 28 | |

| Secondary education | 30% | 84 | |

| Graduate | 40% | 112 | |

| Postgraduate | 15% | 41 | |

| Income Distribution | Less than ₹20,000 | 25% | 70 |

| (Monthly) | ₹20,000 – ₹40,000 | 30% | 84 |

| ₹40,000 – ₹60,000 | 20% | 56 | |

| More than ₹60,000 | 25% | 69 | |

| Payment Adoption | Adopted Digital Payments | 80% | 223 |

| Did Not Adopt Digital Payments | 20% | 56 |

To ensure the representativeness and applicability of the findings, this study intentionally included respondents from a range of age groups, occupations, and income levels. This demographic diversity aligns with the objective of understanding mobile payment adoption determinants across different user segments. Research demonstrates that younger individuals are more likely to adopt mobile payment systems, while older participants often express more caution and require greater trust or familiarity with digital tools [40]. Occupation and income also play critical roles: individuals employed full-time or those with higher incomes tend to adopt mobile payments more frequently, whereas lower-income or varying occupational groups may face distinct barriers, such as limited access or reduced necessity [17, 44]. Incorporating these demographic variables reveals segment-specific behaviours and strengthens the external validity of the study, thereby offering practical insights for both policymakers and industry stakeholders.

3.4 Data Collection Instrument

The survey was based on an extensive conceptual model and includes several unique variables. Responses from participants were collected in a Likert scale format, and the test item of each survey was pilot-tested. Several statistical methods like Cronbach’s alpha, Average Variance Extracted (AVE), Composite Reliability, rho_A, and Heterotrait-Monotrait ratio were used to check consistency and validity of the variables measured [13, 16]. A baseline value of 0.7 to 0.9 for Cronbach’s alpha is considered acceptable.

Furthermore, all calculated AVE values were higher than 0.5, showing convergent validity, whereas the offered Heterotrait-Monotrait ratio values were below the limit of the acceptable value and hence guaranteed discriminant validity, and this is represented in Table 3 as well [13, 37].

Table 2 Reliability & validity

| Cronbach’s | Composite | Composite | Average Variance | |

| Alpha | Reliability (rho_a) | Reliability (rho_c) | Extracted (AVE) | |

| ATT | 0.904 | 0.906 | 0.929 | 0.723 |

| BI | 0.855 | 0.856 | 0.912 | 0.776 |

| EE | 0.891 | 0.892 | 0.925 | 0.755 |

| FC | 0.887 | 0.888 | 0.922 | 0.747 |

| PER | 0.877 | 0.881 | 0.924 | 0.802 |

| SI | 0.858 | 0.859 | 0.914 | 0.779 |

| TRUST | 0.827 | 0.831 | 0.896 | 0.743 |

| UB | 0.849 | 0.853 | 0.908 | 0.767 |

| Source: Author calculated values through SmartPLS 4. | ||||

| ATT | BI | EE | FC | PER | SI | TRUST | UB | |

| ATT | 0.85 | |||||||

| BI | 0.691 | 0.881 | ||||||

| EE | 0.651 | 0.68 | 0.869 | |||||

| FC | 0.651 | 0.705 | 0.643 | 0.864 | ||||

| PER | 0.667 | 0.71 | 0.729 | 0.672 | 0.896 | |||

| SI | 0.67 | 0.71 | 0.727 | 0.701 | 0.798 | 0.883 | ||

| TRUST | 0.659 | 0.763 | 0.639 | 0.637 | 0.683 | 0.677 | 0.862 | |

| UB | 0.725 | 0.771 | 0.752 | 0.707 | 0.788 | 0.777 | 0.721 | 0.876 |

| Source: Author calculated values through SmartPLS 4. | ||||||||

3.5 Data Collection Procedure

The data collection procedure involved administering the questionnaire to the selected respondents through face-to-face interviews. Trained interviewers conducted the interviews and explained the purpose of the study to the participants. The confidentiality and anonymity of the respondents were ensured, and their informed consent was obtained prior to data collection. The interviews were conducted from March to May 2024.

4 Results

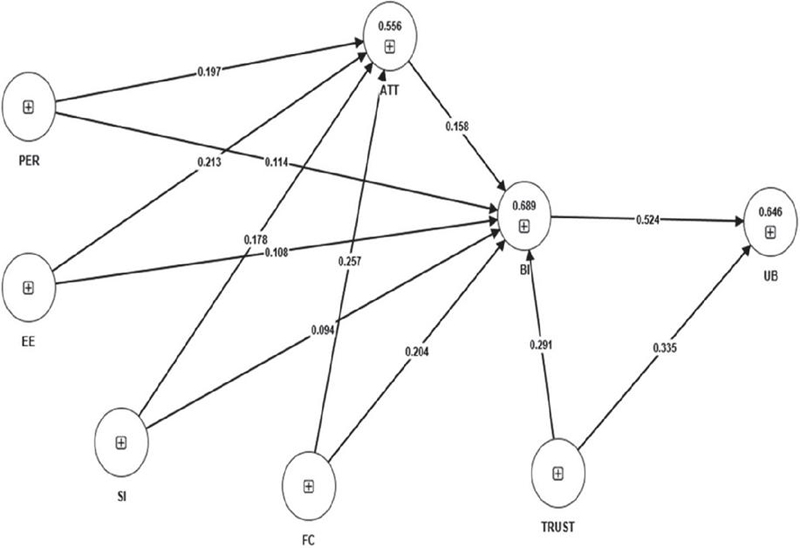

The data analysis was done on Smart PLS SEM-4 and it shows that the framework is quite fitted. The outcome of structural model analysis shows that positive relation among the variables. The main variable Trust shows the favourable response to behavioural intentions and uses behaviour; in it the standardized coefficient is 0.291and 0.335 respectively with statistical significance validation. The statistical examination shown that attitude has significant relationship with BI, where standardized coefficient is 0.158. In a similar way BI has favourable impact on UB with standardized coefficient 0.524.

The variable facilitating condition (FC) exhibits a significant positive effect on both attitude and behavioural intention, with standardized coefficients of 0.257 and 0.204, respectively. Conversely, although performance expectancy (PE) and social influence (SI) show positive relationships with attitude, their effects on behavioural intention are not statistically significant, having coefficients of 0.114 and 0.094. (see Table 4 and Figure 2)

| Original | Standard | |||

| Sample | Deviation | T Statistics | ||

| (O) | (STDEV) | (O/STDEV) | P Values | |

| ATT -> BI | 0.158 | 0.057 | 2.794 | 0.005 |

| BI -> UB | 0.524 | 0.072 | 7.243 | 0 |

| EE -> ATT | 0.213 | 0.08 | 2.672 | 0.008 |

| EE -> BI | 0.108 | 0.066 | 1.638 | 0.102 |

| FC -> ATT | 0.257 | 0.062 | 4.117 | 0 |

| FC -> BI | 0.204 | 0.055 | 3.677 | 0 |

| PER -> ATT | 0.197 | 0.089 | 2.214 | 0.027 |

| PER -> BI | 0.114 | 0.067 | 1.699 | 0.089 |

| SI -> ATT | 0.178 | 0.081 | 2.209 | 0.027 |

| SI -> BI | 0.094 | 0.07 | 1.34 | 0.18 |

| TRUST -> BI | 0.291 | 0.068 | 4.274 | 0 |

| TRUST -> UB | 0.335 | 0.071 | 4.726 | 0 |

| Source: Author calculated values through SmartPLS 4. |

Figure 2 Author generated model.

5 Discussion and Conclusion

5.1 Discussion

The findings of this study provide significant insights into the relationships among the various elements affecting user behavior and intentions. One of the hypotheses with the strongest evidence is H2, which asserts that BI does, in fact, have a positive impact on UB. With a p of 0 and a very high t-score of 7.243, UB is seriously reliant on it in order for actual usage to be feasible. It proves that people are very likely to follow through on their intentions.

Others are H11 and H12, which aim to facilitate TRUST’s involvement in UB and BI, respectively.

The strong positive association found between TRUST and BI (t-statistic 4.274, p-value 0) as well as between TRUST and UB (t-statistic 4.726, p-value 0) highlights the significant factor of trust in enhancing intention to use and actual usage of a service or good. This result is supported by previous research in which trust was cited to be one of the main issues that affect behavioural outcomes based on various scenarios. The research further ascertains the existence of a significant relationship between FC and both ATT and BI, as explained by hypotheses H5 and H6. This would mean that when the individual recognizes the availability of resources and support, he or she would be likely to have positive attitudes and a stronger intent to engage in the behaviour.

Another important finding is the favourable impact of EE on ATT (H3), which implies that users have more positive opinions of a system if they find it easy to use.

All theories, though, were not validated. As an illustration, H4 and H8, which claimed that EE would improve BI while PE would do the same, were not substantiated. The intention to utilize in this situation may therefore be unaffected by performance expectations and convenience of use. It is equally accurate to say that SI had no effect on BI (H10) as, in this situation, societal pressure was not realized as a significant motivator of behavioural intention.

In summary, the findings show that behavioural intention has a major role in predicting actual usage behaviour, although trust and facilitating conditions likewise had a substantial impact. Several assumptions were not supported, which raises the possibility that context dependence exists in the relationship. This merely implies that further research is necessary to examine all of these connections in various situations. The relationship between these results and earlier studies is then established, and the theoretical and practical ramifications of the findings are then examined.

The findings of this study shed important light on the connections between several elements affecting user behaviour and intentions. H2, which suggests that BI has a beneficial impact on Usage Behaviour (UB), receives the strongest evidence. With a p-value of 0 and a very high t-statistic of 7.243, this research emphasizes how important BI is in influencing actual usage behaviour. It implies that people are quite likely to carry out their intentions when they set out to do something.

6 Theoretical Implications

It adds depth to the body of literature by demonstrating the crucial role that behavioural intention (BI) plays as the most accurate interpreter of definite usage behaviour (UB). This strengthens the validity of models that depend on intention as a key behaviour precursor. Theoretically, trust is a crucial element of technology adoption and usage patterns, as demonstrated by the significant impact it has on both BI and UB. Additionally, the results indicate that FC has a considerable impact on ATT and BI, confirming the idea that resources and outside assistance play a crucial role in influencing user attitudes and intentions.

Remarkably, the work challenges some of the old hypotheses, claiming that EE and PE do not directly affect BI in this situation, and even hinting that their impact might be even more dependent on context than previously thought.

In addition to its limited impact on business intelligence, social influence’s widespread usage as a predictor in contested technology adoption models raises the possibility that social aspects do not always influence user intentions. These revelations make it possible to update current models and direct future studies that examine these connections in various settings.

7 Practical Implication

Since users’ behavioural intentions are the best indicator of their actual usage behaviour, it will be practically significant to improve them. Perhaps targeted marketing campaigns and user education initiatives can accomplish this. Because user behavioural intentions are the best indicator of actual usage behaviour, practical results suggest that enterprises should concentrate more on developing these intentions. For this reason, tailored experiences that are in line with user demands, user education initiatives, and strategic marketing could all be employed. Establishing trust is crucial since it has been shown to affect both BI and actual usage patterns. This goal will entail guarantees of data security, transparency, and dependable services. A more favourable attitude and intent in the direction of the adoption of a new technology will result from improving FC, which is the availability of all resources and assistance required for its implementation. Because user-friendliness results in higher adoption rates and more favourable opinions, the user experience is another important consideration. Finally, as SI had little effect on BI, there might be more internal motivators to encourage user participation rather than as many social pressure drivers. Although it primarily drives usage behaviour, establishing trust over the innovation is equally important because it has a significant impact on BI. Transparency, data security, and service dependence will be crucial in this situation. Facilitation conditions, such as the availability of resources and assistance, would improve intentions and attitudes. Higher adoption rates and more positive sentiments are likely to result from a simplified user experience. Lastly, because SI has limited impact on BI, firms may rely more on internal reasons to encourage user engagement than on social pressure.

8 Limitations

Although the current study offers valuable information, it has certain drawbacks. The research’s conclusions are restricted to a particular setting and might not apply to different sectors or user demographics. The findings may not be as broadly applicable as they could be due to the small sample size and certain demographic characteristics. The last drawback is that it depended on self-reported information, which may be biased in terms of response accuracy or social desirability. Third, several of the relationships, such as EE and SI, were very weak, suggesting that BI may be influenced by many unmeasured factors in various circumstances. Lastly, because the cross-sectional research approach only records a single moment in time, it is challenging to evaluate how user behaviour or attitude has changed over time. Deeper understanding of the evolution of these interactions would be better obtained by longitudinal research.

9 Future Research

Researchers hoping to build on this work with mobile payment systems have several promising paths to consider. For starters, a single survey snapshot can only say so much – tracking people’s habits over time would likely shed light on how intentions around digital payments actually play out day-to-day. It’s also worth asking whether trust and social pressure look different from one country to another. Would trust be such a big deal in places where technology is already part of daily life, or where consumer rights are well protected? [30, 39]. Besides, factors like how comfortable someone feels with technology, their attitude toward change, or how risky they believe digital payments to be could all have a real impact, especially among older folks or those outside major cities [32]. Finally, not everything can be captured in numbers – sometimes, talking to people directly or mixing in their stories offers a richer, more honest glimpse into what really helps or hinders them [2].

References

[1] Al-Saedi, K., and Al-Emran, M. (2021). A Systematic Review of Mobile Payment Studies from the Lens of the UTAUT Model. Studies in Systems, Decision and Control, 79–106. https://doi.org/10.1007/978-3-030-64987-6\_6.

[2] Arfi, W. B., Nasr, I. B., Kondrateva, G., and Hikkerova, L. (2021). The role of trust in intention to use the IoT in eHealth: Application of the modified UTAUT in a consumer context. Technological Forecasting and Social Change, 167, 120688. https://doi.org/10.1016/j.techfore.2021.120688.

[3] Alalwan, A. A., Dwivedi, Y. K., and Williams, M. D. (2016). Customers’ intention and adoption of telebanking in Jordan. Information Systems Management, 33(2), 154–178. https://doi.org/10.1080/10580530.2016.1155950.

[4] Arfi, W. B., Nasr, I. B., Kondrateva, G., and Hikkerova, L. (2021). The role of trust in intention to use the IoT in eHealth: Application of the modified UTAUT in a consumer context. *Technological Forecasting and Social Change, 167, 120688. https://doi.org/10.1016/j.techfore.2021.120688.

[5] Alghazi, S. S., Kamsin, A., Almaiah, M. A., Wong, S. Y., and Shuib, L. (2021b). For Sustainable Application of Mobile Learning: An Extended UTAUT model to examine the effect of technical factors on the usage of mobile devices as a learning tool. Sustainability, 13(4), 1856. https://doi.org/10.3390/su13041856.

[6] Arfi, W. B., Nasr, I. B., Kondrateva, G., and Hikkerova, L. (2021). The role of trust in intention to use the IoT in eHealth: Application of the modified UTAUT in a consumer context. Technological Forecasting and Social Change, 167, 120688. https://doi.org/10.1016/j.techfore.2021.120688.

[7] Aziz, S. A., and Idris, K. M. (2016). The impact of incentive alignment in behavioral acceptance. International Journal of Economics and Financial Issues, 6(4), 78–84. https://econjournals.com/index.php/ijefi/article/view/2693/pdf.

[8] Carter, L., Christian Shaupp, L., Hobbs, J., and Campbell, R. (2011). The role of security and trust in the adoption of online tax filing. Transforming Government: People, Process and Policy, 5(4), 303–318. https://doi.org/10.1108/17506161111173568.

[9] Chong, A. Y. L. (2013). Understanding mobile commerce continuance intentions: An empirical analysis of Chinese consumers. Journal of Computer Information Systems, 53(4), 22–30. https://doi.org/10.1080/08874417.2013.11645647.

[10] Demombynes, G., and Thegeya, A. (2012). Kenya’s mobile revolution and the promise of mobile savings. World Bank Policy Research Working Paper No. 5988. The World Bank, Washington, DC.

[11] Dwivedi, Y. K., Rana, N. P., Jeyaraj, A., Clement, M., and Williams, M. D. (2017b). Re-examining the Unified Theory of Acceptance and Use of Technology (UTAUT): towards a revised theoretical model. Information Systems Frontiers, 21(3), 719–734. https://doi.org/10.1007/s10796-017-9774-y.

[12] Fang, I. C., and Fang, S. C. (2016). Factors affecting consumer stickiness to continue using mobile applications. International Journal of Mobile Communications, 14(5), 431. https://doi.org/10.1504/ijmc.2016.078720.

[13] Hair, J. F., Hult, G. T. M., Ringle, C. M., and Sarstedt, M. (2017). A primer on partial least squares structural equation modeling (PLS-SEM) (2nd ed.). Sage Publications.

[14] Hair, J. F., Risher, J. J., Sarstedt, M., and Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24. https://doi.org/10.1108/ebr-11-2018-0203.

[15] Handayani, W. P. P. (2023b). The UTAUT implementation model in defining the behavioral intention of mobile banking users. Jurnal Manajemen Bisnis, 14(2), 361–377. https://doi.org/10.18196/mb.v14i2.18649.

[16] Henseler, J., Ringle, C. M., and Sarstedt, M. (2014). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/s11747-014-0403-8.

[17] He, Q., Ma, W., Vatsa, P., and Zheng, H. (2024). Impact of mobile payment adoption on household expenditures and subjective well-being. Review of Development Economics, 28(2), 932–950. https://doi.org/10.1111/rode.13054.

[18] Hermanto, A. H., Windasari, N. A., and Purwanegara, M. S. (2022). Taxpayers’ adoption of online tax return reporting: Extended meta-UTAUT model perspective. Cogent Business & Management, 9(1), 2110724. https://doi.org/10.1080/23311975.2022.2110724.

[19] Hassaan, M., and Yaseen, A. (2024). Factors influencing customers’ adoption of mobile payment in Pakistan: application of the extended meta-UTAUT model. Journal of Science & Technology Policy Management. https://doi.org/10.1108/jstpm-01-2024-0029.

[20] Jadil, Y., Rana, N. P., and Dwivedi, Y. K. (2021). A meta-analysis of the UTAUT model in the mobile banking literature: The moderating role of sample size and culture. Journal of Business Research, 132, 354–372. https://doi.org/10.1016/j.jbusres.2021.04.052.

[21] Kang, S. (2014). Factors influencing intention of mobile application use. International Journal of Mobile Communications, 12(4), 360. https://doi.org/10.1504/ijmc.2014.063653.

[22] Lai, I. K. W., and Shi, G. (2015). The impact of privacy concerns on the intention for continued use of an integrated mobile instant messaging and social network platform. International Journal of Mobile Communications, 13(6), 641. https://doi.org/10.1504/ijmc.2015.072086.

[23] Loh, X. K., Lee, V. H., Loh, X. M., Tan, G. W. H., Ooi, K. B., and Dwivedi, Y. K. (2021). The dark side of mobile learning via social media: How bad can it get? Information Systems Frontiers, 1–18. https://doi.org/10.1007/s10796-021-10202-z.

[24] Lady, Lady, Lie, K., Hesniati, H., and Candy, C. (2024). From Innovation and Compatibility to The Intention to Adopt Mobile Payment with User Expectations as The Mediating Factor. Almana, 8(3), 470–484. https://doi.org/10.36555/almana.v8i3.2667.

[25] Marinković, V., Đorđević, A., and Kalinić, Z. (2020). The moderating effects of gender on customer satisfaction and continuance intention in mobile commerce: A UTAUT-based perspective. Technology Analysis & Strategic Management, 32(3), 306–318. https://doi.org/10.1080/09537325.2019.1655537.

[26] Mas’ud, A., and Umar, M. A. (2019). Structural effects of trust in e-filing software on e-filing acceptance in services sector. International Journal of Enterprise Information Systems, 15(2), 76–94. https://doi.org/10.4018/IJEIS.2019040105.

[27] Medeiros, M., Ozturk, A., Hancer, M., Weinland, J., and Okumus, B. (2022). Understanding travel tracking mobile application usage: An integration of self determination theory and UTAUT2. Tourism Management Perspectives, 42, 100949. https://doi.org/10.1016/j.tmp.2022.100949.

[28] Mukherjee, M., and Roy, S. (2017). E-Commerce and online payment in the modern era. International Journal of Advanced Research in Computer Science and Software Engineering, 7(5), 1–5. https://doi.org/10.23956/ijarcsse/sv7i5/0250.

[29] Nandru, R., Kumar, B., and Chendragiri, R. (2024). Adoption intention of mobile QR code payment system among marginalized street vendors: An empirical investigation from an emerging economy. Journal of Science and Technology Policy Management, ahead-of-print. https://doi.org/10.1108/jstpm-11-2024-246.

[30] Oliveira, T., Thomas, M., Baptista, G., and Campos, F. (2016). Mobile payment: Understanding the determinants of customer adoption and intention to recommend the technology. Computers in Human Behavior, 61, 404–414. https://doi.org/10.1016/j.chb.2016.03.030.

[31] Pérez-Morote, R., Pontones-Rosa, C., and Núñez-Chicharro, M. (2020). The effects of e-government evaluation, trust and the digital divide in the levels of e-government use in European countries. Technological Forecasting and Social Change, 154, 119973. https://doi.org/10.1016/j.techfore.2020.119973.

[32] Patil, P., Tamilmani, K., Rana, N. P., and Raghavan, V. (2020). Understanding consumer adoption of mobile payment in India: Extending meta-UTAUT model with personal innovativeness, anxiety, trust, and grievance redressal. International Journal of Information Management, 54, 102144. https://doi.org/10.1016/j.ijinfomgt.2020.102144.

[33] R, A., Kuanr, A., and Kr, S. (2021b). Developing banking intelligence in emerging markets: Systematic review and agenda. International Journal of Information Management Data Insights, 1(2), 100026. https://doi.org/10.1016/j.jjimei.2021.100026.

[34] Rahman, T., Noh, M., Kim, Y. S., and Lee, C. K. (2021b). Effect of word of mouth on m-payment service adoption: a developing country case study. Information Development, 38(2), 268–285. https://doi.org/10.1177/0266666921999702.

[35] Rastogi, S., Panse, C., Sharma, A., and Bhimavarapu, V. M. (2021b). Unified Payment Interface (UPI): a digital innovation and its impact on financial inclusion and economic development. Universal Journal of Accounting and Finance, 9(3), 518–530. https://doi.org/10.13189/ujaf.2021.090326.

[36] Sarkar, S., Chauhan, S., and Khare, A. (2020). A meta-analysis of antecedents and consequences of trust in mobile commerce. International Journal of Information Management, 50, 286–301. https://doi.org/10.1016/j.ijinfomgt.2019.08.008.

[37] Sarstedt, M., Ringle, C. M., Cheah, J. H., Ting, H., Moisescu, O. I., and Radomir, L. (2020). Structural model robustness checks in PLS-SEM. Tourism Economics, 26(4), 531–554. https://doi.org/10.1177/1354816618823921.

[38] Singh, S., and Srivastava, R. (2018b). Predicting the intention to use mobile banking in India. International Journal of Bank Marketing, 36(2), 357–378. https://doi.org/10.1108/ijbm-12-2016-0186.

[39] Slade, E. L., Williams, M. D., Dwivedi, Y. K., and Piercy, N. C. (2015). Exploring consumer adoption of proximity mobile payments. Journal of Strategic Marketing, 23(3), 209–232. https://doi.org/10.1080/0965254X.2013.840347.

[40] Song, K., Wu, P., and Zou, S. (2023). The adoption and use of mobile payment: Determinants and relationship with bank access. China Economic Review, 77, Article 101893. https://doi.org/10.1016/j.chieco.2022.101893.

[41] Thakur, R., and Srivastava, M. (2014b). Adoption readiness, personal innovativeness, perceived risk and usage intention across customer groups for mobile payment services in India. Internet Research, 24(3), 369–392. https://doi.org/10.1108/intr-12-2012-0244.

[42] Thusi, P., and Maduku, D. K. (2020b). South African millennials’ acceptance and use of retail mobile banking apps: An integrated perspective. Computers in Human Behavior, 111, 106405. https://doi.org/10.1016/j.chb.2020.106405.

[43] Venkatesh, N., Morris, N., Davis, N., and Davis, N. (2003). User acceptance of information Technology: toward a unified view. MIS Quarterly, 27(3), 425. https://doi.org/10.2307/30036540.

[44] Vatsa, P., Ma, W., and Zheng, H. (2023). Mobile payment adoption in China: Do demographic and socioeconomic factors matter? Managerial and Decision Economics, 45(2), 201–211. https://doi.org/10.1002/mde.4086.

[45] Wang, X., Lin, X., and Spencer, M. K. (2018). Exploring the effects of extrinsic motivation on consumer behaviors in social commerce: Revealing consumers’ perceptions of social commerce benefits. International Journal of Information Management, 45, 163–175. https://doi.org/10.1016/j.ijinfomgt.2018.11.010.

[46] Zhou, T. (2012). An empirical examination of continuance intention of mobile payment services. Decision Support Systems, 54(2), 1085–1091. https://doi.org/10.1016/j.dss.2012.10.034.

Biographies

Madhvendra Pratap Singh holds a B.Sc. degree from science stream and an MBA degree. Madhvendra is also a UGC NET qualified scholar and pursuing his Ph.D. in the Management field from the School of Management and Business Studies, Chhatrapati Shahu Ji Maharaj University, Kanpur, Uttar Pradesh, India. He has over ten years of teaching and research experience and has published more than ten research papers in indexed journals, which includes Scopus and ABDC-listed publications. His research interests include business research, service marketing, and consumer-oriented studies. He is very actively contributing to the academic community and often acts as a reviewer for such reputed journals.

Mridulesh Singh is an Associate Professor in the Department of Business Management at Chhatrapati Shahu Ji Maharaj University. He holds a Ph.D. in Business Management and has extensive academic and research experience. Dr. Singh has published numerous papers in reputed indexed journals and authored several books in the field of management. He has also conducted Faculty Development Programs (FDPs) and delivered expert sessions on diverse contemporary management topics.

Journal of Reliability and Statistical Studies, Vol. 18, Issue 2 (2025), 399–418.

doi: 10.13052/jrss0974-8024.1826

© 2025 River Publishers