Efficiency of Mergers and Acquisitions (M&A): The Case of Greek Banks

Dimitrios I. Vortelinos1 and Anargiros Papaioannou2

1Department of Accounting and Finance, Hellenic Mediterranean University, Greece

E-mail: dvortelinos@hmu.gr

2Department of Business Administration and Tourism, Hellenic Mediterranean University, Greece

E-mail: ipassas@hmu.gr

Corresponding Author: Dimitrios I. Vortelinos;

E-mail address: dvortelinos@hmu.gr

Received 12 November 2024, Accepted 20 December 2024; Published Online: 31 December 2025.

Abstract

This study investigates the efficiency and value creation outcomes of mergers and acquisitions (M&As) in the Greek banking sector amid the turbulent period of 2012–2013. Combining a comprehensive review of international M&A literature with empirical analysis of four major bank acquisitions—Alpha Bank, Eurobank, Piraeus Bank, and National Bank of Greece—this research examines both short-term market reactions and long-term financial and operational performance. The findings reveal a persistent asymmetry in shareholder gains, with target firm shareholders benefiting significantly, while acquiring bank shareholders realize limited or statistically insignificant returns. Furthermore, key profitability and efficiency metrics, including Return on Assets (ROA), Return on Equity (ROE), and Cost-to-Income ratios, show no sustained improvement post-acquisition, underscoring the challenges of achieving synergy in crisis-driven consolidations. The study concludes that Greek banking M&As during this period were largely reactive measures driven by systemic distress and regulatory imperatives rather than strategic value maximization. Implications for policy and future research emphasize the critical role of integration quality, cultural fit, and comparative cross-country analysis in understanding post-merger success in distressed financial sectors.

Keywords: Acquisitions, mergers, performance, accounting performance measures, technical efficiency, abnormal returns, average abnormal returns, cumulative average abnormal returns.

1 Introduction

Mergers and acquisitions (M&As) have long been considered key strategic tools for firms seeking to achieve growth, improve efficiency, and enhance shareholder value. Within the banking sector, M&As are often pursued to achieve economies of scale, expand market share, diversify risk, and comply with evolving regulatory requirements. The global financial crisis of 2008 and the subsequent sovereign debt crisis in Europe have intensified consolidation waves in many banking systems, including Greece, where systemic distress and regulatory pressure triggered a series of high-profile acquisitions during 2012–2013.

Despite the theoretical expectations that M&As should create value for shareholders and improve operational efficiency, empirical evidence of their actual performance remains mixed. While some studies report significant gains following bank mergers, others find limited or no improvement in profitability or efficiency, highlighting the complexities and challenges inherent in the post-merger integration process. The Greek banking sector, characterized by severe financial strain and structural vulnerabilities during the crisis period, provides a unique case study to explore these dynamics in a distressed economic environment.

This study investigates the short- and long-term impacts of four major acquisitions by Greek systemic banks—Alpha Bank, Eurobank, Piraeus Bank, and National Bank of Greece—undertaken in 2013. Employing a multi-method approach combining event study analysis, accounting performance evaluation, and data envelopment analysis (DEA), this paper offers a comprehensive assessment of whether these transactions delivered the expected gains in shareholder wealth, profitability, and operational efficiency.

By integrating an extensive review of the international literature with rigorous empirical analysis, this paper contributes to the ongoing debate on the effectiveness of banking sector consolidation, particularly in crisis contexts. The findings provide valuable insights for policymakers, bank managers, and investors regarding the conditions under which bank mergers may succeed or fail to fulfill their strategic objectives.

The paper is structured as follows. Section 2 provides a comprehensive review of the international literature on mergers and acquisitions, focusing on their efficiency, value creation, and performance outcomes in the banking sector. Section 3 outlines the data sources, sample selection, and research methodology, including the event study, accounting performance analysis, and data envelopment analysis (DEA) techniques employed. Section 4 presents the empirical results, analyzing the short-term shareholder wealth effects, long-term profitability, and operational efficiency of the Greek systemic banks involved in acquisitions during 2013. Finally, Section 5 concludes with a summary of key findings, implications for theory and practice, and suggestions for future research.

2 Introduction to Mergers and Acquisitions

2.1 Definition, Typologies, and Financing Modalities of Mergers and Acquisitions

Mergers and acquisitions (M&As) represent pivotal corporate strategies aimed at enhancing competitive advantage, expanding market presence, or achieving operational synergies. An acquisition typically involves one company purchasing a controlling interest or the entirety of another company’s shares, leading to the absorption of the acquired entity, which ceases to operate independently. In contrast, a merger refers to the consolidation of two or more companies into a single corporate entity, often resulting in the legal dissolution of one or more of the original firms. This convergence may occur either through the integration into an existing company or the formation of a new organizational structure.

M&As can be classified according to the relationship between the participating firms. A horizontal merger occurs between companies operating within the same industry and at the same stage of production, while a vertical merger involves firms along the supply chain, such as a manufacturer acquiring a supplier or distributor. Further distinctions include product-extension mergers, where firms offer complementary products within the same market, and market-extension mergers, which unite firms with identical offerings but in different geographical regions. A conglomerate merger is characterized by the union of companies from entirely unrelated industries, typically for diversification purposes.

Similarly, acquisitions can mirror this classification. Horizontal acquisitions involve firms in the same industry, vertical acquisitions connect firms at different stages of the production process, and conglomerate acquisitions are those where the acquiring and acquired firms have no operational overlap. Conglomerate acquisitions are also referred to as diagonal acquisitions and are often pursued to reduce exposure to sector-specific risks.

Another important dimension distinguishes between friendly and hostile acquisitions. In a friendly acquisition, the target company’s management agrees to the takeover, often negotiating mutually agreeable terms and facilitating a smoother transition. Hostile acquisitions, by contrast, are unsolicited and opposed by the target’s management. These typically involve alternative strategies such as open market purchases or public takeover bids directly targeting shareholders, and they often entail higher acquisition costs due to the lack of cooperative engagement.

From a strategic standpoint, acquisitions may also be categorized as either strategic or financial. Strategic acquisitions are motivated by long-term corporate objectives such as market expansion, innovation, or operational synergy. These transactions frequently involve higher premiums and occur during the earlier phases of the target company’s development. In contrast, financial acquisitions are typically driven by investment considerations, where the buyer perceives the target as undervalued relative to its potential cash flows. Such transactions often involve lower bid prices and are frequently leveraged using debt instruments.

Financing is a critical component of M&A transactions, with firms employing various mechanisms based on cost, flexibility, and capital structure. The primary methods include all-cash transactions, all-stock deals, and mixed forms combining both. One notable cash-based mechanism is the leveraged buyout, where the acquirer uses significant debt financing to fund the transaction, often using the target company’s assets as collateral.

In terms of financial strategy, acquiring firms may utilize internal funds such as surplus cash or retained earnings, or raise capital through external sources, including equity issuance, debt instruments, or credit facilities. The choice of financing depends on multiple factors, including market conditions, the acquiring firm’s financial health, and the nature of the target. While cash offers are generally the least costly, they require immediate liquidity. Equity financing, though more expensive due to potential dilution, provides flexibility and is particularly attractive when the acquirer’s stock is overvalued. Debt financing, facilitated through bond issuance, loans, or other instruments, remains a prevalent method, especially in large-scale or strategic acquisitions.

Geographically, M&As can be either domestic, involving entities within the same country, or cross-border, wherein the acquiring and target companies are headquartered in different countries. Although cross-border transactions offer potential access to new markets and global synergies, they also pose unique challenges related to regulatory compliance, cultural integration, and political risk. Nevertheless, global M&A activity increasingly reflects a growing trend toward international expansion, driven by globalization and competitive pressures.

Overall, the typological and financial diversity of mergers and acquisitions highlights the strategic complexity of these corporate decisions. Understanding the motivations, structures, and implications of various M&A forms is essential for scholars and practitioners seeking to evaluate the effectiveness and sustainability of such transactions.

2.2 Motivations, Drivers, and Benefits of Mergers and Acquisitions

The motivations underlying mergers and acquisitions (M&As) can be broadly categorized into two principal perspectives: those of the acquiring firm (the buyer) and those of the target firm (the seller). According to Varma (2012), M&A rationales can be grouped into three overarching categories: (1) efficiency-seeking, (2) market-seeking, and (3) strategic asset-seeking.

Efficiency-seeking motives aim to optimize production processes and cost structures, often by maximizing output with limited resources or by increasing sales while maintaining or lowering operational costs. Market-seeking motives, by contrast, are primarily associated with expansion into new geographical regions or product markets. Strategic asset-seeking motives relate to the acquisition of intangible and tangible resources, including but not limited to research and development capabilities, intellectual property (e.g., patents and licenses), distribution and supply chain networks, and brand equity. These motives are particularly salient in the context of international or cross-border M&As, where firms pursue competitiveness on a global scale (Varma, 2012).

Grant et al. (2024) proposes an additional tripartite classification of M&A motives: strategic, financial, and managerial. Strategic motives—further elaborated by Weber et al. (2013)—include individual, organizational, and industry or market-related drivers. Organizational strategic motives typically involve value creation through synergies, enhanced market positioning, and access to new customer bases or distribution channels.

2.2.1 Synergy realization in M&A

One of the most widely cited strategic rationales for M&A activity is the achievement of synergies. Delios (2011) differentiates synergies into two primary forms: cost synergies and revenue synergies. Revenue synergies are realized through increased sales post-merger, which may arise from expanded customer bases or greater market power. Cost synergies, on the other hand, stem from reductions in operational expenses, typically through economies of scale, scope, or through the elimination of redundancies. Synergies can also be delineated into operational and financial types. Operational synergies are derived from the integration of production, logistics, and managerial capabilities, thereby fostering cost reductions and increased efficiency. These include economies of scale, where average production costs decline as output increases, and economies of scope, where shared resources are utilized across multiple product lines or geographical markets (Ross et al., 2013; Rosenbaum and Pearl, 2022). The realization of operational synergies enhances firm profitability by reducing per-unit production costs and enabling more efficient resource allocation (Brealey et al., 2016; Cremades, 2021).

Financial synergies, conversely, pertain to improvements in capital structure and reductions in the cost of capital. For instance, post-merger entities may benefit from lower borrowing costs due to increased size and perceived lower credit risk, often referred to as the “too big to fail” effect. Empirical evidence indicates that unrelated M&A transactions may also reduce systematic (market) risk, thereby lowering the acquiring firm’s cost of equity (DePamphilis, 2019). Traditional financial theory suggests that related mergers tend to reduce unsystematic (firm-specific) risk, contributing to a lower overall cost of capital (Brealey et al., 2016).

2.2.2 Growth and strategic positioning

A central strategic rationale for M&As is firm growth. Acquisitions provide a mechanism for rapid external expansion as opposed to slower, organic growth. Companies may prefer acquisition as it enables immediate access to new customers, revenues, and capabilities (Tvede and Faurholt, 2018; Voudouri, 2021). Moreover, acquiring an established business can be more cost-effective and less risky than developing new products or entering unfamiliar markets independently (Krug, 2009). In addition to horizontal acquisitions, firms may engage in vertical integrations to exert greater control over the supply chain. For example, upstream acquisitions enable control over input materials, while downstream acquisitions offer access to distribution channels, potentially generating both cost and revenue synergies (Ross et al., 2013; Rosenbaum and Pearl, 2022). These benefits are often categorized as industry-level strategic incentives (Weber et al., 2013).

2.2.3 Diversification and risk management

Another salient driver of M&A activity is diversification, which may be geographical or industrial in nature. Geographical diversification, commonly pursued through cross-border M&As, mitigates country-specific risks and facilitates access to new markets (Brealey et al., 2016; Cremades, 2021). Industrial diversification, particularly through unrelated or diagonal mergers, helps reduce the volatility of cash flows by spreading operations across industries with low correlation in performance (Gaughan, 2013; Berk and DeMarzo, 2013). This diversification reduces bankruptcy risk and enhances firm stability. Market globalization has further intensified M&A activity, as firms seek to maintain competitiveness by following rivals into international markets or responding to the needs of global consumers (Krishnamurti and Vishwanath, 2008). Additionally, companies may pursue acquisitions to overcome entry barriers related to regulation, culture, or consumer preferences in foreign markets.

2.2.4 Competitive and market power considerations

M&As can also be motivated by competitive dynamics. Firms may engage in mergers or acquisitions to strengthen market power, achieve monopolistic advantages, or neutralize competitors (Krug, 2009; Berk and DeMarzo, 2013). According to monopoly theory, such transactions can increase pricing power by reducing competition and increasing industry concentration, thereby enhancing revenues and long-term profitability (Weber et al., 2013; Papadakis, 2016).

2.2.5 Brand, innovation, and intellectual capital

Strategic acquisitions may also be driven by the desire to acquire strong brands or innovative capabilities. Small firms with high brand equity often become attractive targets for larger firms seeking to augment their portfolio or enter niche markets. A notable example is the acquisition of the Greek startup e-food by a larger multinational, reflecting the strategic value of branding in M&A decisions (Cremades, 2021). Similarly, established firms may acquire innovative startups to accelerate product development cycles, especially when internal R&D lacks speed or agility. Such acquisitions allow for quicker adaptation to market trends and consumer demands (Papadakis, 2016).

2.2.6 Financial motives and tax considerations

From a financial perspective, several motives may drive M&As. One such motive is tax efficiency—profitable firms may acquire loss-making entities to utilize their tax loss carryforwards, thereby reducing tax liabilities (Berk and DeMarzo, 2013). Additionally, leveraged acquisitions offer tax shields on debt financing due to the deductibility of interest expenses (Weber et al., 2013). Asset stripping is another financial motive, where an acquirer purchases a firm at a value below its net assets and profits from the subsequent sale of those assets (Johnson et al., 2015). Similarly, undervalued firms—identified via valuation metrics such as the Q-ratio or market-to-book ratios—are prime targets for acquisition with the expectation of turnaround and resale at a premium (Brealey et al., 2016; DePamphilis, 2019).

2.2.7 Managerial motives and agency considerations

Managerial motives, as explained through agency theory, highlight the divergence between the interests of managers and shareholders. Managers may pursue acquisitions to increase firm size, which often correlates with higher executive compensation and job security, rather than to maximize shareholder value (Weber et al., 2013). Acquisitions may also serve as a defensive strategy to avoid becoming a takeover target, as acquiring firms are less vulnerable to hostile bids. Furthermore, executive compensation often includes performance-based incentives linked to successful acquisitions, reinforcing managerial incentives for M&A activity (Brealey et al., 2016).

In sum, the drivers of M&A are multifaceted, encompassing strategic, financial, organizational, and individual-level considerations. These transactions serve as pivotal mechanisms for achieving growth, enhancing competitiveness, diversifying operations, and creating value—both tangible and intangible—for stakeholders.

3 The Performance of Mergers and Acquisitions

3.1 Determinants of Success and Failure in Mergers and Acquisitions

Empirical evidence indicates that a significant proportion of mergers and acquisitions (M&As) do not achieve their intended strategic or financial objectives. For instance, Solomon et al. (2018) report that approximately 50% of mergers either fail outright or fall short of expectations. Kumar (2011) synthesizes the literature and finds that 63% of studies conclude acquisitions fail, with 37% reporting no value creation and 26% noting value destruction. Similarly, Selden and Colvin (2003) estimate failure rates as high as 70% to 80%. Historical evidence from Ellis and Pekar (1978) and Marks (1988) corroborates these findings, suggesting that 50% to 80% of M&As underperform in terms of financial performance. Specifically, hostile takeovers exhibited a failure rate of approximately 47% for the period 1973–1998 (Andrade et al., 2001).

A primary reason cited for M&A failure is the inability to achieve effective post-acquisition integration, particularly cultural integration (Cremades, 2021; Papadakis, 2016). Brealey et al. (2016) note that cultural differences, cited in approximately 85% of unsuccessful integrations, represent a major barrier. Incompatible corporate cultures, conflicting values, and divergent strategic visions frequently impede successful integration (Cremades, 2021). To mitigate these challenges, targeted management of cultural transformation—termed “cultural integration”—is necessary (Hrebiniak and Black, 2013). Failure to manage cultural differences may result in the departure of key employees, diminished morale and productivity, and ultimately deteriorated customer service (DePamphilis, 2019).

Integration difficulties are further exacerbated by discrepancies in operational systems and methods. For example, challenges in harmonizing distribution systems can hinder post-merger efficiency (Grant et al., 2024). In such cases, the acquired firm’s need for organizational autonomy may be pronounced, particularly in unrelated acquisitions or when cultural and operational disparities are significant. According to integration typologies, the appropriate strategy varies depending on the level of strategic interdependence and required autonomy: preservation, coexistence, absorption, or holding (Johnson et al., 2015; Thanos, 2021). When strategic interdependence is high and autonomy low, rapid integration or “absorption” is preferred. Conversely, where interdependence is low and autonomy is unnecessary, the acquired company may continue to operate independently under the ownership of the acquiring firm.

Another barrier to successful integration is implementation speed. Excessively rapid change can disrupt processes and overlook critical contextual variables, particularly in complex integrations (Hrebiniak and Black, 2013). However, this concern is less relevant in scenarios of strategic coexistence or when gradual absorption is employed.

The absence of a robust post-acquisition plan constitutes another significant cause of failure. Approximately 80% of failed mergers are attributed to insufficient post-merger planning (Brealey et al., 2016). Effective M&A execution necessitates comprehensive planning before and after the transaction (Grant et al., 2024). Among the most cited failures is the inability to realize expected synergies (Papadakis, 2016), often stemming from their overestimation. A McKinsey & Company study reveals that 70% of acquiring firms overestimate revenue synergies, while 40% overestimate cost synergies (Grant et al., 2024).

Overestimated revenue synergies are frequently based on unrealistic sales projections, which may not materialize due to competitive price responses or heightened customer expectations (Papadakis, 2002). Moreover, target company misvaluation remains a pervasive problem. Poor due diligence or inadequate evaluation may result in acquiring fundamentally weak or incompatible firms (Thanos, 2021; Jones, 2016).

Pre-acquisition goal setting has been identified as a critical success factor. Brealey et al. (2016) reports that 76% of successful acquisitions had clearly defined objectives. Another determinant is the human capital element. Lack of respect by acquirers for the acquired firm’s products, markets, or clientele, and low motivation among retained employees, frequently contribute to failure. Drucker (2020) advocates for offering incentives (e.g., bonuses, promotions) within the first year post-acquisition to maintain morale and productivity.

Managerial hubris also plays a pivotal role in acquisition failure. Overconfidence in managerial capabilities can result in overambitious and poorly executed expansions (Varma, 2012; Voudouri, 2021). This behavioral bias leads to the pursuit of undervalued targets without sufficient grounding and can reflect the prioritization of personal ambitions over shareholder interests (Berk and DeMarzo, 2013). Furthermore, inexperience or incompetence among acquiring firms—particularly those engaging in their first acquisition—amplifies risk (Cremades, 2021).

Excessive acquisition premiums are another notable contributor to failure. If the present value of anticipated cash flows does not exceed the acquisition cost, the investment yields a negative or neutral net present value (Krug, 2009). Porter’s “entry test” underscores the importance of paying a fair price. Huyett et al. (2010) warn that acquiring companies must avoid overpaying to ensure value creation. On average, acquisition premiums hover around 30%, with the 2017 Boston Consulting Group study reporting an average of 33% (Watson and Head, 2019). Premiums well above this benchmark often compromise value creation.

Additionally, high leverage resulting from acquisition-related borrowing presents significant post-transaction risks (Voudouri, 2021). In leveraged buyouts or hostile takeovers, acquirers may incur substantial debt, increasing bankruptcy risk if performance falters (Papadakis, 2002). This risk is compounded if the target firm itself is highly leveraged.

Exogenous factors also influence M&A outcomes. Unforeseen shifts in market conditions, such as economic downturns or global crises (e.g., the COVID-19 pandemic), may significantly alter the valuation of target firms and disrupt post-merger forecasts (Cremades, 2021).

Finally, unattractive industry structure in the target firm’s sector can obstruct long-term profitability. As articulated in Porter’s “attractiveness test,” sectors characterized by perfect competition and minimal margins are unlikely to yield sustainable gains (Krug, 2009).

These determinants of M&A success or failure can be broadly categorized based on the timing of their impact—pre-acquisition versus post-acquisition—as illustrated in Table 3.1.

Table 1 Reasons for M&A failure

| Time Period | Key Reasons for M&A Failure |

| Pre-Acquisition | – Lack of clear goal setting |

| – Inadequate due diligence | |

| – Overestimation of synergies | |

| – Excessive acquisition premiums | |

| – Managerial hubris | |

| – Misvaluation of target companies | |

| Post-Acquisition | – Integration difficulties (cultural, operational) |

| – Poor planning | |

| – Human resource challenges | |

| – Inappropriate pace of implementation | |

Source: Thanos (2021).

These multifaceted challenges underline the complexity of M&A processes and underscore the necessity for strategic alignment, thorough evaluation, and effective post-merger integration to enhance the likelihood of success.

3.2 Factors Affecting the Performance of Mergers & Acquisitions

The performance efficiency of mergers and acquisitions (M&As) is commonly defined as the financial outcome experienced by the acquiring firm following the merger or acquisition, encompassing the resultant creation or destruction of shareholder value (Hrebiniak and Black, 2013). This efficiency is evaluated using various methodologies and can be categorized into short-term performance, typically measured within a few days surrounding the announcement date, and long-term performance, which may extend up to five years post-announcement. The extant literature predominantly emphasizes short-term efficiency, with fewer studies addressing long-term outcomes.

A critical determinant of acquisition performance is the mode of payment utilized by the acquiring firm, specifically whether the acquisition is financed through cash or equity issuance. Loughran and Vijh (1996), analyzing data from 1970 to 1989, documented that acquiring firms paying in cash experienced positive abnormal returns averaging 18.5%, while those paying with shares incurred negative abnormal returns of approximately 24.2% (Andrade et al., 2001). Consistent with these findings, Gregory (1997) also reported positive abnormal returns for cash-financed acquisitions. Similarly, Huang and Walkling (1987) observed that cash offers yield higher and more significant abnormal returns compared to share offers. A contemporaneous study by Travlos (1987) corroborated these results, demonstrating that share-financed acquisitions are associated with negative abnormal returns for acquiring firm shareholders at announcement, whereas cash-financed acquisitions generate positive excess returns.

Eckbo and Thorburn (2000) further extended this analysis, reporting that acquisitions paid exclusively in cash resulted in average abnormal returns of 3.1% to the target’s shareholders, 3% for share-financed deals, and 5.1% for mixed payment acquisitions. More recent research supports this trend: Betton et al. (2008) found that large firms acquiring smaller firms via share issuance incurred negative abnormal returns, while Mateev (2017) similarly concluded that cash acquisitions outperform share acquisitions in terms of abnormal returns.

Several theoretical explanations underpin the superior performance of cash-financed acquisitions. First, consistent with Myers and Majluf’s (1987) model, investors perceive equity issuance during acquisitions as a signal of overvaluation, prompting them to sell shares and thereby depress stock prices, resulting in negative abnormal returns (Krishnamurti and Vishwanath, 2008). Second, payment in cash conveys confidence from the acquiring firm regarding the value of the target, mitigating adverse selection problems arising from information asymmetry (Krishnamurti and Vishwanath, 2008). Third, cash acquisitions are often debt-financed and, given that the cost of debt capital is typically lower than the cost of equity capital, this financing structure enhances acquisition efficiency. Thus, it can be concluded that cash-based acquisitions, including leveraged buyouts, generally exhibit greater efficiency than share-financed transactions.

Another determinant of acquisition success relates to the acquiring firm’s strategic orientation. Cihan and Tice (2010), analyzing a large sample of 1810 firms over the period 1981–2010, found that acquisitions executed by diversified firms yielded superior performance compared to focused firms, attributable to higher profit margins and lower costs. Specifically, diversified acquirers’ stock returns were 1.5 percentage points higher at announcement relative to those of focused acquirers (Gaughan, 2015).

The financial characteristics of the target firm also significantly influence acquisition outcomes. Ray and Vermaelen (1998), examining over 3700 M&As from 1980 to 1991, demonstrated that acquisitions of “glamour firms”—firms with low book-to-market (B/M) ratios and strong prior earnings and cash flow growth—yielded lower returns than acquisitions of “value firms,” characterized by higher B/M ratios and weaker prior performance (Gaughan, 2015). Sudarsanam and Mahate (2003) reinforced this conclusion, showing that glamour firms tend to reduce shareholder wealth post-acquisition relative to value firms (Watson and Head, 2019). Furthermore, firms with higher B/M ratios are more frequently targets of hostile takeovers (Gregory, 1997).

The nature of the acquisition approach, whether friendly or hostile, also affects efficiency. Hostile acquisitions tend to be more efficient but are less likely to succeed compared to friendly acquisitions (Papadakis, 2002). Ray and Vermaelen (1998) found that hostile acquisitions generate small but statistically significant positive abnormal returns for acquiring shareholders up to three years post-acquisition, whereas friendly acquisitions yield lower or insignificant returns. Similarly, Higson and Elliott (1997) reported higher returns to target shareholders in hostile acquisitions relative to friendly ones during the announcement period in the UK market (1975–1990). Gregory (1997) also confirmed that friendly acquisitions generally produce insignificant or negative returns for acquiring firms.

Geographical factors play a role as well. Domestic acquisitions typically outperform cross-border transactions. For instance, Eckbo and Thorburn (2000) observed positive abnormal returns for Canadian domestic acquirers at announcement contrasted with insignificant returns for foreign acquirers. This finding aligns with Wennekers (2021), who reported that domestic hostile takeovers yield higher short-term returns than international acquisitions. Martynova and Renneboog (2006) further demonstrated greater wealth creation for domestic acquirers relative to cross-border acquirers.

Firm size also influences acquisition efficiency. Moeller et al. (2004), in an extensive study of 12,203 acquisitions from 1980 to 2001, found that smaller acquirers earn at least 2% higher abnormal returns than larger acquirers. Das (2021) corroborated these findings, showing that smaller acquiring firms exhibit superior long-term financial performance.

The ownership structure of the target firm matters as well. Mateev and Andonov (2016) found that acquisitions of private companies generate positive abnormal returns averaging 1.01% for acquiring firm shareholders within three days of announcement, whereas acquisitions of public enterprises produce slightly negative abnormal returns (0.13%).

Corporate governance quality is another critical factor. Firms with stronger governance tend to pay lower acquisition premiums (Martynova and Renneboog, 2008), and high governance scores correlate positively with improved post-acquisition profitability and shareholder wealth creation (Rani et al., 2016).

Finally, the competitive landscape impacts acquisition performance. Acquisitions with fewer potential bidders tend to create more value, as stock returns of acquirers negatively correlate with the number of bidders (Clayman et al., 2012).

Beyond firm-specific characteristics, macroeconomic conditions also influence M&A efficiency. Lakstutiene et al. (2015) found that acquisitions conducted during economic downturns tend to be more efficient than those during periods of economic expansion.

Table 1 summarizes the principal factors associated with greater M&A efficiency.

Table 2 Factors affecting M&A profitability

| Factor | Associated with Greater Efficiency |

| Country of origin of acquiring firm | Domestic acquisition |

| Acquisition approach | Hostile takeover |

| Payment method | Cash payment |

| Acquirer strategy | Diversified company |

| Target company type | Value company |

| Ownership of target company | Private company |

| Acquirer size | Small company |

| Number of bidders | Small number of potential buyers |

3.3 Impacts of Mergers and Acquisitions

Mergers and acquisitions (M&As) affect both the shareholders of the target (acquired) company and the shareholders of the acquiring company. Most studies conclude that M&As have a more positive short-term impact on the shareholders of the target companies, whereas shareholders of acquiring companies tend to realize returns in the long term (Clayman et al., 2012).

For example, Eckbo (2008), studying US companies over the period 1980–2005, found that at the announcement of a merger, the stock price of the target company rises by about 15%, while the acquiring company’s stock price increases by only about 1% (Berk and DeMarzo, 2013). Similarly, research on 1305 companies from 1990 to 1999 showed that returns on acquiring company shares were slightly negative but statistically insignificant, whereas target company shares gained slightly over 20% around the announcement date (Mulherin and Boone, 2000).

Overall, many studies find that acquiring companies’ shareholders tend to experience negative average returns in the short term, while target company shareholders realize positive returns (Greenbaum and Thakor, 2007).

Regarding bondholders, M&As have a limited effect (DePamphilis, 2019). Research on European companies found that bondholders of acquiring companies earned average abnormal returns of 0.56% (median 0.81%), whereas bond returns for target companies were positive but statistically insignificant (Renneboog and Szilagyi, 2006). While theory suggests that M&As might transfer wealth from bondholders to shareholders, empirical evidence is mixed. For example, a study of 3901 bonds from 1979 to 1997 found significant positive abnormal returns for target company bonds and significant negative returns for acquiring company bonds at announcement, but this did not conclusively demonstrate wealth transfer (Billet et al., 2004). Earlier research by Lehn and Poulsen (1988) also found no evidence of wealth transfer from bondholders to shareholders in leveraged buyouts (Gaughan, 2015).

M&As significantly impact human resources. Acquiring firms sometimes treat employees as expendable, leading to reduced motivation, increased turnover, and lowered productivity (Davies and Wei, 2011). Studies show that approximately 23% of employees at acquired companies were laid off or voluntarily left, while nearly half changed roles within the company (Andrade et al., 2001).

However, retention of “key” employees and managers is critical for M&A success. Research by Watson Wyatt, involving executives from 190 companies in 1998–1999, found that about three-quarters of companies prioritize retaining key employees and about two-thirds prioritize retaining key managers.

The type of acquisition matters for employees; unrelated acquisitions or acquisitions of only part of a business tend to have more positive effects on employees (Siegel and Simons, 2008). Conversely, M&As often increase employee stress due to concerns about relocation, role changes, career prospects, and compensation (Cartwright and Cooper, 1992; Rafique, 2021). Managers also experience anxiety about job security, cultural assimilation, and adapting to new corporate missions post-acquisition (Cartwright and Cooper, 1992; Rafique, 2021).

At a societal level, M&As generally have a neutral to positive effect. They often improve company productivity, increase product and service supply, and lower consumer prices (DePamphilis, 2019). However, horizontal mergers can increase market concentration and monopoly power, potentially leading to higher prices for consumers. This effect offsets gains from economies of scale, resulting in little net change in overall economic welfare (Cowling et al., 1980; Watson and Head, 2019). Additionally, acquisitions motivated solely by increasing monopoly power do not improve company performance (Eckbo, 1992).

Empirical research shows that M&As increase average company productivity by approximately 4.8% (Dimopoulos and Sacchetto, 2017). This productivity growth positively affects society by boosting employment and reducing unemployment, as companies tend to hire more and lay off fewer employees post-acquisition (DePamphilis, 2019).

4 Empirical Research on the Efficiency of Mergers and Acquisitions in Greece

4.1 Data and Research Methodology

4.1.1 Stock market measures (event study)

To measure short-term shareholder profitability, we apply an event study methodology focusing on the announcement of each acquisition or merger.

• Average abnormal return (AAR):

Calculated as the average of abnormal returns over a defined event window, where abnormal returns (AR) are the difference between actual returns and expected returns.

AR_i &= R_i - E(R_i) AAR_i = ∑^N_t=1AR_t/N• Cumulative average abnormal return (CAAR):

Firstly, the cumulative abnormal return (CAR) is estimated:

CAR_i(t_1,t_2) = ∑^t_2_t=t_1AR_i,t

Then, estimate the average of it; in the cumulative average abnormal return (CAAR):

• The expected returns are estimated using the market model regression:

with the error term; where is intercept, is beta coefficient (systematic risk), and is the expected market return.

The event window covers 3 days before to 3 days after the announcement ( to ), with particular focus on the announcement day and the three subsequent days.

We test the statistical significance of AAR and CAAR using t-statistics, comparing to critical values (Kintis, 1998).

Additionally, we use a multiple regression with dummy variables to analyze abnormal returns before, on, and after the announcement date:

where if day t is the announcement day, if day t is 3 days prior to the announcement, if day t is 3 days after the announcement (and zero otherwise, for all D variables), is the error term. The three coefficients measure the direct impact upon abnormal returns on the respective days. The same regression is also extended for CAR instead of AR.

4.1.2 Accounting measures (accounting study)

To evaluate long-term financial performance, we calculate profitability ratios for each acquiring bank over two periods:

• Pre-acquisition: 2009–2012

• Post-acquisition: 2013–2016.

Specifically, we calculate:

• Return on equity (ROE):

• Return on assets (ROA):

The average values over each period are computed using the arithmetic mean to identify changes in profitability resulting from the M&As.

4.1.3 Technical efficiency (DEA method)

To assess operational efficiency, we apply data envelopment analysis (DEA) to measure technical efficiency, reflecting how effectively banks convert inputs into outputs. Inputs are the number of branches and the number of employees. Output is the net interest income (interest income from loans minus interest expenses on deposits). Efficiency scores range from 0 to 1, with scores closer to 1 indicating higher efficiency.

4.1.4 Justification of methodology

Stock market measures capture market perception and short-term shareholder value creation or destruction upon the announcement of M&As (King et al., 2019). Accounting measures reveal actual profitability changes and wealth creation over several years post-M&A. DEA efficiency analysis complements the above by measuring operational productivity improvements due to the merger or acquisition. Avoidance of subjective survey methods reduces bias (King et al., 2019).

4.2 Analysis of the Long-term Efficiency of Acquisitions by Greek Systemic Banks

This study evaluates the long-term efficiency of acquisitions undertaken by the four major Greek systemic banks. Profitability ratios and technical efficiency metrics were estimated for pre- and post-acquisition periods to assess the impact of mergers and acquisitions (M&A). Additionally, event study methodology was applied to examine shareholder abnormal returns surrounding acquisition announcements.

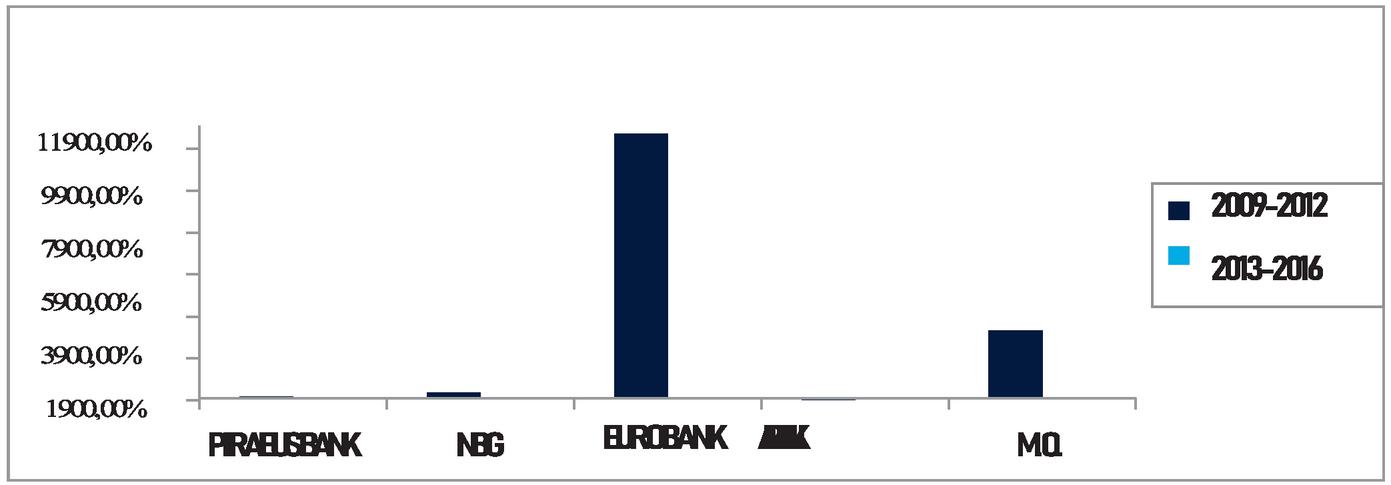

Note: ROE values for 2011-2012 are highly distorted due to negative equity during the financial crisis.

Figure 1 Average return on equity of Greek Systemic Banks before and after M&A (2009–2012 and 2013–2016).

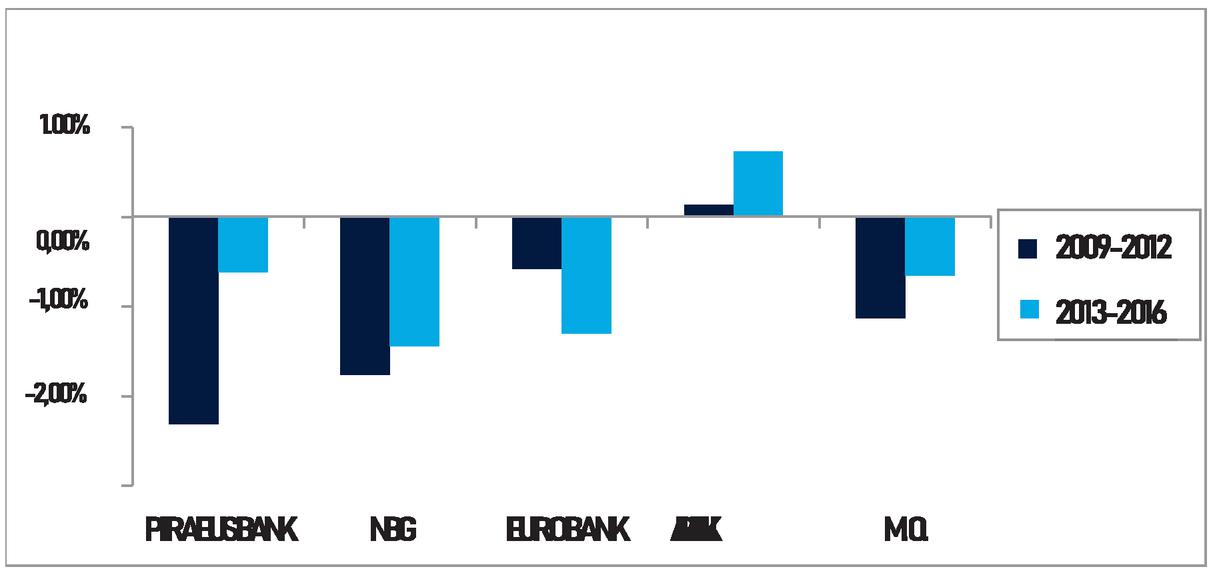

Figure 2 Average return on assets of Greek Systemic Banks before and after M&A (2009–2012 and 2013–2016).

4.2.1 Profitability ratios: ROE and ROA

The return on equity (ROE) results, presented in Figure 1, revealed anomalously high values during 2011–2012. This period coincided with substantial losses and negative equity levels, particularly for Eurobank, which reported an average ROE of 12,610.19%. Such extreme values are attributable to the combination of negative and very low equity alongside large net losses, leading to unrealistic ROE figures that distort the average. Due to these distortions, ROE is considered an unreliable indicator for profitability in this context and is thus excluded from further conclusions.

Conversely, return on assets (ROAs), shown in Figure 2, provides a more consistent and interpretable measure of bank profitability. Three out of four banks experienced slight improvements post-acquisition: Piraeus Bank’s ROA improved from 2.31% to 0.66%, National Bank of Greece (NBG) from 1.77% to 1.45%, and Alphabank from 0.13% to 0.73%. The average ROA across the four banks increased from 1.13% in the pre-acquisition period (2009–2012) to 0.66% in the post-acquisition period (2013–2016). These results suggest a modest improvement in profitability following acquisitions.

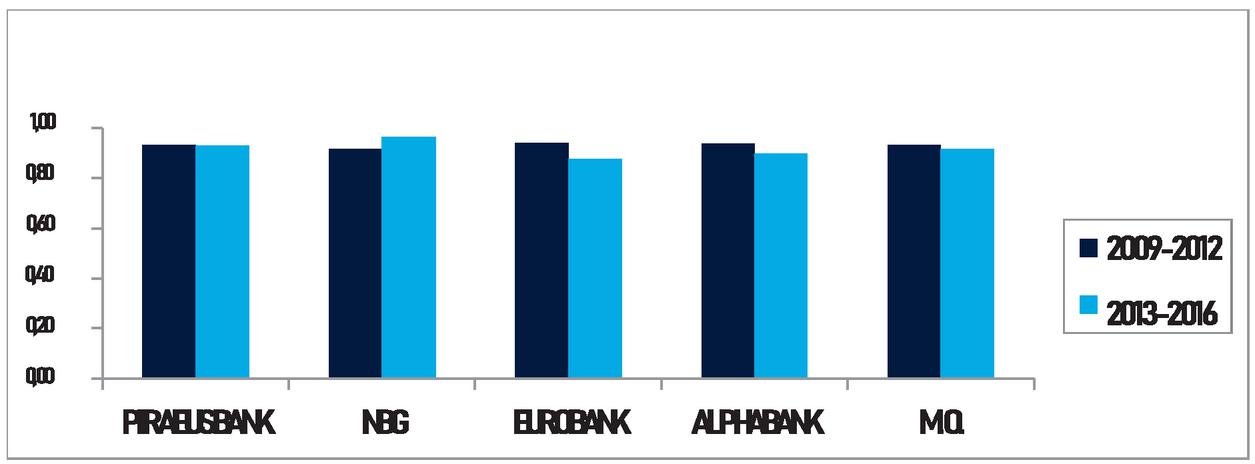

4.2.2 Technical efficiency analysis

The technical efficiency of the banks was estimated using data envelopment analysis (DEA), comparing the periods before and after acquisitions. As shown in Figure 3, the average technical efficiency marginally declined from 0.93 (2009–2012) to 0.92 (2013–2016). Specifically, Piraeus Bank’s efficiency remained stable at 0.93, NBG improved from 0.92 to 0.97, while Eurobank and Alphabank declined from 0.94 to 0.88 and from 0.94 to 0.90, respectively. These results indicate a negligible and slightly negative impact of acquisitions on operational efficiency.

Figure 3 Technical efficiency of Greek Systemic Banks before and after M&A (2009–2012 and 2013–2016).

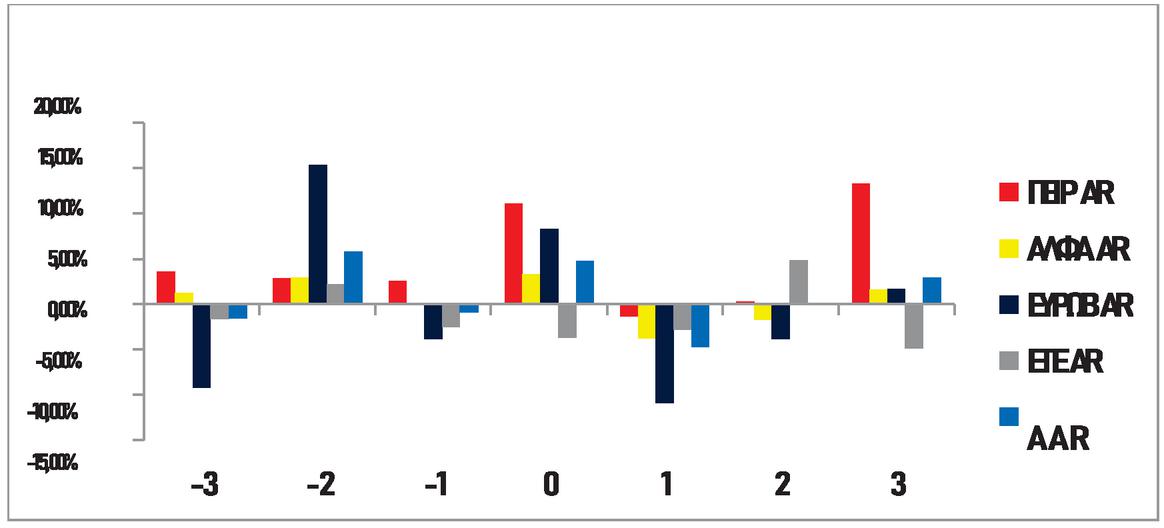

Table 3 Average excess (abnormal) returns per day and statistical significance

| Event Day | AAR (%) | t-Statistic |

| -3 | -1.51 | -0.54 |

| -2 | 5.81 | 1.84 |

| -1 | -0.95 | -0.67 |

| 0 | 4.70 | 1.44 |

| 1 | -4.72 | -2.20 |

| 2 | -0.12 | -0.06 |

| 3 | 2.91 | 0.77 |

4.2.3 Event study: Abnormal returns around acquisition announcements

To assess shareholder value creation, abnormal returns were calculated using the single-index model. The expected returns for each acquiring bank were estimated as follows (intercepts omitted due to insignificance):

E(R_Piraeus)&=1.87×E(R_m)

E(R_Alphabank)=2.45×E(R_m)

E(R_Eurobank)=1.33×E(R_m)

E(R_NBG)=2.06×E(R_m)

Abnormal returns (AR) regressed on event window dummy variables; resulted in the following:

where if day t is within the pre-announcement window (3 days prior to the announcement), if day t is within the post-announcement window (3 days after the announcement) (and zero otherwise, for all D variables), and is the error term.

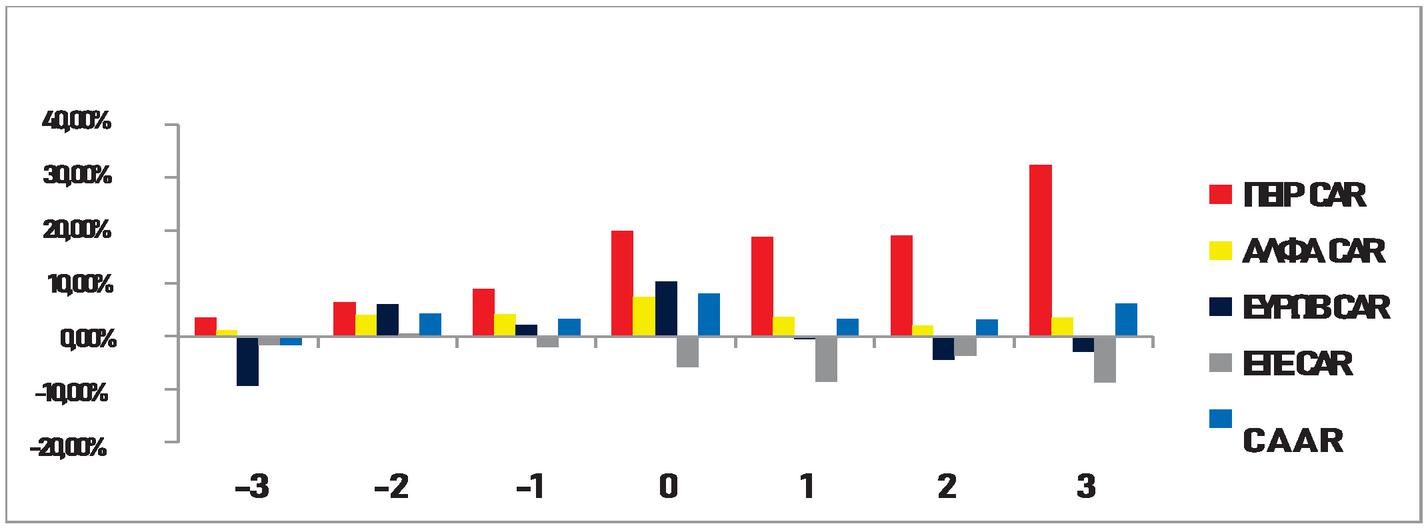

Figure 4 Excess (abnormal) returns of Greek Systemic Banks before, during, and after acquisitions (three-day event window).

Table 4 Cumulative average excess (abnormal) returns and statistical significance

| Event Day | CAAR (%) | t-Statistic |

| -3 | -1.51 | -0.54 |

| -2 | 4.30 | 3.24 |

| -1 | 3.34 | 1.49 |

| 0 | 8.05 | 1.52 |

| 1 | 3.33 | 0.58 |

| 2 | 3.21 | 0.59 |

| 3 | 6.13 | 0.67 |

Figure 5 Cumulative excess (abnormal) returns of Greek Systemic Banks around acquisition announcements (three-day event window).

The daily average abnormal returns (AAR) and their statistical significance over the event window are presented in Table 4.2.2 and visualized in Figure 4. On the announcement day , the average abnormal return was positive at 4.70%, though statistically insignificant . The day following the announcement saw a statistically significant negative abnormal return of 4.72% . The cumulative average abnormal returns (CAAR), displayed in Figure 5 and detailed in Table 4.2.3, show a positive but statistically insignificant increase of 6.13% by day three after the announcement.

4.2.4 Conclusion

The empirical evidence suggests that the acquisitions by the Greek systemic banks in 2013 had no significant effect on long-term financial performance or operational efficiency. While ROA demonstrated a slight profitability improvement post-acquisition, the overall technical efficiency decreased marginally. Furthermore, the event study reveals that acquisitions failed to generate statistically significant abnormal returns for shareholders in the short run, indicating a lack of shareholder value creation.

The distortion in ROE caused by negative equity during the crisis highlights the need to cautiously interpret profitability metrics under financial distress. Our findings contribute to the broader literature on banking consolidation, underscoring that, in this case, major acquisitions did not yield the anticipated improvements in performance or shareholder wealth.

5 Concluding Remarks

This study has sought to evaluate the efficiency and value creation of mergers and acquisitions (M&As), with a specific focus on the Greek banking sector during the critical period of 2012–2013. Combining an extensive review of the international literature with empirical analysis, this thesis provides comprehensive insights into the short-term and long-term impacts of bank acquisitions for both acquiring and target firms.

Empirical evidence from prior studies, corroborated by our own analysis, indicates that M&As generally yield limited or negligible gains for the shareholders of acquiring firms. In contrast, the shareholders of target firms tend to experience significant positive abnormal returns, affirming the asymmetrical distribution of M&A benefits.

The literature also identifies several transaction-specific and contextual factors that enhance M&A efficiency. Higher efficiency is typically observed in: domestic and hostile acquisitions; cash-financed deals; acquisitions involving undervalued or privately held firms; M&As pursued by acquirers with a diversified business strategy; and acquisitions targeting small and medium-sized enterprises (SMEs).

Our empirical investigation of the four major bank acquisitions in Greece during 2013 (namely the cases of Alpha Bank, Eurobank, Piraeus Bank, and National Bank of Greece) reveals that these strategic transactions did not produce sustained improvements in long-term financial performance or technical efficiency. Key profitability and efficiency metrics, such as return on assets (ROA), return on equity (ROE), and cost-to-income ratio, remained largely unchanged or even deteriorated post-acquisition. This finding aligns with international evidence suggesting that the anticipated synergies from banking consolidations often fail to materialize in practice.

Additionally, the short-term wealth effects of these transactions were analyzed through the calculation of abnormal returns surrounding the acquisition announcement dates. Although positive cumulative abnormal returns (CARs) were observed for some acquirers, these were statistically insignificant at conventional levels, indicating that the market response to the announcements was subdued and non-conclusive.

In conclusion, while the theoretical rationale behind M&As remains robust—especially regarding efficiency gains and shareholder value creation—the practical realization of these objectives remains elusive. For the Greek banking sector, the 2013 consolidation wave was largely reactive, driven by systemic distress and regulatory pressure, rather than by proactive strategic alignment. As such, these acquisitions failed to deliver material benefits to acquirers or their shareholders in either the short or long term.

Future research may benefit from exploring the impact of post-merger integration quality, cultural compatibility, and regulatory intervention on the success of M&As in distressed banking systems. Moreover, comparative analyses with other crisis-affected economies (e.g., Spain, Portugal, or Italy) could yield additional insights into the determinants of post-acquisition performance in the financial services industry.

References

Andrade, G., Mitchell, M. and Stafford, E. (2001). New evidence and perspectives on mergers, Journal of Economic Perspectives, 15(2), 103–120.

Berk, J. and DeMarzo, P. (2013). Corporate Finance. 3rd ed. Boston: Pearson Education.

Betton, S., Eckbo, B. E., and Thorburn, K. S. (2008). Corporate takeovers, The Handbook of Corporate Finance: Empirical Corporate Finance, 2, 291–429. Amsterdam: Elsevier/North-Holland.

Billet, M. T., King, T.-H. D., and Mauer, D. C. (2004). Bondholder wealth effects in mergers and acquisitions: New evidence from the 1980s and 1990s, Journal of Finance, 59(1), 107–135.

Brealey, R. A., Myers, S. C., and Allen, F. (2016). Principles of Corporate Finance. 12th ed. New York: McGraw-Hill Education.

Cartwright, S. and Cooper, C. L. (1992). Mergers and Acquisitions: The Human Factor. Oxford: Butterworth-Heinemann.

Cihan, E. and Tice, S. (2010). Diversification and acquisition performance: Evidence from U.S. firms, Journal of Financial Economics, 97(3), 599–621.

Clayman, M. R., Fridson, M. S., and Troughton, G. H. (2012). Corporate Finance: A Practical Approach. 2nd ed. Hoboken, NJ: John Wiley & Sons.

Cowling, K., Stoneman, P., Cubbin, J., Cable, J., Hall, G., Domberger, S., and Dutton, P. (1980). Mergers and Economic Performance. Cambridge: Cambridge University Press.

Cremades, A. (2021). Mergers and Acquisitions: A Step-by-Step Legal and Practical Guide. Hoboken, NJ: John Wiley & Sons.

Das, N. (2021). Mergers and Acquisitions: The Critical Role of Stakeholders. Abingdon: Routledge.

Davies, R. and Wei, Z. (2011). Mergers and Acquisitions: The Critical Role of Stakeholders. Farnham: Gower Publishing.

Delios, A. (2011). Experience and a firm’s performance in foreign markets: A commentary essay. Journal of Business Research, 64(2), 227–229.

DePamphilis, D. M. (2019). Mergers, Acquisitions, and Other Restructuring Activities: An Integrated Approach to Process, Tools, Cases, and Solutions. 11th ed. London: Academic Press (Elsevier).

Dimopoulos, T. and Sacchetto, S. (2017). Managers’ mobility, incentive compensation, and firm performance, Journal of Financial Economics, 124(2), 516–534.

Drucker, P. F. (2020). Management: Tasks, Responsibilities, Practices. New York: Routledge.

Eckbo, B. E. (1992). Mergers and the value of antitrust deterrence, Journal of Finance, 47(3), 1005–1029.

Eckbo, B. E. (2008). Handbook of Corporate Finance: Empirical Corporate Finance. Vol. 2. Amsterdam: Elsevier/North-Holland.

Eckbo, B. E. and Thorburn, K. S. (2000). Gains to bidders and losses to targets in corporate takeovers: Evidence from Canada, Financial Management, 29(1), 16–36.

Ellis, K. and Pekar, P. (1978). Making Mergers Work: The Strategic Importance of People. New York: McGraw-Hill.

Gaughan, P. A. (2013). Mergers, Acquisitions, and Corporate Restructurings. 6th ed. Hoboken, NJ: John Wiley & Sons.

Gaughan, P. A. (2015). Mergers, Acquisitions, and Corporate Restructurings. 7th ed. Hoboken, NJ: John Wiley & Sons.

Grant, M., Nilsson, F., and Nordvall, A. C. (2022). Pre-merger acquisition capabilities: A study of two successful serial acquirers. European Management Journal, 40(6), 932–942.

Greenbaum, S. I. and Thakor, A. V. (2007). Contemporary Financial Intermediation. 2nd ed. San Diego: Academic Press (Elsevier).

Gregory, A. (1997). An examination of the long run performance of UK acquiring firms, Journal of Business Finance & Accounting, 24(7–8), 971–1002.

Higson, C. and Elliott, J. (1997). Post-takeover returns: The UK evidence, Journal of Empirical Finance, 4(1), 27–56.

Hrebiniak, L. G. and Black, S. A. (2013). Making Strategy Work: Leading Effective Execution and Change. Upper Saddle River, NJ: Pearson Education.

Huang, Y. and Walkling, R. A. (1987). Target abnormal returns associated with acquisition announcements: Payment, acquisition form, and managerial resistance, Journal of Financial Economics, 19(2), 329–349.

Johnson, G., Whittington, R., Scholes, K., Angwin, D., and Regnér, P. (2015). Exploring Strategy: Text and Cases. 10th ed. Harlow: Pearson Education Limited.

King, D. R., Bauer, F. and Schriber, S. (2019). Routledge Companion to Mergers and Acquisitions. Abingdon: Routledge.

Krishnamurti, C. and Vishwanath, S. R. (2008). Mergers, Acquisitions and Corporate Restructuring. Los Angeles: SAGE Publications.

Krug, J. A. (2009). Mergers and Acquisitions: Managing Culture and Human Resources. New York: Business Expert Press.

Kumar, R. (2011). Mega Mergers and Acquisitions: Case Studies from Key Industries. Basingstoke: Palgrave Macmillan.

Lakstutiene, A., Breiva, A., and Lakstutis, R. (2015). The impact of macroeconomic factors on mergers and acquisitions: Lithuanian case, Procedia – Social and Behavioral Sciences, 213, 635–640.

Lehn, K. and Poulsen, A. (1988). Free cash flow and stockholder gains in going private transactions, Journal of Finance, 44(3), 771–787.

Loughran, T. and Vijh, A. M. (1996). Do long-term shareholders benefit from corporate acquisitions?, Journal of Finance, 52(5), 1765–1790.

Marks, M. L. (1988). Merging Human Resources: Managing the Cultural and Emotional Issues of Mergers and Acquisitions. San Francisco, CA: Jossey-Bass.

Martynova, M. and Renneboog, L. (2006). Mergers and acquisitions in Europe, Advances in Corporate Finance and Asset Pricing, 13–75. Amsterdam: Elsevier.

Martynova, M. and Renneboog, L. (2008). A century of corporate takeovers: What have we learned and where do we stand?, Journal of Banking & Finance, 32(10), 2148–2177.

Mateev, M. (2017). Is the M&A performance of European firms improving? New insights from the fifth merger wave, Journal of Economic Studies, 44(4), 563–592.

Mateev, M. and Andonov, K. (2016). Do cross-border and domestic acquisitions differ? Firm performance from emerging and developed markets, Research in International Business and Finance, 37, 327–356.

Moeller, S. B., Schlingemann, F. P., and Stulz, R. M. (2004). Firm size and the gains from acquisitions, Journal of Financial Economics, 73(2), 201–228.

Mulherin, J. H. and Boone, A. L. (2000). Comparing acquisitions and divestitures, Journal of Corporate Finance, 6(2), 117–139.

Myers, S. C. and Majluf, N. S. (1987). Corporate financing and investment decisions when firms have information that investors do not have, Journal of Financial Economics, 13(2), 187–221.

Papadakis, V. M. (2002). Strategic Decisions and Corporate Governance. Cheltenham: Edward Elgar Publishing.

Papadakis, V. M. (2016). Mergers, Acquisitions and Strategic Alliances: Understanding the Process. 2nd ed. London: Palgrave Macmillan.

Rafique, M. (2021). Human Resource Management in Mergers and Acquisitions. Abingdon: Routledge.

Rani, N., Yadav, S. S., and Jain, P. K. (2016). Corporate governance and firm performance post-merger and acquisition: Evidence from Indian companies, Managerial Finance, 42(7), 715–731.

Ray, K. and Vermaelen, T. (1998). Institutional ownership and the value of mergers and acquisitions, Journal of Financial Economics, 59(2), 223–260.

Renneboog, L. and Szilagyi, P. G. (2006). The impact of restructuring on bondholders, European Financial Management, 12(4), 601–624.

Rosenbaum, J. and Pearl, J. (2022). Investment Banking: Valuation, Leveraged Buyouts, and Mergers & Acquisitions. 3rd ed. Hoboken, NJ: John Wiley & Sons.

Ross, S. A., Westerfield, R. W., Jaffe, J., and Jordan, B. D. (2013). Corporate Finance. 10th ed. New York: McGraw-Hill/Irwin.

Selden, L. and Colvin, G. (2003). Angel Customers and Demon Customers: Discover Which is Which and Turbo-Charge Your Stock. New York: Portfolio (Penguin Group).

Siegel, D. S. and Simons, K. L. (2008). Human resources and R&D: Does labor turnover matter for firm productivity?, Journal of Human Resources, 43(1), 273–294.

Sudarsanam, S. and Mahate, A. A. (2003). Glamour acquirers, method of payment and post-acquisition performance: The UK evidence, Journal of Business Finance & Accounting, 30(1–2), 299–341.

Thanos, I. C. (2021). Mergers and Acquisitions: Processes, Performance, and Strategic Management. Abingdon: Routledge.

Travlos, N. G. (1987). Corporate takeover bids, methods of payment, and bidding firms’ stock returns, Journal of Finance, 42(4), 943–963.

Tvede, L. and Faurholt, T. (2018). Entrepreneur: Building Your Business from Start to Success. Chichester: John Wiley & Sons.

Varma, A. and Tiwari, U. (2012). Mergers and Acquisitions in the New Economic Order. 47(3), 323–327.

Varma, S. (2012). Mergers and Acquisitions: Managing Culture and Human Resources. New Delhi: Ane Books Pvt Ltd.

Voudouri, I. (2021). Mergers and Acquisitions: Theoretical Framework and Empirical Evidence. Athens: Kritiki Publications.

Watson, D. and Head, A. (2019). Corporate Finance: Principles and Practice. 8th ed. Harlow: Pearson Education Limited.

Weber, Y., Tarba, S. Y., and Rozen-Bachar, Z. (2013). Mergers and acquisitions performance paradox: The mediating role of integration approach, European Journal of International Management, 7(1), 84–107.

Wennekers, S. (2021). Mergers and Acquisitions: Domestic versus Cross-Border Performance Analysis. London: Routledge.

Handling Editor: Ioannis Passas

Citation:

Vortelinos, D. I., & Papaioannou, A. (2025). Efficiency of mergers and acquisitions (M&A): The case of Greek banks. Sustainability Research in the Mediterranean, 1(1), 1–16.

© 2025 River Publishers