Research on the Impact of Economic Financialization on Pollution Reduction – Analysis Based on Panel Data of 285 Prefecture-level Cities

Shiyin Li1,* and Rizhao Gong2

1School of Engineering Management, Hunan University of Finance and Economics, Changsha 410205, China

2School of Business, Hunan University of Science and Technology, Xiangtan 411201, China

E-mail: 249865035@qq.com; grzh661205@163.com

*Corresponding Author

Received 03 June 2022; Accepted 28 June 2022; Publication 28 December 2022

Abstract

As the core content of green China construction, pollution reduction plays an important role in achieving high-quality development. This paper mainly explores the pollution reduction effect of finance in the process of increasing the status of the national economic system, and verifies the indirect role of innovation-driven development in the relationship between economic financialization and pollution reduction. The results show that economic financialization has a significant direct impact on the emission reduction of industrial wastewater and sulfur dioxide, especially in cities with a high degree of financialization. Subsequently, the sample data transformation and the robustness test of green credit policy further support the above conclusions. At the same time, urban innovation capacity has a partial indirect effect on the pollution reduction of economic financialization, while robot use only has an indirect effect on the sulfur dioxide reduction of economic financialization. This study provides a theoretical basis for promoting wider and deeper development of green finance.

Keywords: Economic financialization, pollution reduction, innovation driven, prefecture-level city.

1 Introduction

In the report of 19th CPC National Congress, General Secretary Xi Jinping stated for the first time that “we must resolutely prevent and defuse major risks, take targeted measures to alleviate poverty, and prevent and control pollution, so that the building of a moderately prosperous society in all respects wins the approval of the people and stands the test of history.” The following year, pollution prevention and control was included in the Government Work Report as one of the “three critical battles”, with an emphasis on “ensuring an overall improvement in ecological and environmental quality”. In view of the rising call for environmental protection and governance, financial capital is gradually flowing from highly polluting and energy-consuming industries to clean and environmentally friendly industries, thus promoting the overall improvement of ecological and environmental quality [1]. Meanwhile, at the Hangzhou G20 Summit, China focused on the issue of “green finance”, taking into account the costs, benefits and risks of traditional financial business on the environment as an important reference for financial industry to support green development. For example, internal credit decisions to support clean technology transformation, and the development of green financial products according to the type of pollutants can help financial institutions to shoulder the environmental responsibility of economic development [2]. Existing research results show that the credit scale of financial institutions and financing scale of financial market are negatively correlated with environmental pollution, and financial development can improve the current situation of environmental pollution through opening regional foreign trade and upgrading and rationalization of industrial structure [3]. The cross-country heterogeneity analysis of Dogan and Seker (2016) also shows that financial development can promote the increase of renewable energy consumption and thus reduce non-renewable energy pollution emissions [4]. On the one hand, it is of great practical significance to discuss the impact of financial development on pollution reduction in the context of “pollution prevention and control” and “green finance” issues, which not only helps to evaluate the synergy between existing financial and emission reduction policies, but also provides a strong reference for the formulation and implementation of relevant policies in the future. On the other hand, based on similar research results, there must be more than one action path between financial development and pollution reduction, which may include other indirect action paths such as technology patent innovation and production mode adjustment. Further in-depth analysis of indirect action path and its transmission mechanism is of considerable theoretical value.

Scholars at home and abroad generally use two concepts of economic financialization and financial agglomeration to measure financial development. Compared with the unified concept of spatial distribution of financial agglomeration, the meaning of economic financialization is relatively scattered, including the Monopoly school in the United States, the structure of social accumulation school, the French regulatory school and the post-Keynesian school have defined it. Among them, Epstein’s (2005) definition is the most widely accepted:economic financialization is a process in which financial markets, institutions and employees play an increasingly important role in economic operation and management system at both domestic and international levels [5]. At present, according to the data comparison between the financial and real sectors nationwide, the evolution of economic financialization has led to the asset scale ratio between the financial sector and industrial enterprises rising from 1.7 in 2009 to 2.5 in 2017, and the difference in asset scale has also increased from 34.7 trillion yuan in 2009 to 162.8 trillion yuan in 2017. In terms of the total asset size of the financial sector or the asset growth rate of the financial industry and companies, finance, as an important hub of social capital allocation, is playing an increasingly important role in the national economic system. How to strengthen the process of economic financialization to boost the green development of real economy and strive to improve the “gold content” of growth is the core problem to be solved in China’s economy.

General Secretary Xi Jinping stressed at the 13th Group study session of the Political Bureau of the CPC Central Committee that the economy is the body, and finance is the blood, and the two coexist and prosper together. We need to deepen our understanding of the nature and laws of finance, and blaze a path of financial development with Chinese characteristics based on China’s reality. Therefore, this paper focuses on exploring the pollution reduction effect of finance in the process of upgrading the status of the national economic system (economic financialization), conforming to the path of green finance development with Chinese characteristics, and enriching the research and discussion on economic financialization and environmental protection governance. There are two possible marginal contributions: one is the measurement of pollution emission reduction effect. Based on the traditional measurement method of pollutant emission intensity, the difference calculation of pollutant emission change is adopted to reflect the internal structure of data “change of change”. The second is the analysis of the impact path of economic financialization on pollution reduction. Based on the basic regression results and robustness test, the indirect effects of urban innovation ability and robot usage density are further verified, which provides policy reference for realizing the emission reduction target in the process of economic financialization.

2 Theoretical Mechanism and Analysis

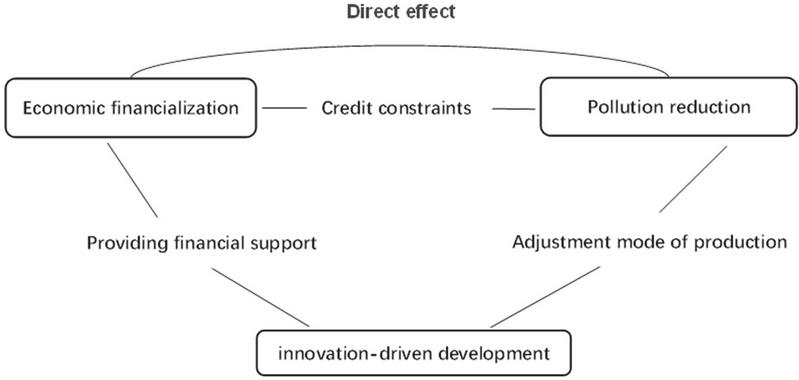

The influence of economic financialization on environmental protection and governance originates from the study of enterprises’ environmental social responsibility. The concept of “green finance” links environmental issues with financial institutions, and makes capital allocation more inclined to enterprises with low energy consumption and low pollution. Moreover, it believes that if environmental risks and social responsibilities of enterprises are not considered in credit decisions, economic sustainability will suffer serious losses [6]. However, at the very beginning of the founding of China, the strategic guidance of giving priority to the development of heavy industry was established, and a large amount of state and private capital was invested in resource-based industries such as metal smelting and processing, chemical raw material manufacturing, oil and coal mining, which were also regarded as key industries for pollutant emission control [7]. Therefore, the direct effect of economic financialization on pollution reduction comes from the internal adjustment of the credit structure of the financial system, shifting from supporting the development of heavy industry with high energy consumption and high pollution to supporting green enterprises with clean production, thus achieving the environmental goal of pollution reduction (as shown in Figure 1).

Figure 1 Indirect path of service industry development in the impact of economic financialization on pollution reduction.

However, the credit constraint on heavy polluting industries is only a basic way to reduce pollution in the process of economic financialization, and its essence is to adjust the direction of credit to restrict the production activities of non-environmentally friendly enterprises. Both the literature research results show that the formation of regional financial development using money, orientation, and catalytic mechanism could improve the ability of money supply, credit and alleviate enterprise innovation by financing constraints, then affect the distribution structure of production factors to boost the growth of the service industry, to alleviate the financing constraints of enterprise R & D and innovation, and the formation of regional financial center promotes the progress of fintech will also help to reduce the barriers of capital flow and information sharing, and meet the “small and efficient” financing needs of urban services to provide a steady stream of technological innovation vitality for the real economy [8]. At the same time, technological innovation changes the division of labor and optimize and adjust the original production mode to change the original energy supply and demand and consumption of the original industrial structure, on oil, coal and other traditional energy dependence, reduce the dependence on oil, coal and other traditional energy in economic growth, so as to achieve the environmental goal of pollution reduction [9]. Therefore, in the impact of economic financialization on pollution reduction, there is another indirect path of innovation-driven development, that is, innovation-driven development promotes the pollution reduction effect of economic financialization.

3 Research Methods and Instructions

3.1 Model Specification

The main content of this paper is the effect of economic financialization on pollution reduction and its pathway mechanism. The core explanatory variable is economic financialization, and the explained variable is pollution reduction effect. Since nonlinear relations are rarely considered in relevant studies, the econometric model in this paper adopts linear relations for estimation, and logarithms (double logarithm model) are used on both sides of the equation to mitigate the impact of data fluctuation and heteroscedasticity on the estimation results. The specific structure is shown as follows:

| (1) |

Among them, i representing different cities, t represents different years. Explained variable lnpol_red is the logarithmic form of pollution reduction effect, core explanatory variable lnfinance represents the logarithmic form of the financialization of the economy, control variables lnEconomy is the Logarithmic indicators related to economic development, lnEnviron is the logarithmic indicators related to environmental governance. In addition, reflect individual effect or heterogeneity effect, is the random interference term.

Table 1 Descriptive statistics and description of selected variables

| Variable symbol | Mean | SD | Number | Variable Declaration |

| wastewater | 79.557 | 100.34 | 3199 | Industrial wastewater discharge (million tons) |

| so2_emi | 61.671 | 59.915 | 3199 | Sulfur dioxide emissions (thousand tons) |

| dep_loan | 127.29 | 67.251 | 3199 | Balance of deposits and Loans of financial institutions (MILLION yuan) |

| per_gdp | 3.4953 | 2.6436 | 3199 | Per capita GDP (ten thousand yuan) |

| sec_gdp | 80.503 | 102.14 | 3199 | Output value of secondary Industry (BILLION YUAN) |

| gdp | 164.06 | 233.16 | 3199 | GDP ($billion) |

| road | 16.041 | 23.195 | 3199 | Urban Road Area (million square meters) |

| cons_sum | 60.135 | 91.134 | 3199 | Total Retail sales of Consumer Goods ($billion) |

| solid_use | 80.018 | 21.983 | 3199 | Comprehensive utilization rate of industrial solid Waste (%) |

| garbage | 85.022 | 22.117 | 3199 | Harmless treatment rate of household garbage (%) |

| life_water | 70.408 | 23.519 | 3199 | Urban domestic sewage treatment rate (%) |

| govern_ex | 227.09 | 388.06 | 3199 | Government Expenditure (100 million yuan) |

3.2 Variable Selection

Core explanatory variable: Although economic financialization involves the change of macro-aggregate representation and micro-structural characteristics, this paper refers to the ideas of Zhao Feng and Tian Jiahe (2015) [10]. The ratio of (dep_loan) outstanding of financial institutions to GROSS domestic product (GDP) is used to represent the degree of financial economy. The higher the proportion is, the more finance penetrates into the economic field and the higher the financial degree of the city’s economy.

Explained variables: Industrial pollutants include soot, dust, waste water, sulfur dioxide, waste solids and other forms. [11]. However, the discharge of industrial wastewater and sulfur dioxide is more common, so based on the availability of samples, this paper will focus on the pollution reduction effect of industrial wastewater and sulfur dioxide [12]. The measurement of pollution reduction effect in the existing literature focuses on the absolute amount or absolute value, that is, the emission intensity of pollutants is used as the explained variable of the model, and the existence of emission reduction effect is judged by the sign of the core explanatory variable in the regression result [13]. Borrowed this method in this paper, and further USES the relative amounts or relative (difference) to represent the pollution reduction effect, there is the advantage of the following two aspects: one is the relative amounts reflected more data “changes of internal structure,” is to increment or decrement is not compared to the stock changes, environmental management and pollution prevention and control to fine direction; Second, the relative quantity can highlight the effect of “emission reduction”. It is the emission of pollutants in the current period minus the emission of pollutants in the previous period, which is conducive to the transition to green development of decreasing pollutants under the total amount control standard.

Other control variables: The control variables in this paper include two aspects, one is urban economic development, the other is urban environmental governance. The control variables of urban economic development include per capita GDP, output value of secondary industry, urban road area and total retail sales of social consumer goods, which reflect the objective economic conditions of pollutant emission. The control variables of urban environmental governance include comprehensive utilization rate of industrial solid waste, harmless treatment rate of domestic waste, treatment rate of urban domestic sewage and government financial expenditure, which reflect the environmental regulation constraints of pollutant discharge. All the sample variables mentioned above are from China Urban Statistical Yearbook and other relevant text data, from which panel data sets of 285 prefecture-level cities from 2002 to 2016 are collected. Descriptive statistics and description of selected variables are shown in Table 1.

Table 2 Baseline regression and heterogeneity regression of the impact of economic financialization on pollution reduction

| Industrial Wastewater Reduction | Sulfur Dioxide Abatement | |||||

| Panel A Benchmark Return | Model (1) | Model (2) | Model (3) | Model (4) | Model (5) | Model (6) |

| Ln_finan | 0.357*** | 0.172*** | 0.186*** | 0.514*** | 0.119* | 0.147** |

| (0.0344) | (0.0512) | (0.0606) | (0.0437) | (0.0634) | (0.0747) | |

| Constant | 2.679*** | 1.940*** | 2.114*** | 3.848*** | 2.621*** | 2.889*** |

| (0.260) | (0.627) | (0.716) | (0.330) | (0.776) | (0.884) | |

| Economic development variable | NO | YES | YES | NO | YES | YES |

| Environmental governance variables | NO | NO | YES | NO | NO | YES |

| Observations | 3568 | 3484 | 2942 | 3549 | 3470 | 2937 |

| Hausman Test | 85.46 | 48.38 | 28.85 | 96.00 | 71.68 | 40.86 |

| F Statistics | 107.41 | 22.76 | 9.38 | 138.11 | 44.83 | 19.75 |

| R-squared | 0.0317 | 0.0344 | 0.0309 | 0.0406 | 0.0659 | 0.0630 |

| Lower | Medium | Higher | Lower | Medium | Higher | |

| Financialization | Financialization | Financialization | Financialization | Financialization | Financialization | |

| Panel B Heterogeneous Regression | Model (7) | Model (8) | Model (9) | Model (10) | Model (11) | Model (12) |

| Ln_finan | 0.0214 | 0.0416 | 0.378*** | 0.189 | 0.194 | 0.365** |

| (0.110) | (0.207) | (0.121) | (0.168) | (0.205) | (0.158) | |

| Constant | 0.248 | 0.189 | 4.100*** | 1.794 | 2.273 | 7.378*** |

| (1.451) | (2.010) | (1.319) | (2.208) | (2.001) | (1.724) | |

| Economic development variable | YES | YES | YES | YES | YES | YES |

| Environmental governance variables | YES | YES | YES | YES | YES | YES |

| Observations | 982 | 978 | 982 | 982 | 978 | 977 |

| F Statistics | 2.11 | 0.73 | 4.28 | 5.11 | 4.32 | 8.09 |

| R-squared | 0.0228 | 0.0085 | 0.0453 | 0.0535 | 0.0482 | 0.0827 |

| Note: ***, **, and * are significant at the level of 1%, 5%, and 10% respectively. Standard error indicates in brackets. | ||||||

4 Empirical Results and Analysis

4.1 Basic Regression Result

In the Table 2, Panel A, part of the results are the baseline regression results of the impact of economic financialization on pollution reduction, however, Panel, part of the results show the heterogeneity of pollution abatement effects at different levels of economic financialization. Hausman Of models (1) to (6), the test statistical results reject the null hypothesis that individual effects are independent of explanatory variables, so panel data fixed effects model is used for estimation. In the reference regression of Panel A, the gradual addition of economic development and environmental governance control variables has no influence on the results of pollution reduction effect of economic financialization. The results of models (1) to (3) show that the process of economic financialization can effectively reduce the discharge of industrial wastewater. When all control variables are added, if the ratio of the balance of deposits and loans of financial institutions to GDP increases by one percentage point, the increment of industrial wastewater discharge will decrease by 0.186% compared with the previous period. A similar conclusion exists for the emission reduction effect of sulfur dioxide. Models (4) to (6) show that the process of economic financialization can also significantly reduce the emission of sulfur dioxide. When all control variables are included, an increase in the ratio of outstanding deposits and loans of financial institutions to GDP by one percentage point will reduce the increase of sulfur dioxide emissions by 0.147% over the same period. Panel, part of the benchmark regression results prove the reduction effect of economic financialization on industrial wastewater and sulfur dioxide under the full sample. However, Wen Shuhui and Zhang Yibo (2020), when discussing the relationship between financial development and economic growth efficiency, believe that financial development has heterogeneity among different economic levels and resource endowments [14, 15]. Therefore, Panel B further investigated the heterogeneity of pollution reduction effect of economic financialization, and divided the whole sample into three types of cities with low financialization, medium financialization and high financialization by using three equal points. Models (7) to (9) reflect the emission reduction effect of economic financialization of three types of cities on industrial wastewater. Cities with high financialization can significantly reduce the discharge of industrial wastewater, while the index coefficients of cities with medium financialization and low financialization are negative but not statistically significant. In addition, models (10) to (12) show the emission reduction effect of the economic financialization of the three types of cities. Only the cities with high financialization can effectively control the increment of sulfur dioxide emissions, while the economic financialization of other types of cities has no significant impact on the emission reduction of sulfur dioxide.

4.2 Robustness Test

The basic regression results are not enough to support the conclusion that economic financialization has emission reduction effect on industrial wastewater and sulfur dioxide, and other methods are needed to test the robustness of the study (as shown in Table 3). Considering the siphoning effect of the four large first-tier cities (Beijing, Shanghai, Guangzhou and Shenzhen) on economic resources, the process of financialization is more characteristic than other cities (including the policy impact, headquarters effect and agglomeration of listed companies, etc.), so in part A of the Panel model in Table 3 (1) and (2) to cut out the four cities of Beijing, Shanghai, Guangzhou and Shenzhen before estimates [16]. The results show that the ratio of the balance of deposits and loans of financial institutions to GDP will increase by one percentage point on average, the increment of industrial wastewater discharge will decrease by 0.182%, and the increment of sulfur dioxide emission will decrease by 0.153%. This is consistent with the results of basic regression, which further indicates that economic financialization has emission reduction effect on industrial wastewater and sulfur dioxide.

Economic financialization process is the financial system in the national economy gradually dominate the process of financial institutions deposit and balance the proportion of the GDP index though to some extent can intuitively reflect the connotation of economic financialization, but in another important macro level, the financial institutions in the workforce need to continue to explore whether there is a steady results. In The model (3) and (4) of Panel A in Table 3, explanatory variables are replaced by the number of employees in financial institutions. The results show that the increment of industrial wastewater discharge will decrease by 0.700% and the increment of sulfur dioxide emission will decrease by 0.0709% in the same period. The regression results after the substitution of core variables in the samples show that the economic financialization has emission reduction effect on industrial wastewater and sulfur dioxide from another perspective.

In early 2012, the China Banking Regulatory Commission (now the China Banking and Insurance Regulatory Commission) formulated the Green Credit Guidelines to promote the development of green credit in banking oriented financial institutions, actively adjust their internal credit structure and capital flow, and actively support the work of energy conservation, emission reduction and environmental protection. Su Dongwei and Lian Lili (2018) constructed a quasi-natural experiment and found that interest-bearing debt financing and long-term debt of heavily polluting enterprises decreased significantly, as well as their business performance, indicating that green credit has significant financing penalty effect and investment inhibition effect [17]. At the same time, Chen Xingxing et al. (2019) also found that green credit policies make it more difficult for heavily polluting enterprises to obtain bank loans, thus forming green credit constraints to promote environmental governance investment of heavily polluting enterprises [18].

Table 3 Robustness test of the impact of economic financialization on pollution reduction

| Eliminate “Beijing, | Substitution | |||

| Eliminate “Beijing, Shanghai, | Substitution of | |||

| Guangzhou and Shenzhen” | Core Variables | |||

| Industrial | Sulfur | Industrial | Sulfur | |

| Wastewater | Dioxide | Wastewater | Dioxide | |

| Reduction | Abatement | Reduction | Abatement | |

| Panel A Sample Data Transformation | Model (1) | Model (2) | Model (3) | Model (4) |

| Ln_finan | 0.182*** | 0.153** | ||

| (0.0612) | (0.0754) | |||

| Ln_work_f | 0.0700* | 0.0709* | ||

| (0.0329) | (0.0369) | |||

| Constant | 2.052*** | 2.923*** | 1.340** | 2.065*** |

| (0.727) | (0.894) | (0.602) | (0.745) | |

| Economic development variable | YES | YES | YES | YES |

| Environmental governance variables | YES | YES | YES | YES |

| Observations | 2898 | 2896 | 3005 | 3001 |

| F Statistics | 9.37 | 19.39 | 12.11 | 25.68 |

| R-squared | 0.0313 | 0.0628 | 0.0386 | 0.0786 |

| Industrial Wastewater | Sulfur Dioxide | |||

| Wastewater Reduction | Dioxide Abatement | |||

| Before 2012 | After 2012 | Before 2012 | After 2012 | |

| Panel B Green Credit Guidelines | Model (5) | Model (6) | Model (7) | Model (8) |

| Ln_finan | 0.144* | 0.320* | 0.122 | 0.656*** |

| (0.0803) | (0.192) | (0.0939) | (0.230) | |

| Constant | 1.195 | 4.233* | 0.633 | 10.53*** |

| (0.976) | (2.165) | (1.145) | (2.555) | |

| Economic development variable | YES | YES | YES | YES |

| Environmental governance variables | YES | YES | YES | YES |

| Observations | 2023 | 1177 | 2015 | 1177 |

| F Statistics | 1.68 | 6.64 | 7.64 | 16.61 |

| R-squared | 0.0087 | 0.0633 | 0.0384 | 0.1447 |

| Note: ***, **, and * are significant at the level of 1%, 5%, and 10% respectively. Standard error indicates in brackets. | ||||

In Panel B of Table 3, this paper investigates the effect of emission reduction on industrial wastewater and sulfur dioxide before and after the implementation of green Credit Guidelines, that is, before and after 2012. The results show that the process of economic financialization can effectively reduce the discharge of industrial wastewater, whether before or after the implementation of the policy. However, after the implementation of the policy, the emission reduction effect is significantly improved. Every percentage point increase in the ratio of the balance of deposits and loans of financial institutions to GDP, the increment of industrial wastewater discharge after 2012 will be further reduced by 0.176% than before. In terms of the emission reduction effect of SULFUR dioxide, the emission reduction effect of economic financialization before the implementation of green Credit Guidelines is statistically insignificant, but the process of economic financialization after the implementation of green Credit Guidelines can effectively reduce sulfur dioxide emissions. When the proportion of the balance of deposits and loans of financial institutions in GDP increases by one percentage point, In the same period, the increase of sulfur dioxide emissions will be reduced by 0.656% compared with the previous period, which is more obvious than the policy effect of industrial wastewater reduction.

Table 4 Economic financialization, innovation-driven development and pollution reduction effects

| Urban Innovation Capacity | Robot Density | |||||

| Economy | Industrial | Sulfur | Economy | Industrial | Sulfur | |

| Financialization | Waste Water | Dioxide | Financialization | Waste Water | Dioxide | |

| Panel A Innovation-driven Development | Model (1) | Model (2) | Model (3) | Model (4) | Model (5) | Model (6) |

| Ln_finan | 0.160** | 0.116 | 0.312 | 0.648*** | ||

| (0.0627) | (0.0774) | (0.192) | (0.230) | |||

| Ln_innovation | 0.0728*** | 0.0232 | 0.0324 | |||

| (0.0049) | (0.0163) | (0.0200) | ||||

| Ln_robot_density | 0.0263* | 0.205 | 0.224 | |||

| (0.0151) | (0.164) | (0.190) | ||||

| Constant | 7.096*** | 1.803** | 2.526*** | 6.031*** | 4.524** | 10.85*** |

| (0.171) | (0.744) | (0.919) | (0.322) | (2.177) | (2.569) | |

| Economic development variable | YES | YES | YES | YES | YES | YES |

| Environmental governance variables | YES | YES | YES | YES | YES | YES |

| Observations | 3106 | 2932 | 2927 | 1184 | 1177 | 1177 |

| F Statistics | 437.73 | 8.67 | 17.94 | 348.22 | 6.14 | 15.10 |

| R-squared | 0.5833 | 0.0318 | 0.0638 | 0.7786 | 0.0650 | 0.1460 |

| Urban Innovation Capacity | Robot Density | |||||

| Industrial | Sulfur | Industrial | Sulfur | |||

| Panel B Indirect Effect Test | Wastewater Reduction | Dioxide Abatement | Wastewater Reduction | Dioxide Abatement | ||

| Sobel-Goodman Test | 0.0442*** | 0.1140*** | 0.0006 | 0.0314*** | ||

| (0.0079) | (0.0102) | (0.0009) | (0.0112) | |||

| Bootstrap Method | 0.0442*** | 0.1140*** | 0.0007 | 0.0314*** | ||

| (0.0082) | (0.0120) | (0.0010) | (0.0111) | |||

| Indirect effect ratio | 0.7302 | 0.9511 | 0.0157 | 0.2162 | ||

| Note: ***, ** and * are significant at the level of 1%, 5% and 10% respectively. The brackets in Panel A are standard error, and the brackets in Panel B are standard error and Bootstrap standard error. | ||||||

4.3 Indirect Effect Analysis

From the perspective of historical evolution, the essence of the emergence and product innovation of any financial institution, whether it is the currency “Jiaozi” used in early China or the shares issued by the East India Company, is to promote the major reform and development of the real economy under specific historical conditions, especially in technological research and innovation. Table 4 presents the test of the indirect effect of innovation-driven development based on the basic regression of the relationship between economic financialization and pollution reduction effect. Among them, models (1) to (6) of Panel A are methods for testing regression coefficients step by step [19]. Panel B is Sobel-Goodman test and self-sampling test [20]. As for the measurement index of innovation-driven development, this paper uses the urban innovation index in the Report on Chinese Cities and Industrial Innovation 2017 published by the Industrial Development Research Center of Fudan University to replace it [21], examines the path transmission mechanism of urban innovation capacity as an indirect variable between economic financialization and pollution reduction effect. The index uses the legal status update information of micro-authorized invention patents from SIPO and the cost structure of invention patents in different years. The patent update model is used to calculate the value weighting coefficient to obtain the total annual patent value of the city. Results showed that in test model (1) step by step to verify the city innovation ability and potential positive relationship between economic financialization, at the same time through the model (2) and (3) statistical significance indicates that the city innovation ability of industrial wastewater emissions of economic financialization indirect role fully, but for economic financialization have indirect effects on the sulfur dioxide emission reduction is still uncertain. However, further Sobel-Goodman test and the test coefficient after 1000 times of sampling show that urban innovation ability not only plays an indirect role in the emission reduction effect of industrial wastewater (effect ratio is 73.02%), but also has an obvious indirect effect on the emission reduction effect of sulfur dioxide (effect ratio is 95.11%). The indirect effect test of models (1) to (3), Sobel-Goodman and self-sampling proves the influence path of economic financialization to reduce pollution emissions by providing financial support for technological innovation.

On the other hand, according to the analysis of the theoretical mechanism above, one possible path for economic financialization to support innovation-driven development and achieve pollution reduction targets is to change the original production mode of enterprises. Therefore, this paper further adopts the industrial robot application data provided by the International Federation of Robotics (from 2012 to 2016), and measures the robot density by comparing the increase scale of robots at the industry level with the number of urban unit labor force [22], then the regional average value is calculated to represent the degree of enterprise’s change in production mode. The results show: In the test model (4) step by step to verify the robot potential positive relationship between the density and economic financialization, at the same time through the model (5) and (6) statistical significance indicates that robot density for economic financialization have indirect effects on the industrial wastewater emissions is still not sure, the economic financialization have indirect effects of sulfur dioxide emissions will be completely. At the same time, further Sobel-Goodman test and the test coefficient after 1000 times of sampling also indicate that robot density has no indirect effect on the emission reduction effect of industrial wastewater, but plays an indirect variable influence on the emission reduction effect of sulfur dioxide (the effect ratio is 21.62%). Therefore, as an important feature of production mode adjustment, the use or application of robots has a certain indirect effect on the pollution reduction effect of economic financialization, which is mainly aimed at sulfur dioxide reduction.

5 Research Conclusions and Implications

During the third group study session of the Political Bureau of the CPC Central Committee, General Secretary Xi Jinping stressed that in building a modern economic system, modern finance should constantly enhance its ability to serve the real economy. The main content of this study is the effect of economic financialization on the reduction of industrial wastewater and sulfur dioxide and the indirect effect mechanism of innovation-driven development in the relationship between the two. The results show that: firstly, the process of economic financialization has obvious pollution reduction effect, especially in cities with higher financialization degree. Finance promotes industrial transformation and upgrading and foreign economic and trade opening, thus reducing industrial wastewater and sulfur dioxide emissions. Moreover, sample data transformation and robustness test of green credit policy further support the above research results. Secondly, innovation-driven development represented by urban innovation capacity and robot usage density has a partial indirect effect on pollution reduction of economic financialization. Financialization of the economy has reduced industrial wastewater and sulfur dioxide emissions by providing funding for R&D and innovation, but the use of robots as a modification of production methods has mainly an indirect effect on sulfur dioxide reduction.

Finance plays a central role in the rational distribution of idle social funds. It plays a role in facilitating capital financing and flow, and is also playing an important role in promoting environmental protection and pollution prevention and control. The research on pollution reduction effect of economic financialization not only presents empirical facts but also reflects many problems worth thinking about: First of all, there is the unbalanced allocation of resources in the process of economic financialization. There is an obvious gap in financial resources enjoyed by different cities. Eastern cities are more developed than central and western cities, and provincial cities are more developed than non-provincial cities. Secondly, the interaction between economic financialization and innovation-driven development not only contributes to the transformation, upgrading and dynamic evolution of urban industrial structure, but also facilitates the realization of the policy goal of pollutant control and emission reduction, which endow innovation-driven development with a new mission in high-quality economic growth. Finally, the change of production organization mode caused by technological research and development innovation, the use and application of automation equipment or the updating and transformation of production links has become an important way to reduce pollution in the industrial field, and the technology biased towards cleaner production should be the primary driving force.

References

[1] Hu Zongyi, Li Yi. Double effects and threshold characteristics of financial development on environmental pollution. China Soft Science, 2019(07), 68–80.

[2] Liu Xiliang, Weng Shuyang. Should China’s financial institutions assume environmental responsibility? – Basic facts, theoretical models and empirical tests. Economic Research, 2019, 54(03): 38–54.

[3] He Jun, Cheng Rui, Liu Ting. Financial development, technological innovation and environmental pollution. Journal of Northeastern University (Social Sciences), 2019, 21(2), 139–148.

[4] Dogan E, Seker F. Determinants of CO emissions in the European Union: The role of renewable and non-renewable energy. Renewable Energy, 2016, 94, 429–439.

[5] Epstein G A. Financialization and the world economy. London: Edward Elgar, 2005.

[6] Weber O, Scholz R W, Michalik G. Incorporating Sustainability into Credit Management. Business Strategy and the Environment, 19(1), 39–50.

[7] Wen Shuyang, Liu Xiliang. Financial mismatch, environmental pollution and sustainable growth. Research on Economics and Management, 2019, 40(3), 3–20.

[8] Li Chuntao, Yan Xuwen, Song Min, Yang Wei. Fintech and Enterprise Innovation: Evidence of NeeQ Listed companies. Chinese Industrial Economy, 2020(1), 81–98.

[9] Li Hao-kuang, ZHANG Yina, Liu Liang. Technological innovation and Transformation of Production Relations – Also on the impact and adjustment of the Four Industrial Revolutions. Shanghai Econmic Review, 2020(11), 33–45.

[10] Zhao Feng, Tian Jiahe. The current level and trend of China’s economic financialization: A Structural and comparative analysis. Political economy review, 2015, 6(3), 120–142.

[11] Xu Zhiwei. Industrial economic development, environmental regulation intensity and pollution reduction effect: Theoretical analysis and empirical test based on “pollution first, treatment later” development model. Financial research, 2016, 42(3), 134–144.

[12] Gao Ming, Huang Qinghuang. Research on the relationship between environmental investment and industrial pollution reduction: Based on the threshold effect analysis of governance investment structure. Economic management, 2015, 37(2), 167–177.

[13] Wu Weiping, He Qiao. “Reverse force” or “retrogression”? – Threshold Characteristics and Spatial Spillover of environmental regulation emission reduction Effect. Economic Management, 2017, 39(2), 20–34.

[14] Wen Shuhui, Zhang Yumbo. Financial development, FDI spillovers and economic growth efficiency: An empirical study of countries along the Belt and Road. World Economic Studies, 2020(11):87–102+136–137.

[15] Claudiu A, Adrian I. The long-run impact of monetary policy uncertainty and banking stability on inward FDI in EU countries. Research in International Business and Finance, 2018, 45, 72–81.

[16] Pan Yue, Ning Bo, Ji Xiangge, Dai Yiyi. The Clan Brand of Private Capital: Evidence from the Perspective of Financing Constraints. Economic Research journal, 2019, 54(7), 94–110.

[17] Su Dongwei, Lian Lili. Does green credit affect the investment and financing behavior of heavily polluting enterprises?. Financial Research, 2018(12), 123–137.

[18] Chen Xingxing, Shi Yaya, Song Xianzhong. Green Credit constraints, Business Credit and corporate environmental governance. International Finance Research, 2019(12), 13–22.

[19] Baron R M, Kenny D A. The moderator-mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 1986, 51(6), 1173–1182.

[20] Zhao X, John G L J, Chen Q. Reconsidering Baron and Kenny: Myths and truths about mediation analysis. Journal of Consumer Research, 2010, 37(2), 197–206.

[21] Kou Zonglai, Liu Xueyue. Shanghai: Industrial Development Research Center of Fudan University, 2017.

[22] Kong Gaowen, Liu Shasha, KONG Dongmin. Robotics and employment: An exploratory analysis based on Industry and Regional Heterogeneity. Chinese Industrial Economics, 2020(8), 80–98.

Biographies

Shiyin Li is a lecturer, Her main research directions are environmental economy, urban innovation. Many articles have been published in related fields.

Gong Rizhao is a professor, His main research direction is economic statistics and decision-making. Years of working experience in digital economic statistics.

Strategic Planning for Energy and the Environment, Vol. 42_1, 1–20.

doi: 10.13052/spee1048-5236.4211

© 2022 River Publishers